Palantir Technologies (PLTR +0.19%) has emerged as a major beneficiary of rising U.S. defense spending. However, investors need to assess this opportunity in the context of the company's valuation. Congress has already approved a $901 billion U.S. military budget for 2026. Additionally, the Pentagon is seeking around $200 billion in supplemental funding amid the ongoing Iran conflict.

Importantly, the Pentagon plans to allocate over $153 billion toward modernization initiatives in 2026, including new ships, artificial intelligence (AI) technologies, and advanced weapons. This shift in spending directly benefits data analytics and enterprise AI player Palantir.

Image source: Getty Images.

Government spending is becoming software-driven

The Pentagon plans to adopt Palantir's Maven AI system as a "program of record," effectively making it a core military platform with stable, long-term funding visibility. That designation can help reduce revenue volatility for the company's government business.

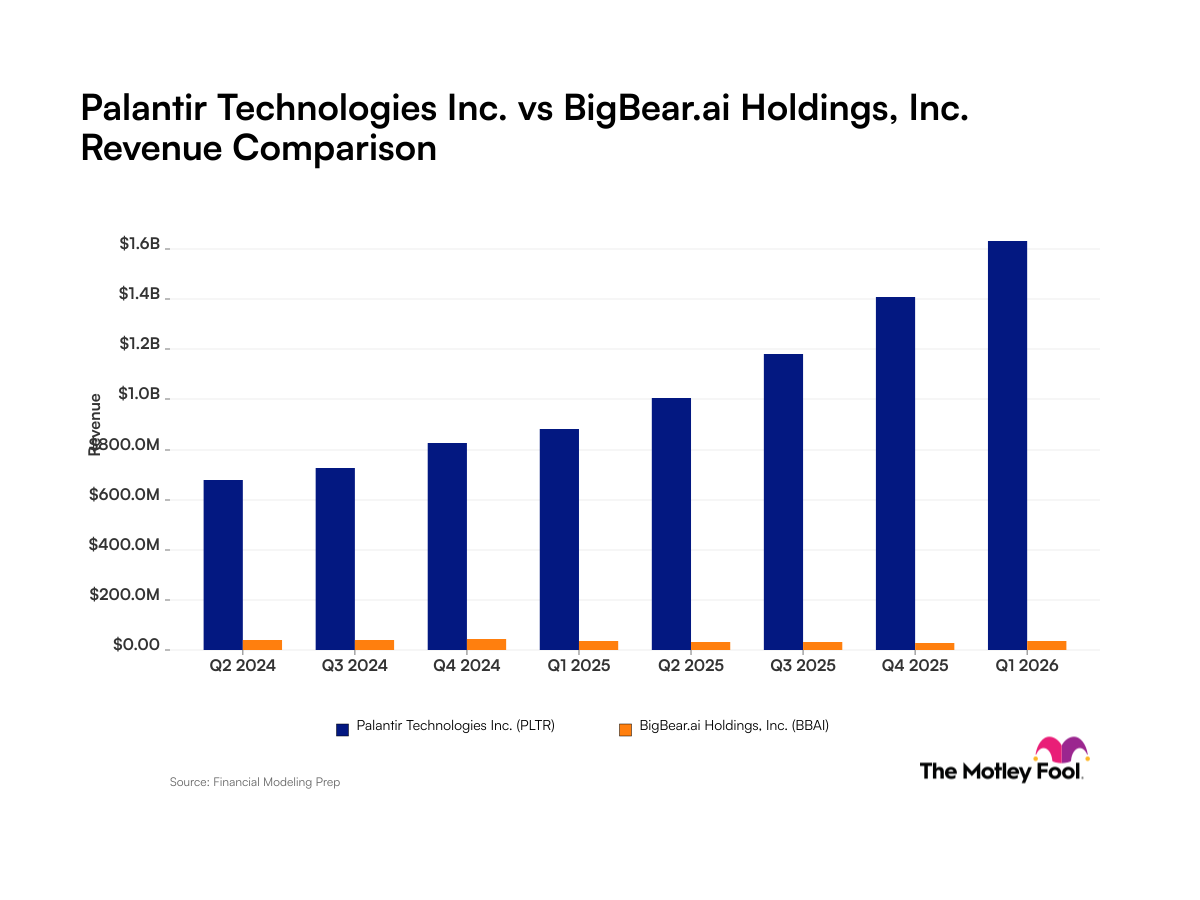

Palantir's government business is already gaining momentum. U.S. government revenue soared 55% year over year to roughly $1.8 billion in 2025, reflecting expanding deployments across defense programs. The company's Gotham and Maven platforms are increasingly embedded in real-time decision-making across battlefield data and target identification. Hence, these deployments are highly sticky and difficult to replace with competitor systems.

Palantir's Artificial Intelligence Platform (AIP) and proprietary ontology framework (which relates an organization's physical assets to digital counterparts) are also driving strong traction in the commercial segment. In fiscal 2025, U.S. commercial revenue soared 109% year over year to around $1.4 billion.

NASDAQ: PLTR

Key Data Points

Palantir also reported $4.3 billion in total contract value in the fourth quarter, up 138% year over year. The company's top 20 customers noted a 45% year-over-year increase in trailing-12-month revenue to $94 million in the fourth quarter. This highlights increasing success in cross-selling and upselling strategies.

Despite these strengths, Palantir's high valuation remains a concern. The company trades at over 77 times forward earnings, leaving limited room for execution missteps.

Hence, although Palantir remains well-positioned to benefit from the Pentagon's increased spending, long-term investors should adopt a disciplined approach and gradually build positions during pullbacks rather than buying aggressively at elevated levels.