Nvidia (NVDA 3.67%) seems like it has delivered a constant string of positive news for investors over the past few years. CEO Jensen Huang just delivered another piece of fantastic news for Nvidia shareholders, and potentially quelled the fears of investors who are concerned we're in an artificial intelligence (AI) bubble.

Nvidia stock still looks quite attractive even following strong third-quarter earnings, and I think it's a great stock to buy now, especially with a visionary CEO like Huang at the helm.

Image source: Nvidia.

Nvidia is sold out of data center GPUs

In its Q3 earnings release, CEO Jensen Huang stated, "Blackwell sales are off the charts, and cloud GPUs are sold out." That's huge news for Nvidia shareholders, as it shows that demand still outpaces supply. When that occurs, Nvidia can maintain pricing power, as it controls the stream of one of the hottest products in the world.

Additionally, Nvidia exceeded its own expectations for the quarter. Management gave guidance of $54 billion for Q3, but Nvidia blew those forecasts out of the water. It delivered $57 billion in revenue and gave projections for Q4 revenue of $65 billion. Most of that growth came on the back of its data center division, which encompasses the graphics processing units (GPUs) and other equipment needed to run artificial intelligence workloads. Data center revenue was $51.2 billion, up 66% from last year's total.

NASDAQ: NVDA

Key Data Points

Another huge story Nvidia revealed is that its leading Blackwell chips are now entirely made in America, with the chips coming from Taiwan Semiconductor's Arizona facility. This helps Nvidia avoid tariff burdens and control its supply chain more tightly.

All of these results help justify Nvidia's valuation and prove that it's still one of the best stocks to own in the market. But has it become too expensive?

Nvidia's valuation

With a fast-growing stock like Nvidia, using trailing earnings metrics isn't a smart idea, as it includes quarters where it was significantly smaller. Instead, I prefer to use forward-facing metrics, although there is some danger in this because it uses projections instead of actual reported results. However, it's the best tool we have to measure a rapid grower like Nvidia.

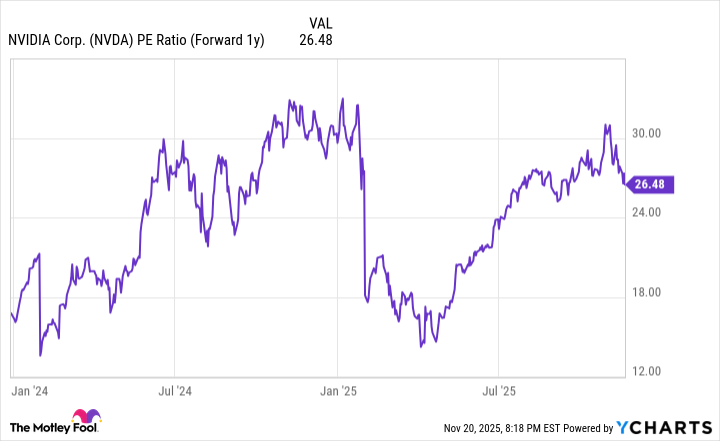

Despite claims that Nvidia's stock is expensive and overvalued, it's really not. Nvidia trades for 26.5 times next year's earnings, which places it in the same ballpark as other big tech companies.

NVDA PE Ratio (Forward 1y) data by YCharts

Compared to its big tech peers, Apple and Microsoft, which trade at 29 and 26 times next year's earnings, respectively, Nvidia's stock doesn't seem so bad. This comparison is even more exaggerated by the fact that Nvidia is growing substantially faster than Apple and Microsoft and expects that growth to stretch out for a few years.

During its Q2 conference call, Nvidia claimed that the global data center capital expenditure bill for 2025 would reach $600 billion. By 2030, they expect it to increase to $3 trillion to $4 trillion. That's a huge rise, and if it comes true, would result in Nvidia maintaining its unprecedented growth through 2030.

The reality is that the AI arms race isn't slowing, even if the market is growing concerned with the spending levels. Many big tech CEOs have said the risk of underbuilding AI computing capacity is far greater than overbuilding it, and with Nvidia being the arms dealer in the AI race, it's sitting in an excellent position.

I think Nvidia will continue to be a must-own investment over the next few years, and the price tag really isn't all that expensive if you put it in context with its growth and other big tech companies.