Nvidia (NVDA +1.08%) has been at the top of the artificial intelligence (AI) investing hierarchy since 2023. However, there could be a significant shift occurring.

Up until a few days ago, it appeared that there were only a handful of options for AI hyperscalers to choose from when outfitting their data centers with parallel processors. Nvidia's graphics processing units (GPUs) have been by far the most popular choice, and AMD's GPUs have also captured a sliver of the market. Another option that the largest data center operators have pursued was to partner with Broadcom (AVGO 2.87%) to develop custom AI accelerators -- called application-specific integrated circuits -- that are optimized for a particular type of workload.

However, news broke recently that Alphabet (GOOG 0.83%) (GOOGL 0.90%) may sign a deal to sell a large quantity of its tensor processing units (TPUs) that it collaborated with Broadcom to design to Meta Platforms. Such an agreement could herald the arrival of a new competitor to the computing hardware market, which is why purchasing these three stocks now may make more sense than adding shares of Nvidia.

Image source: Getty Images.

Three companies are set to benefit

The news articles regarding the possibility that Meta will buy TPUs from Alphabet recognize that it is just that: a possibility. The companies have not made a firm public comment on the matter, nor has a clear dollar figure been floated, although it's reported to be in the range of billions of dollars. With all that said, there are three companies in the TPU value chain, and I think each of them is a worthwhile buy right now.

The most obvious company that will benefit is Alphabet.

Alphabet gets the majority of its revenue ($74 billion of its $102 billion in Q3) from advertising. Advertising is not a steady business -- it rises and falls depending on the strength of the consumer and businesses' willingness to spend on ads. The company also has a cloud computing business that is thriving thanks to a general shift toward cloud workloads and new artificial intelligence workloads coming online.

NASDAQ: GOOGL

Key Data Points

Up until now, if companies wanted to make use of TPUs for their processing needs, their only option was to rent time on them through Google Cloud. They couldn't buy any. If Alphabet starts selling its TPUs, that would open up a new revenue stream that investors haven't yet accounted for. This is why Alphabet's stock soared by a double-digit percentage in the days after the news broke about the possible Meta deal.

Broadcom would also be a huge beneficiary if these sales occur, as Alphabet pays the chip designer for every TPU it purchases. It's unknown if Broadcom would make more money if Alphabet decided to sell them to third parties, but custom AI chips have become a large part of Broadcom's business.

In its fiscal 2025 third quarter, which ended Aug. 3, $5.2 billion of Broadcom's $15.9 billion in revenue came from AI-related sources. However, this division is rapidly growing; management expects $6.2 billion in AI revenue in fiscal Q4.

NASDAQ: AVGO

Key Data Points

If the Alphabet and Meta deal goes through, this number could skyrocket in 2026, enhancing Broadcom's financials accordingly.

The last company that would benefit from this deal is one of my favorites in the AI sector: Taiwan Semiconductor (TSM 0.64%).

NYSE: TSM

Key Data Points

Taiwan Semiconductor benefits regardless of who the ultimate winner is

Nvidia has been the clear-cut leader in the AI accelerator space up to this point, but its dominance could be slipping. However, all of these AI hardware providers are "fabless" chipmakers. They design chips, but they don't manufacture them in-house. Instead, they outsource that task to chip fabrication companies, and the largest of these by a wide margin is Taiwan Semiconductor.

This positions Taiwan Semiconductor as a neutral (but vital) player in the AI world. Its business will grow as long as there is increased spending in AI chips. If Nvidia's dominance slips and Broadcom's custom AI units take off, TSMC will benefit just the same.

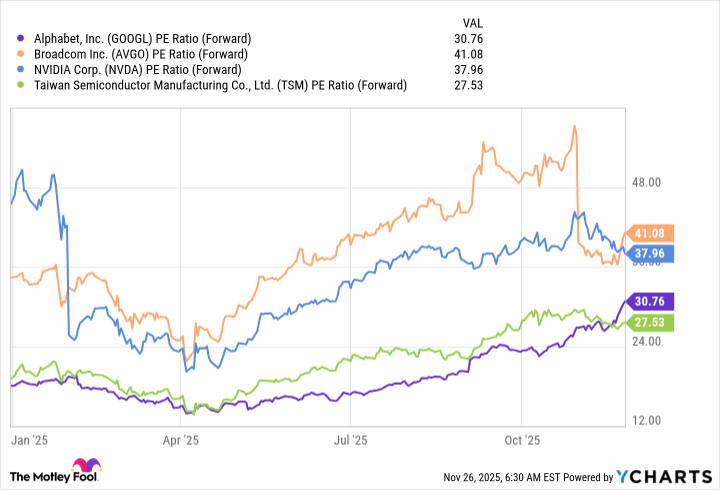

Despite its ability to benefit regardless of which companies' AI chips are in demand, TSMC's stock trades at a far lower premium than the other stocks discussed here.

GOOGL PE Ratio (Forward) data by YCharts.

Trading at 27.5 times forward earnings, TSMC shares are a great deal, and retail investors should buy them alongside Alphabet and Broadcom, particularly if Alphabet does begin selling its TPUs to other data center operators.

I still think Nvidia remains a strong investment pick, but if TPUs become available for widespread purchase, these three may become better buys.