The bull-and-bear debate over Lockheed Martin (LMT +1.05%) and defense stocks in general rages on and is unlikely to be resolved in the near term. While the bulls emphasize the conducive environment for defense stocks, the bears are asking serious questions about the long-term margin profile of these businesses. It's a fascinating debate that every investor should consider before investing.

The Bulls' case for Lockheed Martin

Many investors love defense stocks for their "defensive" profile. Their customers, governments, and defense departments are about as reliable as you can find. Moreover, there's even an element of countercyclicality in their end markets, as governments sometimes boost defense spending during economic slowdowns.

Image source: Getty Images.

Meanwhile, there's no shortage of geopolitical tension worldwide, and the decision made by member countries at a NATO summit earlier this year to increase defense spending to 5% of gross domestic product (GDP) by 2035 supports long-term demand. That's not to mention the record-breaking U.S. defense budget request of over $1 trillion for 2026.

In this environment, investors can buy into the world's leading defense contractor trading at slightly less than 15.5 times estimated 2026 earnings, with a 3.1% dividend yield and a record $179 billion backlog representing more than two years' worth of sales.

The bears' case for Lockheed Martin

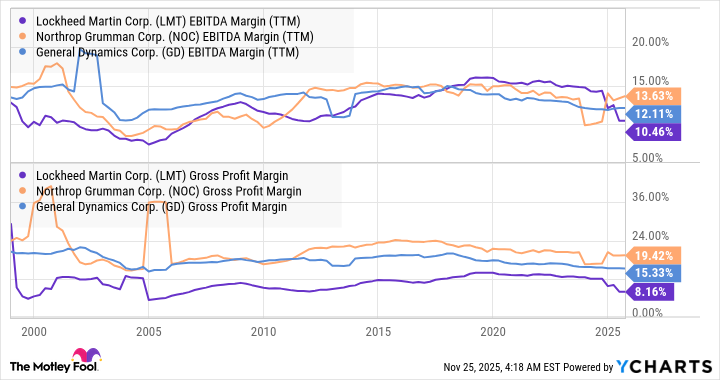

In response, the bears will argue that revenue is one thing, but margins are another. The simple fact is that many defense companies, including Lockheed Martin, have faced severe margin challenges in recent years, mainly due to fixed-price development programs that have significantly overrun cost estimates.

It's challenging to determine whether these issues are transitory and related to the supply chain crisis, causing severe material inflation after contracts were agreed upon, or whether there's a more structural, long-term issue at play, in which governments are better at utilizing their bargaining position.

Data by YCharts.

Lockheed CEO Jim Taiclet was asked about the issue of fixed-price programs on an earnings call in 2024, and he discussed "a monopsony environment here, meaning there's a single buyer for the most part, for almost everything that we make or Boeing Defense makes or General Dynamics makes." He went on to describe an environment where competitors "feel that there are must-win programs for them that they will take tremendous risk on cost and pricing and tremendous cost on the ability to technically deliver these capabilities."

Taiclet may have been referring to Boeing, which won three major fixed-price contracts over Lockheed in 2018, two of which (the T-7 Red Hawk training aircraft and the MQ-25 Stingray refueling drone) have generated significant losses.

NYSE: LMT

Key Data Points

As if to reinforce the point about margin pressure, it's hard not to think that the cost overruns and delays on the F-35 fighter (a cost-plus contract for Lockheed) influenced the decision to give Boeing the Next Generation Air Dominance (NGAD) F-47 contract over Lockheed.

Before you buy Lockheed Martin stock

A favorable end market environment for revenue, or possibly an unfavorable market for margins: Investors need to weigh the pros and cons before making a purchase, and also consider which factor is more lasting. That's the conundrum facing investors in stocks like Lockheed Martin these days.