Carnival (CCL +0.10%) is the longtime leader in the cruise industry. According to the website Cruise Market Watch, nearly 42% of all cruise passengers currently sail on ships owned by Carnival, but the company only claims about an estimated 36% of industry revenue.

More recently, Viking Holdings (VIK +0.84%) has emerged on the scene, drawing luxury-class passengers with smaller ships and a destination-focused approach to cruising. Although it holds a market share of just 0.8%, it claims 4.2% of the revenue earned in the industry. Still, does that advantage and other characteristics make Viking stock a better buy than Carnival? Let's take a closer look.

Image source: Getty Images.

The case for Carnival

Carnival's 42% market share makes it the ultimate generalist in the industry. Its mainstream brand caters to the general population, making it a more budget-friendly choice for many types of travelers. Nonetheless, it also owns regional, premium, and ultra-luxury brands, giving it a foothold in most cruise markets.

The company suffered during the pandemic because it was unable to sail for more than a year. Not only did it have to borrow heavily to stay in business, but it also took years to return to 2019 revenue levels.

Fortunately, cruise demand eventually recovered, and with record bookings, occupancy is at 105% in an industry that defines 100% occupancy at two people per cabin. With that, it has five more ships under construction.

As a result, Carnival generated $2.6 billion in free cash flow in fiscal 2025 (ended Nov. 30). This does not include money invested to build more ships. It also reduced its $26.6 billion in total debt by around $800 million over the course of the year.

That leaves its total debt well above the $12.3 billion in book value. Still, the 23% reduction in interest expense over the last year means the company can borrow under increasingly favorable terms.

NYSE: CCL

Key Data Points

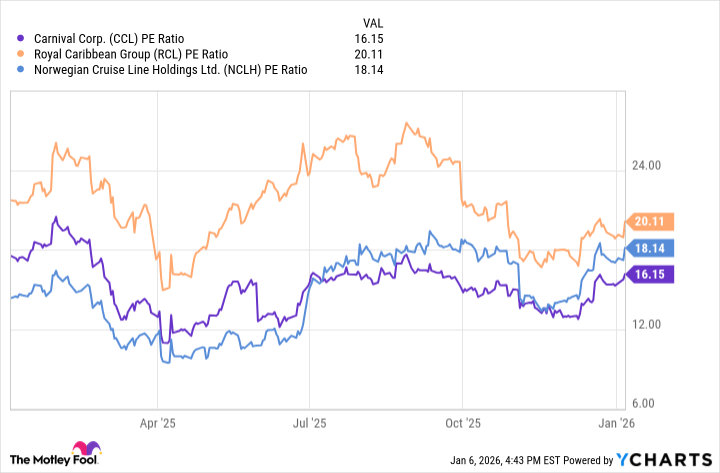

Amid these improving conditions, Carnival stock is up 30% over the last 12 months. Also, at just 16 times earnings, it sells at a lower price-to-earnings ratio (P/E) than either Royal Caribbean Cruises or Norwegian Cruise Line Holdings. Such a valuation, along with ships sailing above capacity, suggests Carnival stock could continue to move higher.

CCL PE Ratio data by YCharts.

Why investors might choose Viking stock

Despite that potential, Viking has succeeded by taking a much different path. Its longboats do not offer some of the more ostentatious offerings of Carnival's much larger ships. Instead, it emphasizes education and longer port stays. With its ships' ability to navigate rivers, it can also compete in areas where Carnival cannot sail.

Moreover, it offers a luxury experience, with its generally higher fares including excursions and other benefits that are typically treated as add-ons on competing cruise lines.

And economic downturns do not tend to affect that cohort as profoundly, making Viking more recession-resistant than competitors. With this approach, it only allows two people per cabin but commands 96% capacity despite that limitation.

Furthermore, Viking did not launch its initial public offering (IPO) until May 2024. Thus, we do not have figures on how it stayed afloat during the pandemic. Nonetheless, its total debt of around $5.4 billion is arguably more manageable than Carnival's debt load when considering its book value, which is also $5.4 billion.

Amid high demand, Viking generated $674 million in free cash flow over the last year, which has fallen as it increases its investments in building more ships. But that should pay off as it seeks to meet the heavy demand for its cruises.

NYSE: VIK

Key Data Points

Investors have responded well to its approach, and the stock is up 70% over the last year. While its 35 P/E ratio is significantly higher than Carnival's and that of other competitors, Viking's strengths and greater recession resistance arguably make it worth that premium.

Carnival or Viking?

Choosing between these stocks may come down to your preferred investing approach.

If you're seeking safety, a low 16 P/E and a large market share might make Carnival stock more attractive. Bookings remain strong, and the company has been able to manage its huge debt load, reducing it while it expands its fleet.

However, if you can take on more risk, Viking could have greater potential despite its higher P/E. A recession-resistant business model makes it less likely that a downturn will interrupt its growth. Moreover, its smaller ships allow it to sail to more destinations, meaning Viking could capture a larger share of the cruise business over time.