Canadian telecommunications and media company Quebecor (QBCR.F 1.20%) is on a dividend hot streak. Since early 2016, it's grown its quarterly payouts from 0.0175 Canadian dollars per share to CA$0.35 today. This 1,900% growth means that anyone who had invested CA$1,000 in 2016 and held on would be collecting a 17% annual yield on the initial investment.

These gains are, alas, in the past. But there are three reasons to think that this CA$11.8 billion Montreal-based company can at least match its previous dividend growth in the next 10 years, too. If I'm right, by 2036, this company could be paying a nearly 55.7% yield on cost to investors who buy today. If it materializes, this income stream could be life-changing.

Image source: Getty Images.

Why Quebecor could still deliver life-changing income

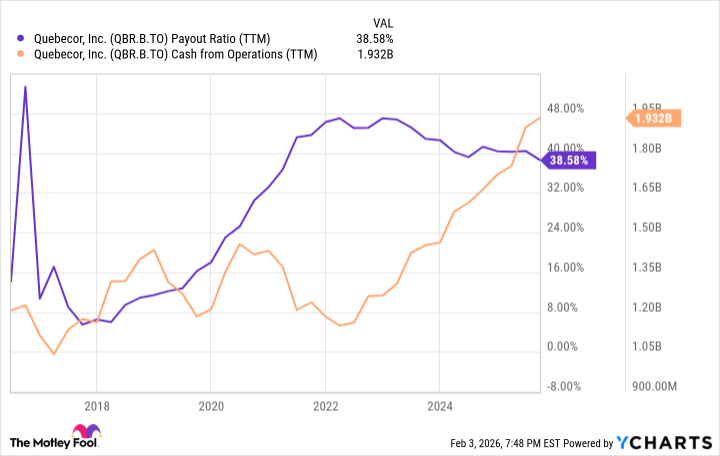

One quick way to gauge a company's ability to keep growing dividends is to examine its payout ratio, or the percentage of net income it's already spending on its dividend.

The lower a payout ratio, the more breathing room management has to grow its dividend. A company that's already spending 99% of net income to pay its dividend, for instance, has a lot less room to maneuver than a company that could double its dividend overnight and still be paying only a small percentage of net income on the dividend.

In Quebecor's case, the payout ratio has fallen over the last four years, as cash flow from operating activities (CFO) began surging in 2022 and recently overtook it.

Data by YCharts.

Rising CFO is great news for income investors because it's a measure of cash generated from regular business activities (not stock offerings, depreciations, or one-time windfalls). This shows that after paying regular expenses (salaries, overhead, cost of materials, etc.), the company just keeps raking in more cash.

All told, this company has grown its dividend by an average of 40% a year since 2016. If there's a wrinkle, it's that this growth has slowed since 2020, with the dividend rising by 75% overall since then. However, this came as management increasingly turned to share buybacks as a way to reward shareholders, with CA$179 million spent repurchasing shares over the last 12 months.

OTC: QBCR.F

Key Data Points

That's almost as much as the roughly CA$216 million that the company paid out in dividends last year. By winding down buybacks, management can almost double its dividend without going into debt or cutting investments elsewhere.

Given its history, it just might do that in 2026. But with the stock looking cheap with a price-to-earnings ratio of just 14 -- under half the S&P 500 -- management may be more tempted to continue buying shares. Income investors should consider following suit.