For much of the last three years, artificial intelligence (AI) has been the hottest thing since sliced bread on Wall Street. With multibillion-dollar AI spending deals being announced on a seemingly regularly basis in 2025, it's no wonder we've witnessed AI stocks soar.

The heartbeat of the artificial intelligence revolution is Nvidia (NVDA 1.44%), Wall Street's largest publicly traded company, and the first to reach a $5 trillion valuation. While institutional investors have benefited immensely from Nvidia's 1,120% gain since 2023 began, retail investors are on board, too!

Favored retail investing platform Robinhood regularly updates its "100 Most Popular" leaderboard, which lists the 100 securities, including exchange-traded funds, that Robinhood customers most commonly hold. Though AI stocks and members of the "Magnificent Seven" litter the top of its leaderboard, the No. 1 holding of retail investors, having supplanted electric-vehicle maker Tesla earlier this year, is Nvidia.

Image source: Getty Images.

While it's easy to become enamored with Nvidia's well-defined competitive advantages, the persistent selling of Nvidia stock by billionaire Philippe Laffont of Coatue Management might encourage retail investors to think twice about buying or holding Robinhood's No. 1 stock.

Nvidia becoming the world's first $5 trillion company didn't happen by accident

Nvidia's claim to fame is its graphics processing units (GPUs), which serve as the brains of AI-accelerated enterprise data centers. The company's three premier generations of AI-GPUs (Hopper, Blackwell, and Blackwell Ultra) have been consistently backlogged, demonstrating that enterprise demand for these chips is very real.

Building on this point, CEO Jensen Huang's company has benefited from the demand for AI infrastructure sharply outpacing supply. The law of supply and demand states that when demand for a good or service significantly outstrips its supply, prices will rise until demand tapers. In Nvidia's case, it's been netting $30,000 to $40,000 for each of its high-powered AI-GPUs, which is a significant premium over its external competitors. Nvidia should enjoy phenomenal pricing power for as long as GPU scarcity persists.

NASDAQ: NVDA

Key Data Points

Nvidia's success is also a reflection of its hardware outperforming its peers. From Hopper through Blackwell Ultra, no external competitors have come particularly close to surpassing Nvidia's chips on a compute basis. Huang intends to keep it this way, with his company on schedule to introduce a new advanced AI chip annually.

Large-scale deals have fueled a fire under Nvidia's shares, as well. For example, on Sept. 22, Nvidia and privately held OpenAI announced a strategic partnership that'll see the latter deploy at least 10 gigawatts (GW) of AI data centers using AI-GPUs from Nvidia. In return, Nvidia will invest up to $100 billion in OpenAI on a progressive basis. The first GW will be deployed in the second half of 2026 and feature Nvidia's next-gen Vera Rubin chip, which will run on an all-new processor (Vera).

Tying everything together is Nvidia's CUDA platform. This unsung hero is the toolkit developers use to get as much compute as possible out of their Nvidia GPUs, as well as to build and train large language models. CUDA ensures that GPU buyers remain loyal to Nvidia's products and services for a long time to come.

In other words, Nvidia's ascent to become the world's largest publicly traded company didn't happen by accident. But the actions of billionaire Philippe Laffont strongly suggest Nvidia's parabolic ascent may be nearing an end.

Image source: Nvidia.

Billionaire Philippe Laffont has dumped 80% of Coatue's Nvidia stake

No later than 45 calendar days following the end of each quarter, institutional investors with at least $100 million in assets under management (AUM) are required to file Form 13F with the Securities and Exchange Commission. This filing provides investors with a snapshot detailing which stocks Wall Street's savviest money managers purchased and sold in the latest quarter. Laffont closed out September with close to $40.8 billion in AUM, meaning his fund handily meets the filing requirement.

As of March 31, 2023, Coatue Management held 49,802,020 shares of Nvidia stock. Keep in mind that this figure has been adjusted to account for Nvidia's historic 10-for-1 forward split, which took place in June 2024. By Sept. 30, 2025, this position has decreased by approximately 80% to 9,870,743 shares, and includes the sale of more than 1.6 million shares in the latest quarter.

Considering how much Nvidia stock has rallied since Laffont's stake in the company peaked more than two years ago, profit-taking is a viable and logical explanation for his near-persistent selling of shares. But profit-taking may not be the only reason he's heading for the exit.

Although Coatue's billionaire boss is a big fan of high-growth tech stocks and next-big-thing innovations, I'd argue he also recognizes the importance of historical precedent.

For instance, history has repeatedly shown that game-changing technologies require considerable time to mature. Hyped innovations, such as the internet, nanotechnology, 3D printing, blockchain technology, and the metaverse, all eventually saw their bubbles burst. Investors consistently overestimate the adoption, utility, and optimization timelines of new technologies, leading to bubbles and investor disappointment.

While Nvidia has reported robust sales growth and seemingly insatiable demand for its hardware, AI solutions are far from optimized at the enterprise level. Furthermore, it's not yet clear whether most businesses are generating a positive return on their AI investments. If an AI bubble forms and bursts, as history suggests it will, the most-direct beneficiary of the AI revolution (Nvidia) would be among the hardest hit.

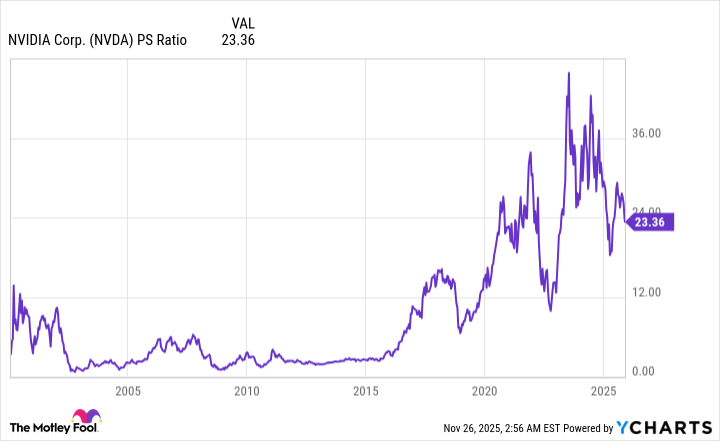

Historical precedent also draws a clear line in the sand when it comes to stock valuations.

NVDA PS Ratio data by YCharts. PS Ratio = price-to-sales ratio.

Over the last three decades, companies that have led next-big-thing innovations forward have commonly peaked at price-to-sales (P/S) ratios of 30 to 40. In early November, prior to Nvidia announcing its fiscal third-quarter operating results, its P/S ratio, once again, surpassed 30. Even with a scorching-hot sales growth rate, Nvidia's valuation appears unsustainable, based on what history can teach us.

Concerns exist beyond history, as well. For example, a whopping 61% of Nvidia's fiscal third-quarter sales came from just four direct customers. If one or more of these clients run into issues or slow their ordering, Nvidia could struggle.

The favorite stock of retail investors on Robinhood might not be the slam-dunk investment it's made out to be.