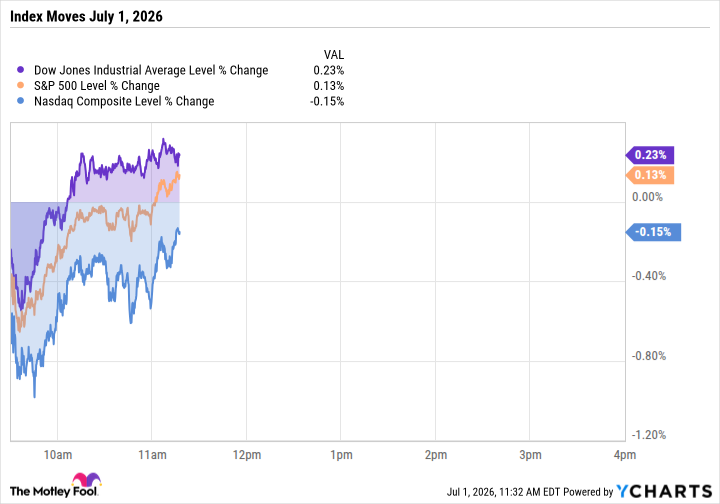

Wall Street is having a split personality on the first trading day of July. As of 11:29 a.m. ET, the S&P 500 (^GSPC +0.24%) gained 0.1% and the Dow Jones Industrial Average (^DJI +1.08%) added 0.2%. At the same time, the Nasdaq Composite (^IXIC -0.21%) was down by 0.2%.

None of these moves were big or dramatic, but plenty was going on underneath the composite stillness of the major index moves.

Cloud wars heat up as chip investors cash out

Meta Platforms (META -0.05%) surged 11.3%, adding $179 billion in market capitalization. Bloomberg reported the company is building a cloud business to sell excess AI computing capacity, kind of like when Amazon (AMZN -0.15%) started selling access to its oversized data centers 20 years ago. Is Meta building the Amazon Web Services (AWS) of the next era?

The gain made Meta the largest contributor to both the S&P 500 and Nasdaq Composite, single-handedly offsetting significant losses elsewhere in the tech sector. The direct losers in Meta's AI resale scenario are the neocloud companies that specialize in this exact kind of service. CoreWeave (CRWV -6.64%) dropped 14% on the news that a company with Meta's resources might be coming for its lunch.

Image source: Getty Images.

The iShares Semiconductor ETF (SOXX -4.99%) dropped 4.7%, with Micron Technology (MU -9.60%) leading the retreat at an 8.2% price drop. After more than tripling in Q2 2026, Micron investors apparently decided to lock in some profits at the start of Q3.

Caterpillar (CAT -4.68%) dragged on the Dow, falling 5.1% and subtracting 323 points from the index. The industrial giant gave back much of Tuesday's gains amid broader uncertainty over Middle East tensions and global growth concerns. Honeywell International (HON +0.81%) continued its post-spinoff slide, down 8.1% and costing the Dow another 118 points.

Fed Chair Kevin Warsh spoke in Portugal and stuck to his new playbook of not telling anyone what the Fed plans to do. He mentioned that "prices are too high," which sent Treasury yields higher.

And I can't skip the Strait of Hormuz, where the vessel backlog eased slightly to 385 ships from 485 on Tuesday. Only five transits occurred in the past 24 hours, though. Others are going back in dock to unload their goods and wait for calmer political waters before trying again.

Dow Jones Industrial Average

Key Data Points

The Week Ahead

The second half of 2026 is off to a bumpy start, which shouldn't surprise anyone after the first half's volatility. The Dow gained 8.9%, the S&P 500 rose 9.6%, and the Nasdaq climbed 12.8% through June, all experiencing painful drawdowns along the way.

Meta's cloud ambitions add a new wrinkle to the AI infrastructure story. Big tech companies have collectively spent over $700 billion on AI this year, and now they're looking for ways to monetize that investment beyond their core businesses. Selling spare computing power is one answer.

Economic data releases will drive market sentiment at the end of another shortened market week. Thursday brings the June unemployment report, which traders will scrutinize for clues about Fed policy. Wednesday's independent jobs report from Automatic Data Processing (ADP +4.47%) came in light at 98,000 private payroll additions versus 110,000 expected, suggesting the labor market may be cooling.