Banks want to give you a loan. It's how they make money, after all. But since the financial crisis, many potential borrowers have found it exceptionally difficult to get their loans approved. Bankers were trigger shy as the economy sputtered along, unemployment remained elevated, and delinquencies mounted.

Now, though, times have changed. The jobs market is improving, the economy is finding its footing and, yes, banks are once again making loans. Here are two reasons why now is the best time to get a loan since the crisis began in 2008.

1. You're approved!

Total loans outstanding expanded by 6.6% in September on a year-over-year basis. That increase was primarily driven by a 12.3% increase in loans to businesses; but loans to consumers also grew by nearly 4%. This growth compares to a near 10% decline in total loans outstanding at the bottom of the recession, and it's the highest annualized growth rate since 2009.

Two factors are driving this growth, and both are great for consumers in need of a loan. First, banks were handcuffed immediately following the financial crisis as they dealt with existing problem loans, and rising capital requirements from new regulation. Today, both of those challenges are waning, and banks are again focusing on growth. Growth means they want to make more loans.

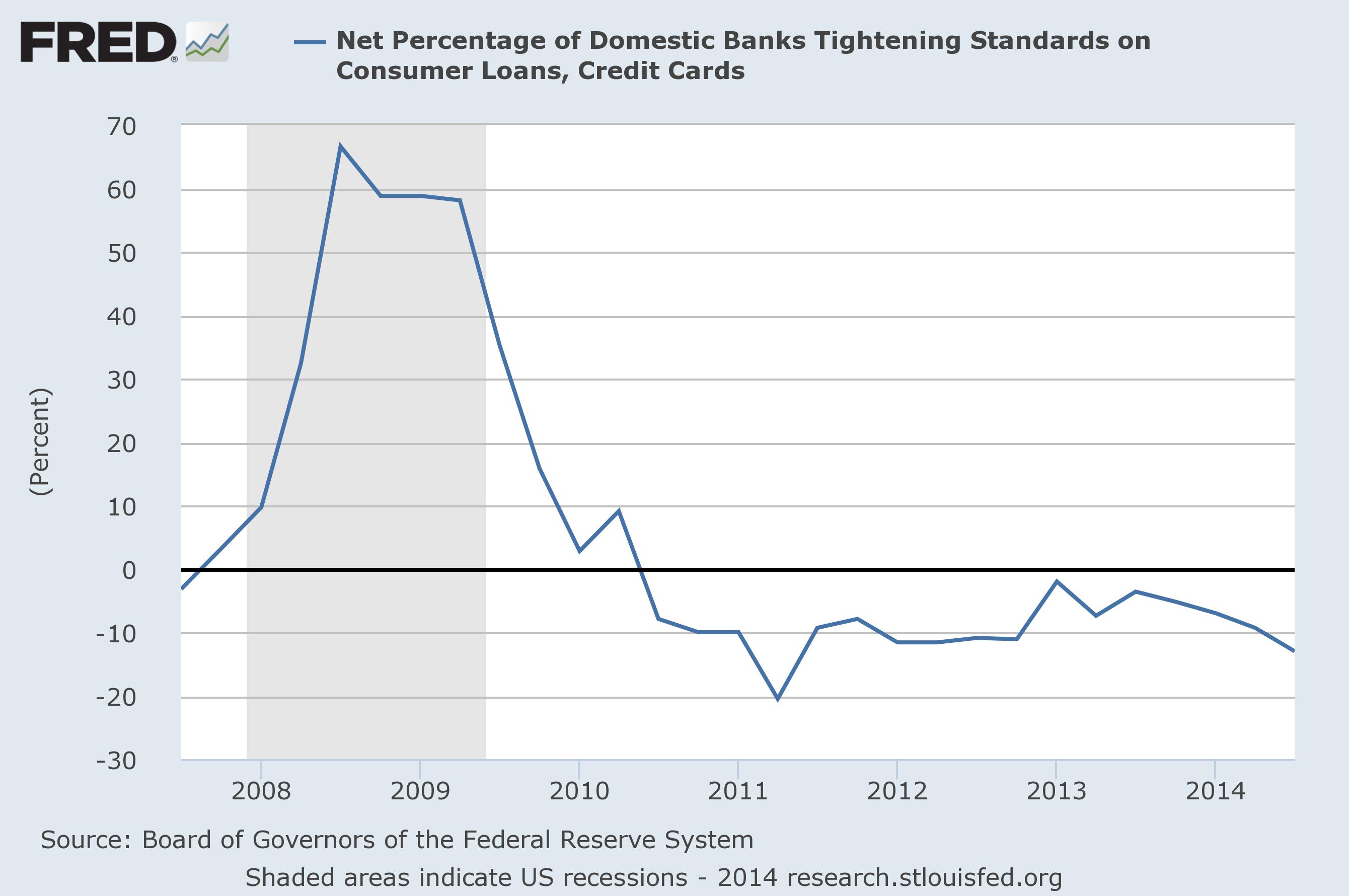

Second, as more and more banks compete for these loans, the consumer has an improved negotiating position. That means better terms and easier approvals. We can measure this by looking at the Federal Reserve's Survey of Senior Loan Officer Survey.

In the chart below, when the line is below zero, it indicates that banks are easing their lending standards.

Across the board, senior loan officers are reporting an easing of standards and terms for consumer and business loans. For the prospective borrower, increased willingness to lend, and increased competition from banks, make now an excellent time to get a loan.

2. Interest rates are still really low

Warren Buffet recently called taking out a mortgage today as a "no brainer" for the everyday investor. Why? Because interest rates today are exceptionally low, and will likely rise in the future.

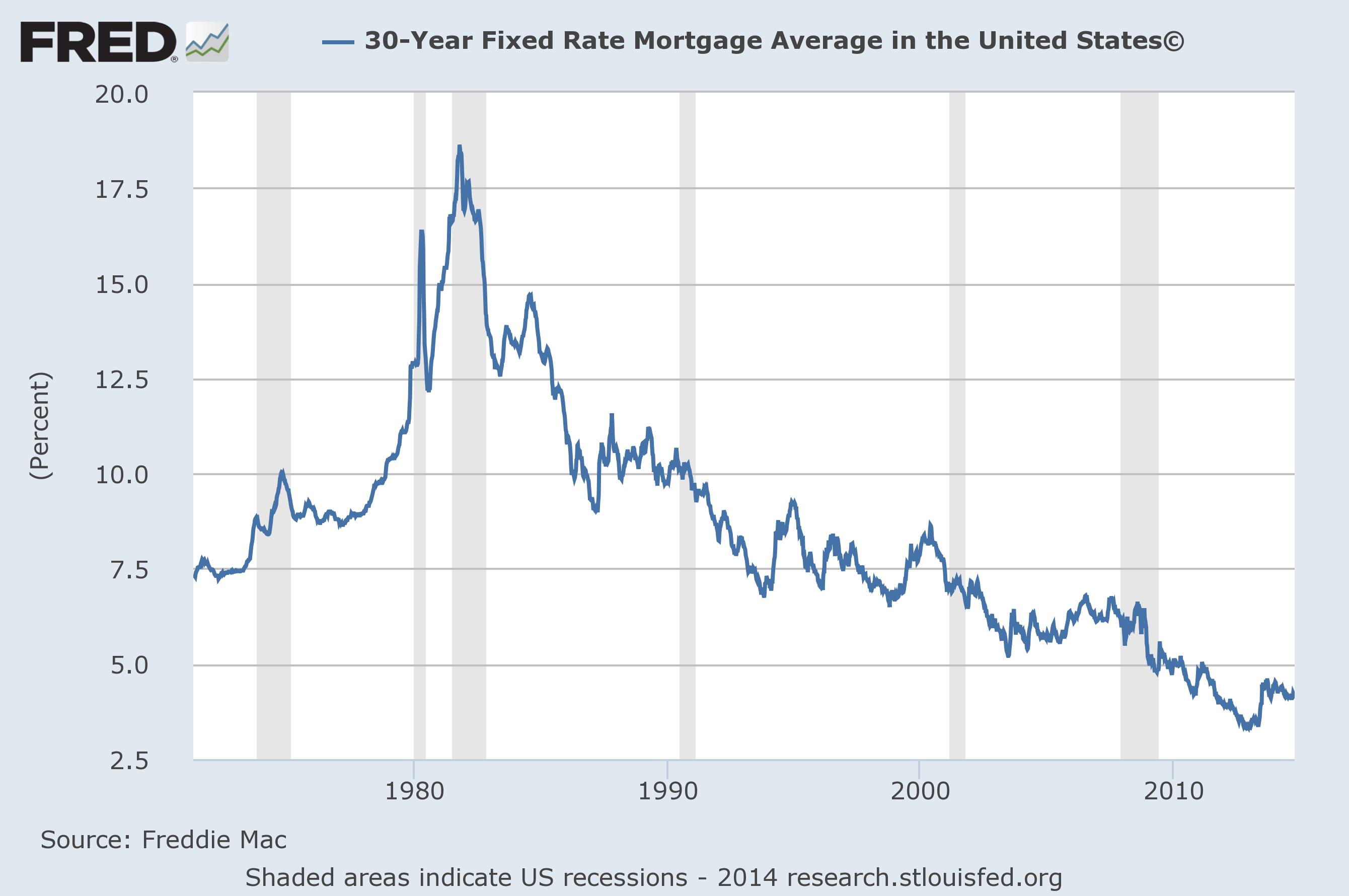

By borrowing today, you can obtain cheap money to hedge against those rising rates in the next few years. For some context, here's a chart that tracks the average 30-year, fixed-rate mortgage loan going all the way back to 1971.

Even as rates have increased slightly from the absolute bottom in April of 2013, today's 4.1% rate is clearly a remarkably low rate.

Most economists anticipate that the Federal Reserve will begin raising its target interest rate sometime in the next 12-18 months. That means there's a short, but very available, window of time right now to take advantage of these low interest rates. It's entirely feasible that these rates will be the lowest of an entire generation.

The case for applying for a loan today is strong. Of course, that doesn't mean running up a huge debt on your credit card. It means prudently structuring your personal finances to finance your home -- or other productive assets (perhaps an apartment building) -- while capital is so readily available, on favorable terms, and so, so cheap.