Image source: Caterpillar.

Caterpillar (CAT -0.07%) is a massive company, and its industrial might reaches across the globe. Caterpillar remains the world's largest construction and mining equipment manufacturer, but it only seems to be digging itself a deeper hole when it comes to global sales. That theme holds true for Caterpillar's recently released October machine retail statistics -- but there is a silver lining for patient investors.

The ugly numbers

It's no secret that Caterpillar's resource industries business segment has resembled a slow motion train wreck during the last couple of years. Weakness in mining markets overseas has all but evaporated demand for Caterpillar's heavy mining equipment, and that continues to weigh down the company's overall machine sales.

In October, for the three-month rolling period, Caterpillar's resource industry retail sales were down a whopping 38% in Asia/Pacific, 42% in Latin America, and down 20% overall across the globe. In fact, a grand total of zero Caterpillar regions posted positive sales growth in its resource industries segment for the three-month period ending in October.

Furthermore, Caterpillar combines sales statistics from its resource industries and construction industries segments, and that overall machine retail total was down 9%. However, there are a couple of silver linings for patient Caterpillar investors.

First, resource industries has been Caterpillar's biggest thorn in the side when it comes to revenues and profit struggles. While the previously mentioned 20% decline isn't good by any stretch of the imagination, it's less terrible than other results recorded this year.

Graph by author. Information source: Caterpillar.

Yes, it's not a great sign that one silver lining in Caterpillar's figures is a decline of 20%, despite it being the best year-over-year performance in 2014; but there is more to be positive about.

At the bottom?

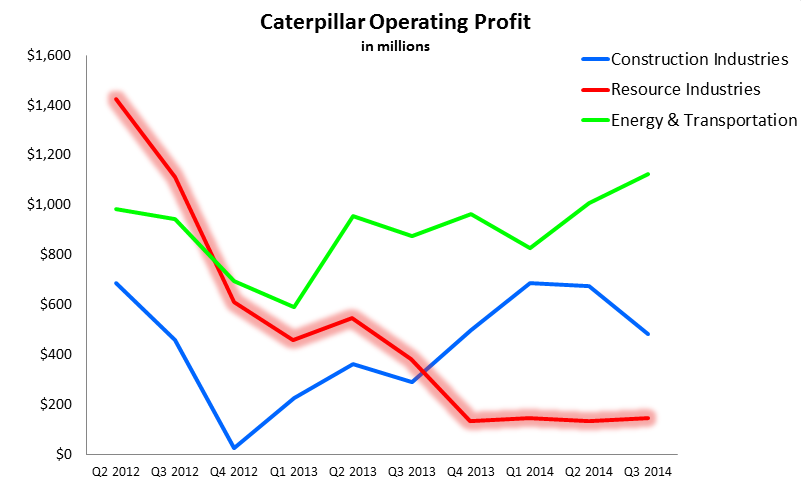

Though Caterpillar's resource industry segment operating profit has nosedived during the past two years, it appears to have finally bottomed.

Graph by author. Information source: Caterpillar.

It's difficult for investors who haven't kept up with Caterpillar during the years to imagine that its resource industries segment once generated a massive amount of the company's profits. It will certainly be a while before investors see profit levels reach its previous high; but if this is truly the bottom, and weakness in mining lightens a little bit and Caterpillar can slowly improve its resource industries profitability, it will be a huge plus to the company's overall financial performance and stock price.

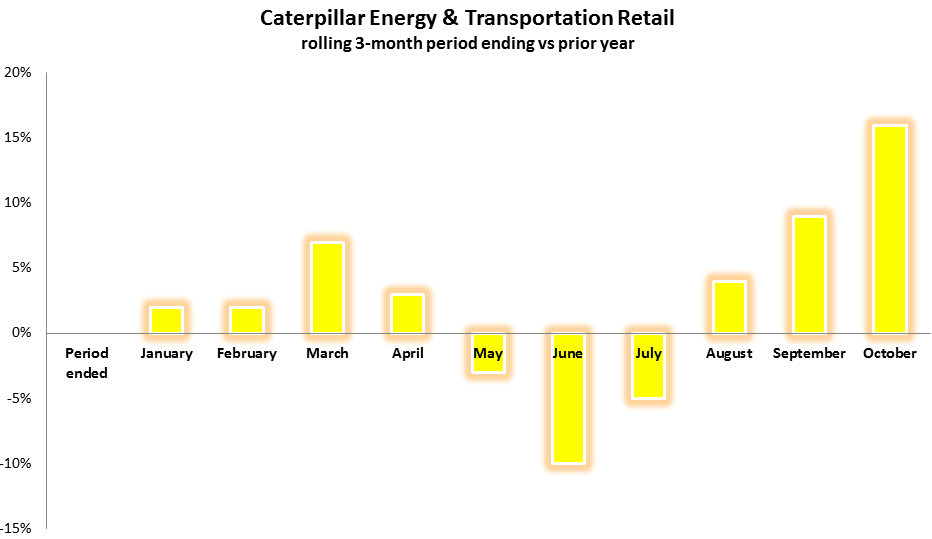

Energy and transportation surge

Another silver lining for Caterpillar is that its energy and transportation segment recorded its best year-over-year improvement of 2014 in October's three-month rolling figure. In fact, since the beginning of the summer, Caterpillar's energy and transportation retail statistics have been consistently surging higher.

Graph by author. Information source: Caterpillar.

Despite the sales and profitability surge of Caterpillar's energy and transport segment, as well as its troubled resource industries segment appearing to have bottomed in terms of profitability, there's very little to suggest the overall business will rebound significantly throughout 2015.

If you're an investor in Caterpillar, you'll need to possess a lot of patience going forward, and keep tabs on what the company can control: cost management and operational efficiencies. Investors will also want to keep an eye on the company's cash flow, which has been strong and stable enough, despite weak demand and slow growth.

The company continues to return value to shareholders -- through three quarters of 2014, Caterpillar has repurchased $4.2 billion of its stock, and raised the dividend 17%. If management stumbles on any of these factors, it could quickly erase the stock price's gain of roughly 28% during the last 12 months.