When it comes to energy resources, large parts of America are floating on a sea of oil and natural gas. New technologies such as hydraulic fracturing, horizontal drilling, and enhanced oil recovery (EOR) are creating record demand for oil and gas transportation and storage. Midstream master limited partnerships are a great way for average investors to tap into this energy bonanza with high yields, strong distribution growth, and capital gains. This article will point out two midstream partnerships (and one general partner) that offer investors strong catalysts for market-beating returns.

ONEOK Partners (OKS +0.00%) is very well situated to take part in some of the fastest-growing natural gas plays.

Oneok Investor Presentation

Its assets include pipelines serving important shale areas, including west and north Texas, Oklahoma, Colorado, Wyoming, and North Dakota. There are two main catalysts for ONEOK's future growth.

First is the completion of a five-year $5.2 billion-$5.6 billion investment program. In addition, the company has a $2 billion-$3 billion unannounced backlog of future investment projects it is considering.

As an example of how much potential demand there is for new gas pipelines, in North Dakota 30%-35% of natural gas produced is burned off. This is because of insufficient storage and transportation infrastructure. Fifty-six percent of ONEOK's investments are going toward building out infrastructure to stop this waste.

The second catalyst is the bottoming of ethane prices. Ethane is a natural gas liquid used in the petrochemical industry to make plastics. Prices have recently dropped because of a glut, and the partnership is facing decreased demand on its NGL pipelines.

The glut in ethane is projected to reverse beginning in 2014 partially because ethane is used to thin and ease transport of Canadian heavy oil. Demand is expected to increase by 700,000 bpd by 2017.

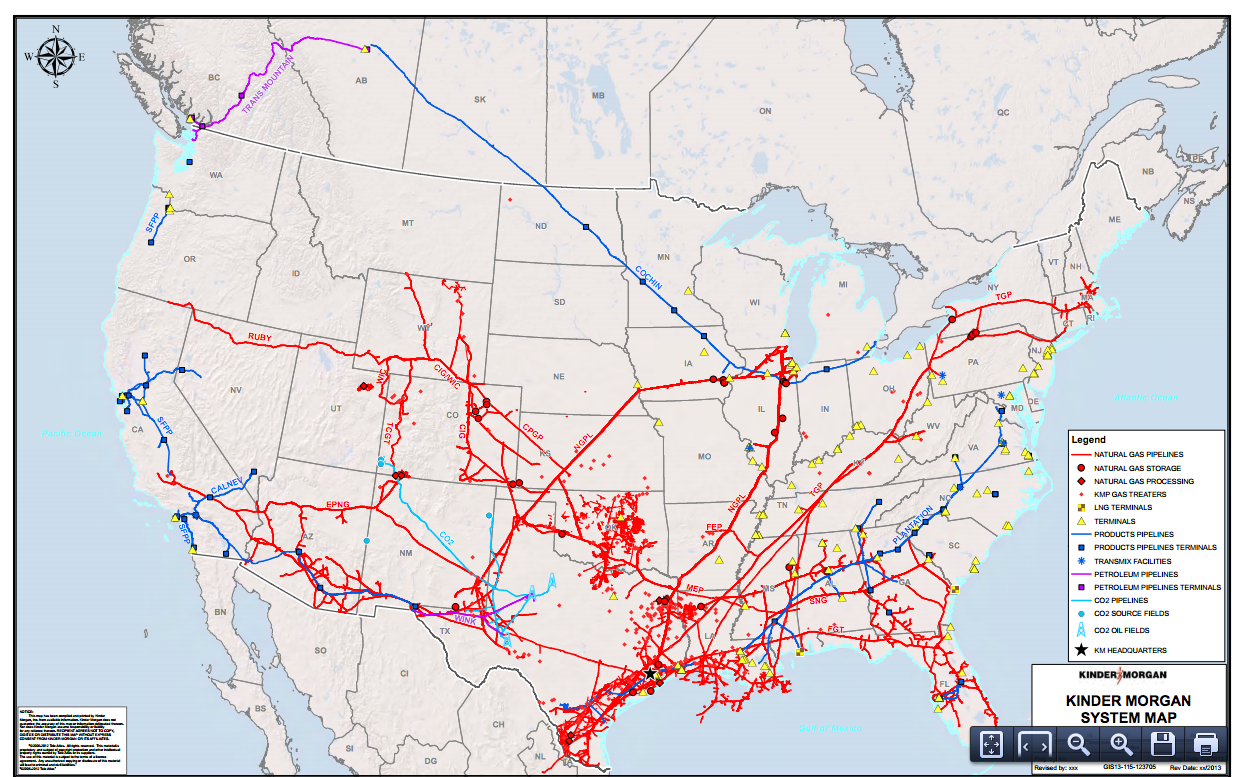

Kinder Morgan, (KMI 0.74%) is the general partner of Kinder Morgan Energy Partners and El Paso Energy Partners. It owns the largest network of natural gas pipelines in the U.S. Its 68,000 miles of pipe service every major shale area including the Eagle Ford, Marcellus, Utica, Uinta, Haynesville, Fayetteville, and Barnett shales.

Source: Kinder Morgan asset map

Recently, a series of negative press articles in Barrons and Bloomberg called into question Kinder Morgan's maintenance cost accounting and future growth prospects. The accounting concerns have been answered by the company; however, concerns remain regarding future dividend/distribution growth. Management is guiding for 5% distribution growth for Kinder Morgan Energy Partners and 8% dividend growth in the general partner over the next three years. Management has recently reaffirmed this guidance and noted $14.8 billion in expansion and joint venture projects designed to continue strong growth into the future. There are three catalysts that strengthen management's claim that strong growth can continue.

First, a recent study by ICF international predicts that $641 billion in additional investment will be required in America's energy infrastructure by 2035. This is approximately $30 billion per year or triple the annual rate of investment over the previous decade.

The second catalyst is the coming boom in LNG exports. Natural gas prices in Europe and Japan are twoto three times higher than in the U.S. and gas companies are eager to capture this difference. Already seven export terminals have been approved that will be capable of liquefying and exporting nine bcf/d of natural gas, approximately 12.5% of U.S. production.

Exports will begin in late 2014 and will result in increased U.S. natural gas prices. This, in turn, will cause gas production to increase and raise demand for Kinder Morgan's transportation and storage services.

The third catalyst is Kinder Morgan's Trans Mountain pipeline, which transports Alberta oil to Canada's west coast for export to energy-starved Asia. The company is in the process of completing a $5.4 billion expansion of the pipeline that will triple capacity from 300,000 bpd to 890,000 bpd. The project will be completed in 2017 and will likely accelerate dividend growth.

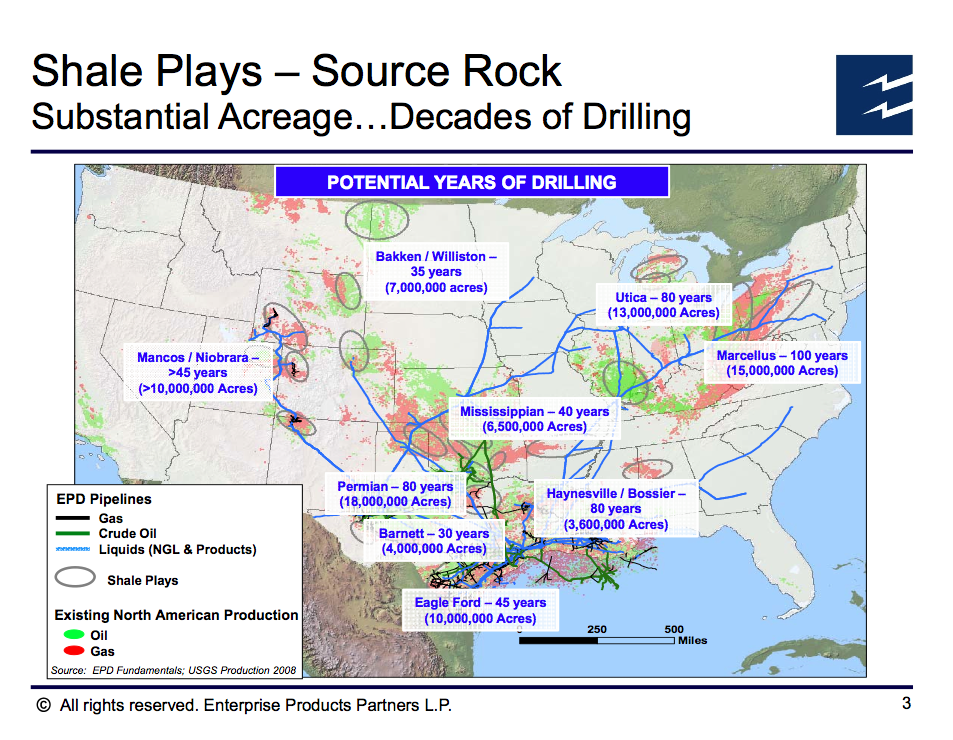

Enterprise Products Partners (EPD +0.53%) is the largest midstream MLP by market capitalization, and like Kinder Morgan, it services every major shale formation in America.

Source: Barclays Investment Grade Energy and Pipeline Conference.

As seen above, the projected life span of the current shale gas fields is between 35 and 100 years. This indicates decades of strong growth and profitability for both investors and the partnership. In the meantime, two medium-term catalysts exist for increasing distributions and capital appreciation.

The first is $5 billion of expansion projects that will be completed in 2014. This includes major projects such as the Seaway joint venture with Enbridge. When the project is complete in the first half of 2014, it will more than double capacity from 400,000 bpd to 850,000 bpd.

The second catalyst is that Enterprise Products Partners has no general partner. This means that 100% of new cash flow will go to increasing distributions for investors.

Bottom line

America's energy boom is just getting started and these partnerships all make excellent options for long-term investors who want to partake in the bounty.