Walmart (WMT +2.06%) just reported another solid all-around quarter, especially considering many retailers are struggling due to cost-of-living increases, which is straining consumer spending and hitting the lower and middle classes particularly hard. Walmart is on track to beat the S&P 500 for the second consecutive year and has more than doubled over the last three years, compared to a 65% gain in the S&P 500.

Let's consider why Walmart continues to perform as well as a red flag that the company discussed on its latest earnings call -- and whether the dividend-paying Dow Jones Industrial Average component is a worthwhile investment now.

Image source: Getty Images.

Walmart is in a league of its own among major retailers

There's an exhaustive list of consumer-facing companies that are struggling. To name a few -- RH and Target are hovering around five-year lows. Home Depot is on track to deliver its third consecutive year of lower earnings and is warning about a prolonged slowdown in home improvement spending due to affordability challenges and a sluggish housing market.

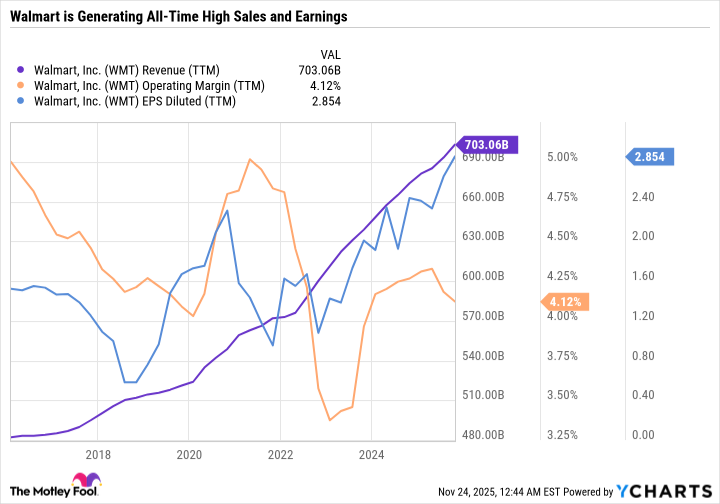

And yet Walmart continues to deliver good results -- growing sales and earnings while maintaining a solid operating margin, given its high volume.

WMT Revenue (TTM) data by YCharts

Walmart's results showcase the nuances of purchasing decisions. Often, consumers don't eliminate a purchase, but shift the source -- for example, cutting back on food spending by cooking from home instead of going to restaurants, or making coffee at home instead of going to Starbucks.

Walmart is capturing a significant portion of this widespread shift toward value. Consumers who typically frequent pricier outlets may shift some of that spending toward Walmart to save money. Walmart is only converting around $0.04 of every $1.00 in sales into operating income.

Therefore, the Walmart value proposition is accurate in the sense that Walmart offers customers good deals. Walmart can afford to have razor-thin margins and undercut the competition because it has more sales than any other retailer in the world.

Walmart has also made it easier than ever to shop, offering convenient options like home delivery through Walmart+ and a significantly improved curbside pickup program. On the Nov. 20 earnings call, Walmart said that membership income generated from Walmart+ continues to grow by double digits.

Walmart is leveraging artificial intelligence (AI) in its supply chain and operations, as well as for customers through a recently announced partnership with OpenAI, which will enable shopping through ChatGPT.

All in all, Walmart continues to leverage its strengths by delivering value through low prices and convenience to its customers.

NYSE: WMT

Key Data Points

Lower-income consumers are getting hit the hardest

Despite these strong results, Walmart has not shied away from the impact of industrywide challenges on its performance. Low-income customers are spending less, which is a headwind for Walmart. But at the same time, it's in a good spot to take market share if these conditions persist. Walmart CFO John Rainey said the following on Walmart's third-quarter fiscal 2026 earnings call:

But when we look at the low-income cohort versus the middle and higher-income, we have seen some moderation in spending in the low-income cohort. And that's consistent with things you've seen from a macro perspective in October, wage growth. The disparity in wage growth between those cohorts was as large as it's been in almost a decade.

Like Home Depot, Walmart is openly discussing the affordability crisis. It also stated that if these conditions persist, consumers will seek even greater value, which is why Walmart is gaining market share.

Walmart isn't worth an ultra-premium price

Walmart's commentary showcases the dichotomy between a struggling consumer economy and rising corporate profits. Asset values like stocks, gold, and housing are hovering around all-time highs. And yet, goods and services are becoming less and less affordable relative to wages. That's an alarm for the economy and some stocks, but not Walmart.

As impressive as Walmart's results have been, this is still a company that is only guiding for year-over-year net sales growth of 4.8% to 5.1% and a 4.8% to 5.5% increase in operating income. So it's not like Walmart is growing at a breakneck pace.

Walmart has accelerated its dividend increases in recent years. But because the stock has done so well, the stock only yields 0.9%, making it a poor source of passive income.

Perhaps the most significant factor weighing on the stock is its valuation. Walmart has historically commanded a premium valuation due to its industry leadership and recession resistance -- with a 10-year median price-to-earnings (P/E) ratio of 28.6. But Walmart's P/E is now a staggering 36.9 -- making it a textbook example of a great company that's expensive for the wrong reasons. Walmart has gotten so pricey that it now commands a higher forward P/E ratio than Nvidia.

In sum, investors will have to pay a premium price for Walmart, which may still be worth it if you're looking for a company that can continue to execute well if economic conditions worsen. However, most investors are probably better off going with top growth stocks at compelling prices or less expensive value stocks with high yields to generate passive income.