For all the talk about the wind possibly coming out of the sails of the artificial intelligence (AI) trade, a real sector rotation hasn't played out.

Recent headlines suggest investors are skittish about what the near term holds for growth and technology stocks. Such jitters often compel market participants to move into defensive sectors, but broadly speaking, consumer staples stocks -- a defensive group to be sure -- aren't responding.

PepsiCo's stock is slumping. A rebound, though possible, could take some time. Image source: Getty Images.

Down 2.16% year to date, the stock of PepsiCo (PEP -0.93%) is one of the Consumer Staples sector's disappointments. Making PepsiCo's lethargy even harder to swallow for investors is that rival Coca-Cola is up more than 14% in 2025 and keeping up with the S&P 500 in the process. Combine those factors, and it might be hard to be bullish on the Gatorade maker, but there's a case for a rebound if the company can allay shareholders' concerns on multiple fronts.

First, the bad news for PepsiCo

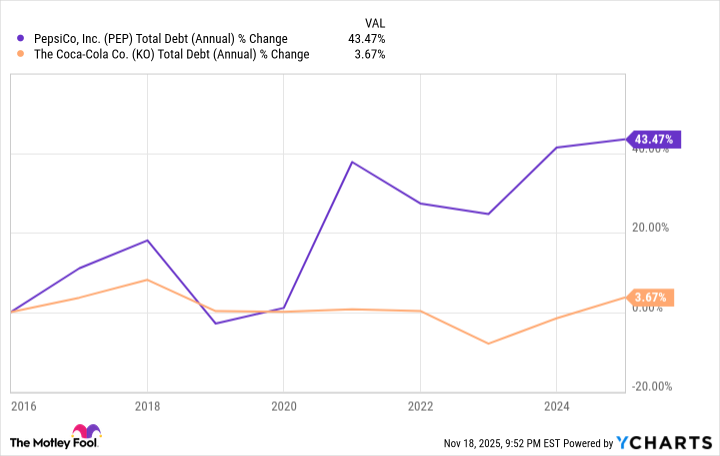

One strike against PepsiCo is that its debt levels have grown much more rapidly than those of Coca-Cola. At the end of the third quarter, PepsiCo carried long-term debt of $44.13 billion, a 14.61% year-over-year increase, extending a lengthy run during which its liabilities ballooned faster than its competitors.

Data by YCharts.

Strike two is the fact that PepsiCo's 2025 organic sales growth has been anemic, and global volumes have declined in each of the first three quarters of the year. One way of looking at those trends, at least as they relate to the U.S., is that at a time when some shoppers view the Consumer Price Index as still being elevated, the company can't price its way into revenue growth.

Strike three is more of an interesting fact. PepsiCo is no longer on the podium of the most popular sodas. That's right: not even a bronze medal as Coca-Cola Classic, Dr. Pepper, and Coke's Sprite are the medalists, with PepsiCo ranking fourth in popularity. As someone who grew up during the cola wars of the 1980s, this is stunning.

How PepsiCo can get its groove back

One of the investment cases for PepsiCo, although the news is priced into the stock, is the involvement of Elliott Investment Management, which took a $4 billion stake in the company in September. The stock hasn't done much of anything since then, but know this: Activist investors don't get involved unless they sense an opportunity to come out on top.

Elliott has made clear it wants PepsiCo to spin off its North American bottling operations -- something Coca-Cola has already done -- and perhaps prune its sprawling brand portfolio. In theory, PepsiCo retaining its North American bottling unit is sensible because it gives it control over the process, but the reality is much different. In the soda margin fight, Coca-Cola comes out far ahead because it doesn't bottle its own drinks.

NASDAQ: PEP

Key Data Points

The brand-paring option has some viability as well because PepsiCo controls 60 brands, according to its website. By parting ways with a few, it could streamline its operations, raise cash to lower debt, and simplify its investment story.

Reducing debt is always a good thing. Less cash going out the door to service liabilities means more capital retained to grow the business and support the company's membership in the Dividend Kings club, which it earned through its history of more than 50 consecutive years of annual dividend hikes. It's one of the primary reasons some investors stick with the stock.