Shares of TE Connectivity (TEL +0.00%) have been soaring lately, rising more than 60% since the beginning of 2013. The supplier of electronic connectors has bounced back after the recession led to a steep drop in revenue and profits, and the company's most recent earnings showed impressive growth and profitability. I've previously laid out a few reasons TE Connectivity's stock could rise, as well as a few reasons it could decline, in the long term. But is TE Connectivity stock a buy?

Strong growth and high margins

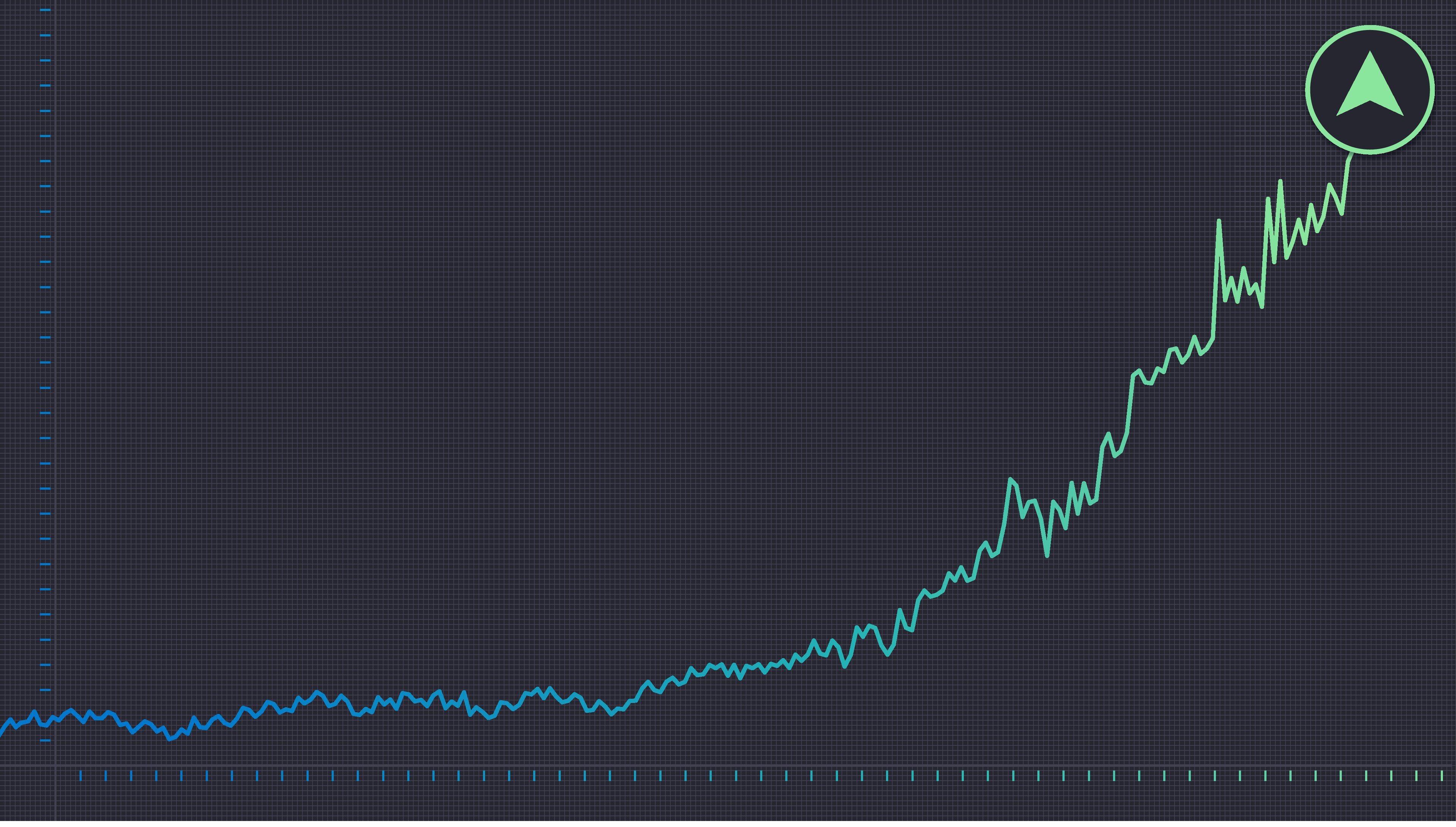

TE Connectivity is a cyclical company, depending heavily on the automotive industry as well as industrial activity. The company was hit hard during the recession, with revenue falling off a cliff:

TEL Revenue (Annual) data by YCharts

The company has recovered since then, and the core strategy has been to focus on so-called harsh-environment markets. These are markets where its connector products need to withstand extraordinary conditions, often involving a high level of engineering, and as of the most recent quarter a full 70% of TE Connectivity's revenue is derived from such markets.

The transportation segment accounted for 44.3% of total revenue during the most recent quarter, and the company managed a 21.1% adjusted operating margin for the segment. The industrial segment accounted for 23.7% of revenue, with a 15% adjusted operating margin. These margins are above the company average, and this focus on harsh environments has led the operating margin during the trailing-12-month period to reach a level not seen since 2005.

TE Connectivity expects EPS growth to be in the double digits going forward, with 5%-7% organic revenue growth along with an adjusted operating margin above 15% driving earnings higher. The recent acquisition of Measurement Specialties (MEAS +0.00%), a provider of sensors, greatly expands the total addressable market for TE Connectivity, allowing the company to vastly expand its sensor business to address the estimated $40 billion market.

Valuation

TE Connectivity appears to have a very strong business, but it does depend heavily on the strength of the global economy. Any slowdown in auto sales or industrial activity would be bad news for the company's bottom line, so valuing the company based on earnings in a great year could lead an investor to overpay for the stock.

In the trailing-12-month period, TE Connectivity earned $3.60 per share, putting the P/E ratio at about 16.7. This doesn't seem unreasonable for a company with such high margins and considerable growth prospects, but the story looks quite a bit different if instead we use the average annual earnings over the past decade, which include some very bad years. Even adding back in a $3.5 billion asset impairment charge from 2009, TE Connectivity averaged about $930 million in net income annually over the past decade, or about $2.23 per share using the current share count. Using this number, the P/E ratio climbs to 27.

At this point, after rising by so much over the past two years, TE Connectivity looks expensive. The company is having a great year, but I'm not convinced that operating margins in the mid-teens are sustainable in the long term. Consistent revenue growth is also questionable, given how choppy TE Connectivity's revenue has been historically. After the recession, revenue peaked in 2011 at $14.3 billion, followed by a decline of more than $1 billion the next year. Even in the TTM period, revenue is still nearly $500 million shy of that peak level.

Verdict: Wait for a lower price

TE Connectivity appears too expensive, and although guidance from management paints a rosy picture, historically the company has not been very consistent. TE Connectivity is a cyclical company, and based on its average 10-year earnings the stock is priced far too high. I would wait for a large correction before thinking about buying any shares of TE Connectivity.