Walgreen (WAG +0.00%) didn't impress Wall Street when it reported third-quarter earnings yesterday, despite announcing year-over-year increases in both profit and revenue. The stock fell more than 2% in mid-day trading on the news. Nevertheless, long-term investors should keep in mind that Walgreen's stock has gained nearly 55% over the past year. Let's dig deeper to uncover what Walgreen's third-quarter results tell us about the overall health of its business.

Beyond the numbers

In case you missed it, here is a brief recap of Walgreen's third-quarter results. The pharmacy chain generated a quarterly profit of $0.91 per diluted share. This marked a 7% increase from the same period a year ago, in which Walgreen posted adjusted earnings of $0.85 per share. Unfortunately, that was still more than 6% below analyst estimates for earnings-per-share of $0.94 in the period. Walgreen's third-quarter revenue, on the other hand, was in line with Wall Street's expectations at $19.4 billion.

Walgreen's stake in European drugstore chain Alliance Boots contributed $0.15 per diluted share to the company's adjusted earnings in the quarter. As a result, the company now expects second-year cost savings in the range of $400 million to $450 million from its strategic partnership with Alliance Boots, up from its prior guidance of $375 million to $425 million.

While this is encouraging in theory, how Walgreen plans to leverage its stake in Alliance Boots going forward is perhaps far more important. Walgreen's purchased a 45% stake in the European company two years ago and has an option to buy the remaining stake in 2015. Management said it would present investors with its game plan regarding this strategic tie-up as soon as July or early August.

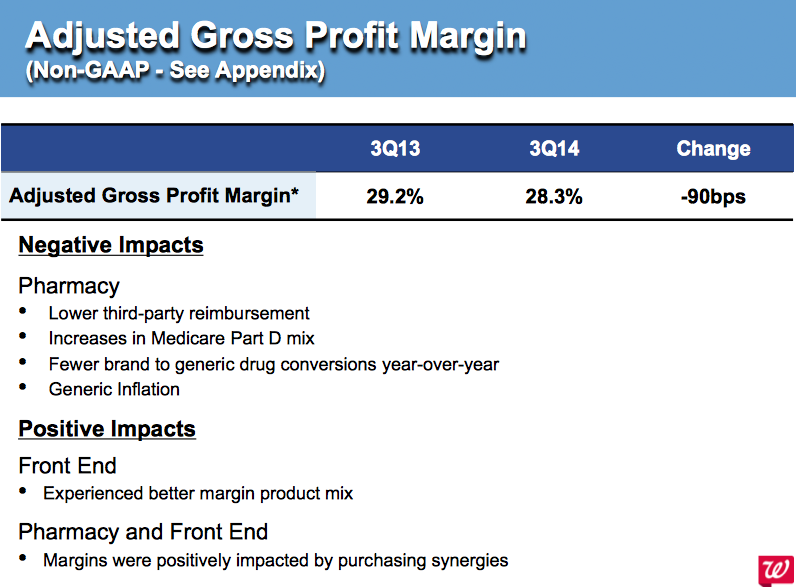

With more details of its partnership with Alliance Boots coming later in the year, let's shift our focus to what we do know from Walgreen's latest earnings release. For starters, increased pressure on gross profit margins in Walgreen's pharmacy business was of concern during the company's earnings call this week.

Source: Walgreen.

When margins matter

Higher generic drug costs and lower reimbursement rates squeezed Walgreen's margins in the quarter. Going forward, this means the pharmacy chain will need to better control costs to help offset some of the margin pressure. The company's chief executive Greg Wasson reassured investors by explaining, "We will be accelerating our optimization efforts, including taking additional steps to lower expenses companywide."

Walgreen's gross margin fell 40 basis points to 28 in the period. Yet, this is something that has also plagued rival pharmacy retailers recently, including Rite Aid (RAD +0.00%). Rite Aid reported quarterly results earlier this month that exposed a 55% decline in profit to $0.04 per share. Similar to Walgreen, Rite Aid blamed higher-than-expected drug costs and declining reimbursement rates for the free fall. With industrywide trends such as these, pharmacy retailers such as Walgreen will need to work especially hard to cut costs across its 8,217 stores nationwide.

Where to from here?

Lower reimbursement rates and pricing pressure from drug suppliers combined with vague details about Walgreen's plans for its expected buyout of Alliance Boots create significant uncertainty for the company today. Therefore, investors may prefer to stay on the sidelines for now, at least until management sheds more light on its plans for the European drugstore chain.