This has been a rough year for some artificial intelligence (AI) stocks. While there have been some huge winners, there have also been several major losers. One of the bigger winners has been Taiwan Semiconductor Manufacturing (TSM +0.23%), up nearly 50% this year. While it sold off on July 1, like all other AI stocks, it's still only down around 7% from its all-time high, after setting a new high just days ago.

The same cannot be said for other AI stalwarts, as Nvidia is down 16% from its all-time high, Alphabet is down around 10%, and Micron Technology is down around 15%. Taiwan Semiconductor is holding strong, but does that make it the ultimate AI stock to buy and hold? Let's take a look.

Image source: The Motley Fool.

The AI market depends on Taiwan Semiconductor

I think it's safe to say that without Taiwan Semiconductor, the artificial intelligence (AI) build-out would look far different. TSMC, as it's known, operates a logic chip foundry, and several of the world's biggest tech companies are clients. Major computing unit providers like Nvidia, Advanced Micro Devices, and Broadcom utilize TSMC's foundry services, making it vital to the AI build-out.

Taiwan Semiconductor is also the dominant force in the foundry world. Motley Fool research estimates that Taiwan Semiconductor generates 72% of the world's chip foundry revenue. That's outright dominance and demonstrates its overall importance. What's also really critical is increased industry spending, and that's likely coming.

NYSE: TSM

Key Data Points

Nvidia told investors during its latest conference call that it expects AI hyperscalers' data center capital expenditures to reach $1 trillion in 2027, up from about $650 billion in 2026. That all plays into the larger, long-term projection of $3 trillion to $4 trillion in annual data center capital expenditure by 2030.

If that pans out, Taiwan Semiconductor really doesn't care which computing unit becomes dominant or whether it's a mix, because odds are high that TSMC is making the chips powering those devices. This puts Taiwan Semiconductor in a vital position, which is why it doesn't sell off as deeply as its peers.

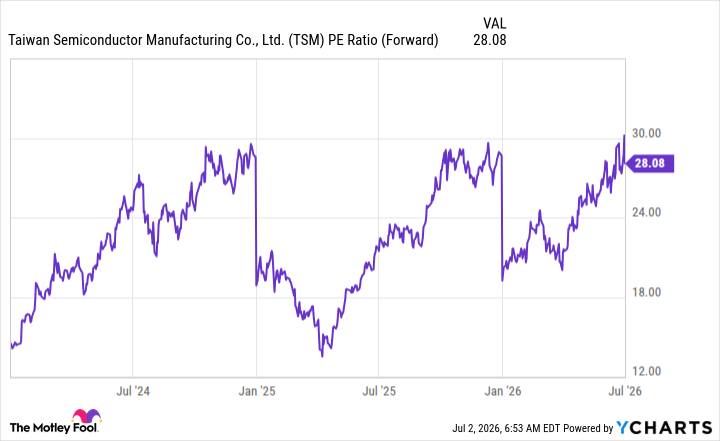

TSM PE Ratio (Forward) data by YCharts

However, you have to pay to own the stock, as the market has recognized its importance and now charges a premium valuation. At 28 times forward earnings, Taiwan Semiconductor isn't cheap, but it's also not terribly expensive considering its growth track record.

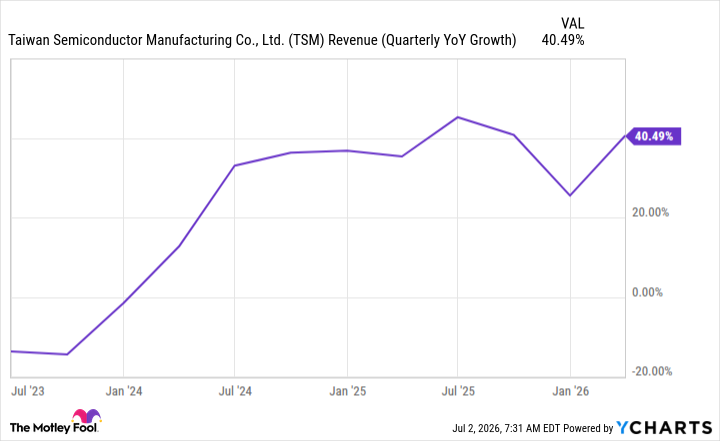

TSM Revenue (Quarterly YoY Growth) data by YCharts

Overall, I think Taiwan Semiconductor is one of the best stocks to buy and hold for the duration of the AI build-out. There's still plenty of growth left in the AI space, and buying shares of Taiwan Semiconductor could be a pretty surefire way to capitalize on this industry's growth.