Year to date (as of Feb. 18, 2026), the State Street Consumer Staples Select Sector SPDR ETF (XLP 0.40%) is up just over 13%. That's the best start to a year this sector has had by far since it launched in late 1998.

Investors who have maintained diversification in their portfolio over the past three years are finally getting rewarded for their patience. But there's a growing concern from the sector having risen this far, this fast.

Source: Getty Images.

When the talk turns to market valuations, most people are talking about the tech sector or artificial intelligence (AI) stocks. And justifiably so. The State Street Technology Select Sector SPDR ETF is trading at about 27 times the next 12 month's earnings expectations, much above its long-term average.

But the rally seen in non-tech sectors is starting to raise valuation concerns there as well. After the recent rally in the consumer staples sector, it has a forward price-to-earnings (P/E) ratio of more than 23. That's the highest this sector has seen going back to just before the tech bubble burst.

Source: Yardeni Research.

Valuations could contract

A high valuation is probably more concerning for this sector than it is for tech. Stocks with high growth rates, like those seen with the Magnificent 7 stocks, can justify higher valuations. Consumer staples, on the other hand, constitute a traditionally low growth sector. It's steady and more defensive but usually doesn't do much to warrant a premium valuation. To get back in line with historical norms, valuations almost certainly need to contract. Stock prices usually need to fall for that to happen.

NYSEMKT: XLP

Key Data Points

But let's flash back to nearly 30 years ago when staples last traded at these levels.

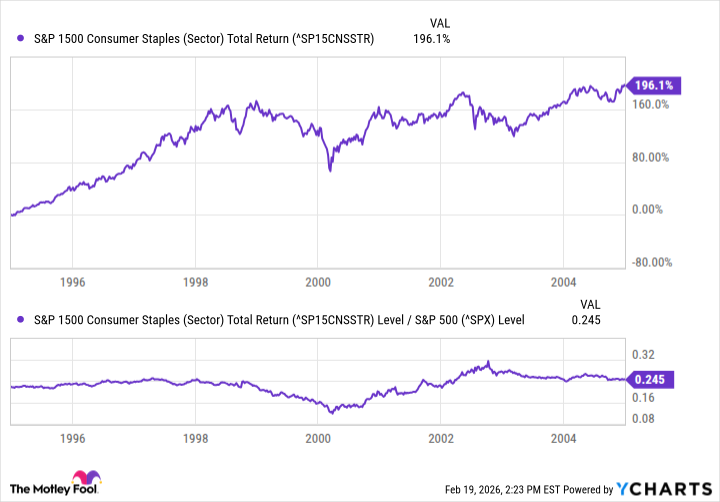

It turns out that peak valuations happened to coincide almost directly with peak stock prices. From late 1998 to early 2000, consumer staples stocks fell by nearly 40% from peak to valley. They also underperformed the S&P 500 for nearly two years.

^SP15CNSSTR data by YCharts.

The big difference between then and now might be that the staples sector was actually outperforming the S&P 500 in the years leading up to its downturn. In more recent times, staples had their last good year relative to the broader market in 2022. During the tech & AI boom of the past few years, they lagged badly.

So perhaps there's some more "catch-up" to be done by this sector today. But I don't want to discount the downside of investing in a sector that's at its most expensive level in nearly three decades. Earnings growth for consumer staples in 2025 was relatively flat, and 2026 isn't expected to be much better.

That suggests these stocks might be priced for perfection at the moment. That should serve as a warning to anyone considering chasing recent winners here.