Shares of Brinker International (NYSE: EAT) recently hit a new 52-week high. Let's take a look at how the company got there and whether clear skies remain in the forecast.

How it got here

The name Brinker International may not ring a bell, but the owner of the Chili's and Maggiano's restaurant chains continues to buck sector weakness and truck higher.

Rival Ruby Tuesday (NYSE: RT) is in the midst of closing 27 underperforming locations and tightening spending, while the struggle of DineEquity's (NYSE: DIN) IHOP franchise is evident in the 1% same-store sales drop in its most recent quarter.

On the flip side, casual-dining chains Buffalo Wild Wings (Nasdaq: BWLD), Darden Restaurants (NYSE: DRI), and Brinker have figured out the magic formula to growth despite rising input prices. First, these companies have worked hard to either remodel or make their restaurants visually appealing and welcoming to customers. Also, all three have a good mix of product on their menus, which keeps customers coming back. Traffic is growing nicely for all three companies.

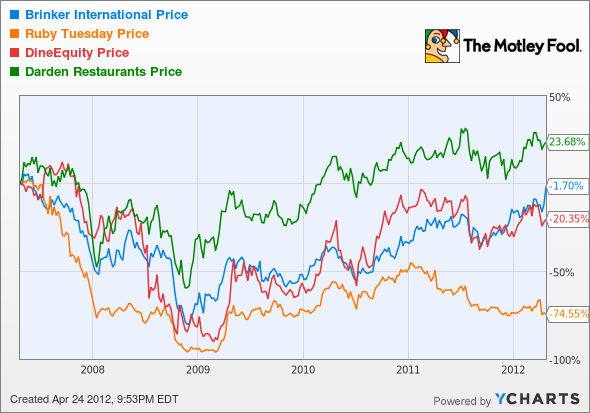

How it stacks up

Let's see how Brinker International stacks up next to its peers.

As you can see, owning restaurant chains hasn't exactly been a profitable venture in most cases over the past five years.

|

Company |

Price/Book |

Price/Cash Flow |

Forward P/E |

5-Year Revenue CAGR |

|---|---|---|---|---|

| Brinker International | 6.7 | 8.8 | 14.4 | (7.8%) |

| Ruby Tuesday | 0.8 | 3.8 | 11.8 | (0.6%) |

| DineEquity | 8 | 7.2 | 11 | (12.7%)* |

| Darden Restaurants | 3.7 | 8.8 | 12.4 | 5.6% |

Source: Morningstar. CAGR = compound annual growth rate. *Three-year CAGR used due to merger in 2008.

I give these metrics a collective "Yuck!" These numbers put into perspective how difficult it has been for restaurants to get customers back through their doors. When the recession hit, consumers' discretionary spending all but dried up. Darden Restaurants has been one of the industry's few bright spots recently, managing to grow despite weakness in its Olive Garden franchise. Brinker actually looks worse on paper than Ruby Tuesday, but its traffic growth of 5.8% at Maggiano's and 3.8% at Chili's saves it from the shortfalls currently being felt by Ruby Tuesday. DineEquity's large debt load and struggling IHOP franchise make it possibly the worst of the bunch.

What's next

Now for the real question: What's next for Brinker International? The answer, as with all restaurants, depends on whether the company can keep customers coming back with a favorable mix of products and drive new business while also raising prices high enough to offset rising input costs. It sounds like a challenge, but it appears Brinker is finally getting its act together.

Our very own CAPS community gives the company a two-star rating (out of five), with just 65.7% of members expecting it to outperform. I have yet to make a CAPScall on Brinker for two particular reasons.

First, I can't say I'm a huge fan of the restaurant sector because of rapidly changing consumer spending habits and the ebb-and-flow nature of the industry. If I wanted a cyclical company, I'd rather own something that has high growth potential or pays a higher dividend. Secondly, Brinker has repurchased 47% of its outstanding shares in just the past 10 years, which has the effect of boosting EPS while masking a lack of organic growth. Don't get me wrong; I'm impressed with Brinker's ability to drive traffic to its stores in the latest quarter, and I do appreciate the 2.3% yield, but I'd rather see the company put that money to work in marketing or upping its dividend, rather than more share buybacks.

I consider myself close to being able to pull the trigger on an outperform call, but I need one or two quarters more of outperformance before I'll be ready to give Brinker a clean bill of health.

Craving more input on Brinker International? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most. Click the links below to start today.

- Add Ruby Tuesday to My Watchlist.

- Add Brinker International to My Watchlist.

- Add Darden Restaurants to My Watchlist.

- Add DineEquity to My Watchlist.

- Add Buffalo Wild Wings to My Watchlist.