Coffee shop leader Starbucks (SBUX 0.28%) has disappointed investors over the past few years, but after cycling through four CEOs over the past four years, it might finally be turning around.

Shareholders have had high hopes for star CEO Brian Niccol, who joined the company just over a year ago, and his action plan looks like it might be starting to bear fruit. Is the stock a buy for 2026?

Image source: Starbucks.

One cup at a time

Starbucks is a massive coffee shop chain, with more than 41,000 stores worldwide. It's not easy to steer an organization that big and that entrenched in legacy systems, and the company has fallen behind in several important ways as global trends change. Wait times have been sluggish, prices are high, and the company's "third place" designation appeared outdated in the era of digitization.

Niccol is actually leaning into the third-place status, but he's revamping the company's image, processes, and equipment to make it relevant to today's customer. The company has been more deliberate with promotions, has changed its marketing story, and has put a lot of effort into improving its throughput to get beverages into customers' hands quickly without compromising on quality.

Starbucks may finally be demonstrating progress. In the 2026 fiscal first quarter (ended Dec. 28), revenue increased 6% year over year to $9.9 billion, while comparable sales were up 4% globally. Adjusted earnings per share declined 19% to $0.56. Niccol is heavily investing in the improvement strategy, which weighed on the bottom line, but he anticipates it will eventually lead to better margins and increased profitability when the investments pay off.

NASDAQ: SBUX

Key Data Points

Dividends, value, and valuation

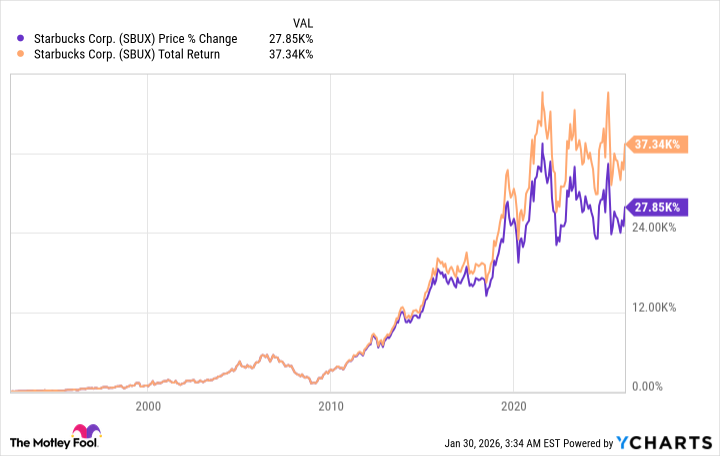

Starbucks has been an incredible market winner over time, gaining almost 28,000% since its debut on the stock market, and more than 37,000% when you include dividends.

Starbucks' dividend yields about 2.6% at the current price, and the company has raised it annually for the past 15 years.

There's a lot to like about how Niccol's plan it going, and there's certainly good reason to feel confident about the company's ability to reach its goals and get back to growth. Long-term investors and dividend investors are likely to be rewarded over many years.

However, one thing stopping me from giving a heartier recommendation is the stock's valuation. Investors were piling into the stock in anticipation of a strong report, and Starbucks stock trades at a P/E ratio of 78 today. That's rich for a company still trying to recover and without long-term high growth prospects. That valuation doesn't support high stock gains, and I suggest waiting for a better entry point to take a position.