At the time of this writing, Apple (AAPL +1.32%) is the world's second-largest company by market cap, with a $4 trillion valuation. So, predicting that a much smaller company like Taiwan Semiconductor Manufacturing (TSM +2.84%) can grow to become larger than Apple is a bold claim, especially when you consider that Taiwan Semi is a $1.4 trillion company right now. However, after looking at growth rates for the industries in which it's involved, I think Taiwan Semiconductor can achieve this feat, making it an incredible stock pick over the next few years.

I think Taiwan Semi could grow to become a larger company than Apple by 2030, but it's going to need a lot of help to accomplish that goal.

Image source: Getty Images.

Taiwan Semiconductor is front and center in the AI race

Apple doesn't need a lot of introduction. It's a leader in consumer electronics, and there's a good chance that this article is being read from an Apple-powered device. But therein lies the largest issue with Apple: market saturation. Apple has failed to grow revenue at a meaningful pace over the past few years, and it has only had one reported quarter of double-digit revenue growth since mid-2022 (and it only achieved that mark if you round up).

AAPL Revenue (Quarterly YoY Growth) data by YCharts

Apple has done a great job repurchasing shares and decreasing expenses, which has allowed its diluted earnings per share (EPS) to grow in the low-double-digit range. As a result, we'll use 12% as Apple's long-term EPS growth rate.

For Taiwan Semiconductor, it's at the heart of the artificial intelligence (AI) race. Its chips are being used in nearly every high-powered AI computing device, ranging from Nvidia graphics processing units (GPUs) to custom AI accelerators from Broadcom. Furthermore, Taiwan Semiconductor is launching new chip technology that promises to improve energy consumption by 25% to 30% when configured for the same speed as previous generations. That's game-changing technology, and allows TSMC to charge a premium for those chips.

Furthermore, there are no signs of the AI race slowing down. The other day, AMD released its projection that it expects its data center division to grow revenue at a 60% compound annual growth rate (CAGR) through 2030. That aligns well with a previous projection given by Nvidia, where global data center capital expenditures are expected to rise from $600 billion in 2025 to between $3 trillion and $4 trillion by 2030. That indicates a 42% CAGR at the midpoint, showcasing that TSMC's chip business can easily grow at that rate as well.

During Q3, Taiwan Semiconductor's revenue rose 41% in U.S. dollars, aligning with the broader market growth. That aligned with TSMC's net income growth as well, so I'll use a 40% EPS growth rate for this projection.

While that may seem like an aggressive assumption, it's what's required for TSMC to surpass Apple in market share by 2030. If the AI data center market is as large as the AMD and Nvidia projections, then this assumption may not be unreasonable.

Taiwan Semiconductor has huge upside if this projection pans out

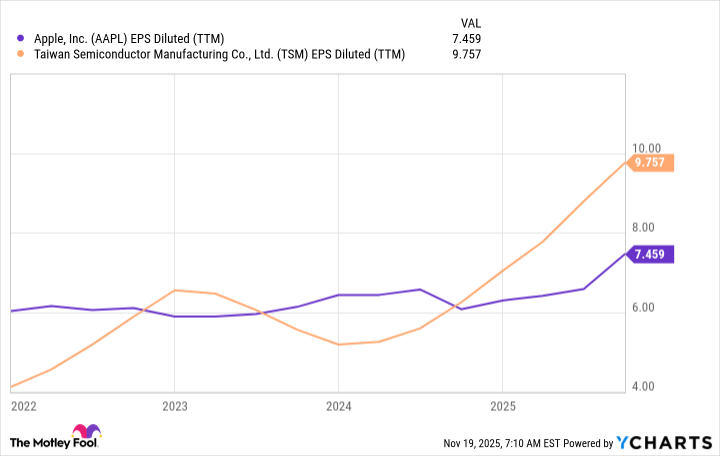

If Apple can grow its EPS by 12% throughout 2030 and Taiwan Semiconductor's rises by 40%, that would result in Apple having $13.52 in diluted EPS by the end of 2030 and Taiwan Semiconductor having a jaw-dropping $57.08. That's a substantial increase from today's values.

AAPL EPS Diluted (TTM) data by YCharts

To find out how much that would be worth for each company, we need to multiply the EPS figure by the total number of shares outstanding. Then, we'll have to assign it an earnings multiple. Using today's valuation figures (Apple at 36 times earnings and Taiwan Semiconductor at 28), that would give Apple a market cap of $7.2 trillion and Taiwan Semiconductor a market cap of $8.3 trillion by 2030.

Will that happen? I'm not sure. Those are massive growth assumptions baked into Taiwan Semiconductor's stock that may not pan out. But if they do, I think it has a strong chance of surpassing Apple in market cap by 2030.