Finding bargains when the stock market is near an all-time high isn't as easy as when the market is at its lows. But there are still plenty of stocks that I would consider bargain buys with strong upside. I think a bull run could occur any day for these three stocks, making them great ones to buy now.

The three that I have on my watch list are Meta Platforms (META 0.04%), Adobe (ADBE 2.62%), and The Trade Desk (TTD 2.03%). Each is in bargain territory and can be bought with confidence.

Image source: Getty Images.

Meta Platforms

Meta Platforms, formerly known as Facebook, changed its name a few years ago to signal to investors that it was focusing on the metaverse, although that business never developed as it had hoped. All the while, its social media business was still going strong and paying for its huge metaverse investments.

That draws parallels with what Meta is doing with artificial intelligence (AI) right now. Management is using nearly all of its cash flow to fund data centers so it can continue to train and improve its AI models. But unlike the metaverse disappointment, investors are already starting to see some payoffs, with Meta reporting more time spent on the platform by users and increased ad conversions due to some generative AI technology powering the ads.

Wall Street seems to be focused only on how much management is spending on AI, which may be a valid concern. However, thanks to the pessimism, the stock is now valued at a fairly cheap forward-earnings price tag, although it may not be as cheap as the others on this list.

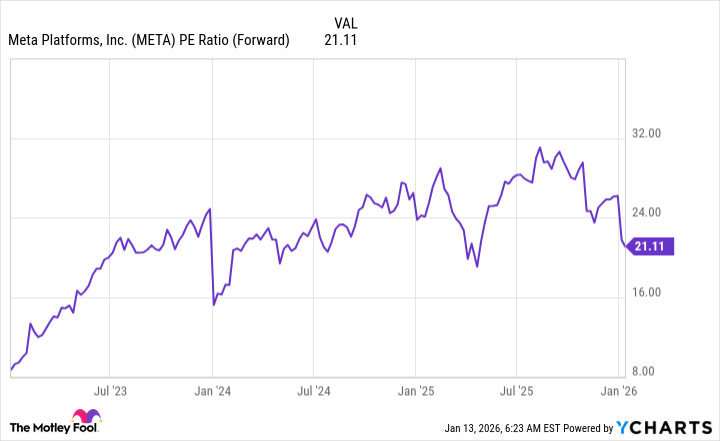

META PE Ratio (Forward), data by YCharts; PE = price to earnings.

At 21 times forward earnings, it's far cheaper than most of its big tech peers that trade for around 30 times forward earnings -- essentially a 30% discount. Furthermore, the S&P 500 trades for 22.4 times forward earnings, so it's cheaper than the broader market as well. This makes Meta an intriguing stock to buy on the dip, because it could offer monster returns if it reaches a valuation similar to its peers.

Adobe

Everyone is assuming that Adobe's business model is going to be replaced by generative AI. Image generation is improving, and some models generate images indistinguishable from real ones. The thought is that this could put many graphics designers out of business and harm the revenue stream of the Adobe software that they use.

NASDAQ: ADBE

Key Data Points

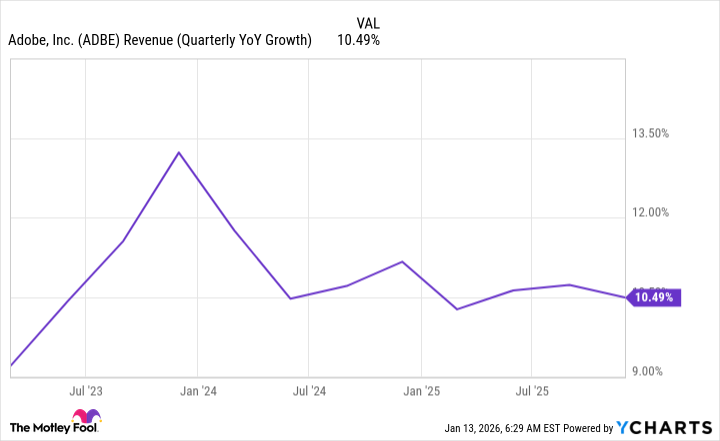

However, this thesis hasn't panned out. Adobe has openly embraced generative AI tools and has integrated them into its products to bolster designers' capabilities. And its revenue growth hasn't faltered from the low double-digit range since the AI race kicked off in 2023.

ADBE Revenue (Quarterly YoY Growth), data by YCharts; YoY = year over year.

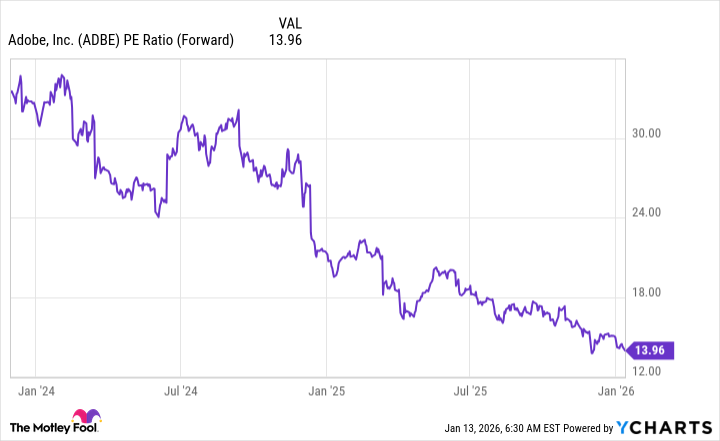

The market hasn't even considered what happens if Adobe is fine, and its stock has sold off to a dirt-cheap valuation as a result. Adobe is a true bargain right now. And if it can continue posting double-digit revenue growth, it's primed for a bull run.

ADBE PE Ratio (Forward), data by YCharts.

The Trade Desk

Lastly, The Trade Desk was among the worst-performing stocks in the S&P 500 during 2025. However, I think it has what it takes to bounce back during 2026.

The Trade Desk operates a buy-side ad platform, which helps businesses and services that want to advertise find the most opportune place on the internet. Its revenue growth has slowed from previous levels, but it still had a strong 18% gain during the third quarter.

NASDAQ: TTD

Key Data Points

Yet the stock trades at less than 18 times earnings -- far cheaper than the S&P 500. If The Trade Desk can deliver high double-digit growth throughout 2026 at a cheaper premium to the market, I think it could easily outperform most stocks and go on a bull run.