Consumer stocks have long served as a steady, sometimes lucrative source of dividend income. The more successful ones benefit from a loyal customer foundation that fosters a consistent and growing profit base, ultimately translating into cash for shareholders.

Not all consumer stocks can maintain such streaks, meaning investors have to discern the businesses and financials of the stocks they own. These three stocks stand out as dividend growers on track to continue raising payouts, with a significant chance of stock price appreciation to add to one's total returns.

Image source: Getty Images.

1. Realty Income

Realty Income (O +0.29%) is a real estate investment trust (REIT) specializing in single-tenant commercial properties. Under such deals, the tenant covers taxes, insurance, and maintenance, ensuring steady cash flows.

Realty Income owns more than 15,500 such properties and boasts a client base that includes the likes of Home Depot, Dollar General, and Wynn Resorts. Also, with occupancy close to 99%, the company continues to acquire and develop additional properties.

Realty Income is also known as the "monthly dividend company," and true to that moniker, it has paid a dividend every month since it began offering payouts in 1994. It has also hiked that dividend at least one time annually since that year.

The payout now stands at $3.24 per share annually, giving it a dividend yield of 5.3%, far above the S&P 500 (^GSPC 0.09%) average of 1.1%. The payout hikes, combined with a depressed stock price, have raised the yield as high interest rates weighed on the stock.

NYSE: O

Key Data Points

However, the Federal Reserve has reduced interest rates in recent months. That should make more potential deals profitable, thereby raising Realty Income's profits and, likely, its stock price.

Investors should also know that Realty Income sells at just 15 times its FFO income, a measure of a REIT's free cash flow. Such conditions, along with its generous dividend, should help boost the stock over time.

2. Target

Target (TGT +2.47%) is one of America's best-known retailers. Its nearly 2,000 locations in all 50 states mean that more than 75% of Americans live within 10 miles of a Target location.

Admittedly, the company has struggled recently. Its upscale discount products seem to hold less appeal in an uncertain economy. Moreover, a seeming inability to reduce inventory has weighed on the stock, and the company's forays into and out of politics have managed to alienate both right-leaning and left-leaning shoppers.

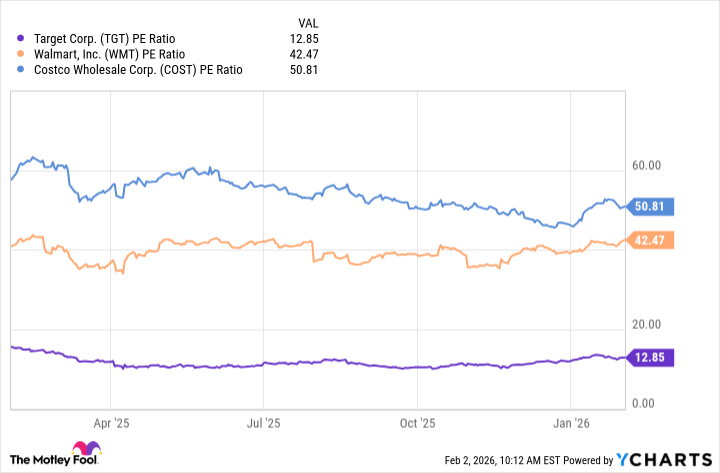

That brought about a collapse in the stock in the last few years. Consequently, its 13 P/E ratio is far below retail peers like Walmart and Costco.

TGT PE Ratio data by YCharts

NYSE: TGT

Key Data Points

Still, Target is a Dividend King by virtue of its 54 years of dividend increases. At $4.56 per share yearly, its dividend yields 4.3%. Also, since abandoning the Dividend King status could further damage the stock, the annual payout hikes will likely continue.

Additionally, Target just promoted COO Michael Fiddelke to the CEO position. Under Fiddelke, Target plans to invest $5 billion in capital expenditures for store remodels, technology, and improved infrastructure.

Such changes could help revamp the struggling retailer. When also factoring in the low P/E ratio and high dividend yield, Target looks increasingly like a stock investors should double up on right now.

3. Clorox

Consumers know Clorox (CLX +2.37%) best for its flagship cleaning products. However, Kingsford, Hidden Valley Ranch, and Burt's Bees are among the many brands under its umbrella.

Nonetheless, when the obsession with cleaning subsided as the pandemic began to wind down, investors soured on the stock. Moreover, higher inflation, a cyberattack on the company in 2023, and a recent enterprise resource planning (ERP) project brought significant disruption to its business, further spooking shareholders.

That brought a considerable stock price decline, but it also reduced its P/E ratio to 18, which is near a multiyear low. By the same token, it helped boost the dividend yield on its $4.96 per share annual payout to 4.4%. The streak of annual payout hikes going back decades also reinforces the dividend's stability.

NYSE: CLX

Key Data Points

Additionally, business conditions could improve soon. The aforementioned ERP implementation that slowed sales should help increase efficiencies moving forward, which could accrue to the company's bottom line.

Furthermore, if the performance of other consumer staples giants like Procter & Gamble is any indication, brand loyalties could work in Clorox's favor despite inflation concerns. When considering such factors and the dividend, Clorox could turn into a market-beating income and growth stock.