IBM's Thomas J. Watson Research Center. Source: IBM.

Shares of IBM (IBM +0.34%) fell on Tuesday night, following a fourth-quarter report marred by soft revenue. The stock is trading near its three-year low as investors worry about Big Blue's never-ending turnaround effort.

Analysts were looking for fourth-quarter earnings of $5.41 per share on roughly $24.8 billion in total sales. IBM delivered adjusted earnings of $5.81 per share, down 6% year over year. In the top line, revenue fell 2% to land at $24.1 billion.

The revenue figure was adjusted to remove currency exchange headwinds and the impact of the sale of some business operations during the year. If that sounds unfair, you'd want to call it a 12% year-over-year sales drop. But then you're forgetting about IBM's strategy change, which is driving most of this negative sales trend.

I prefer the adjusted revenue line because it offers a better take on how IBM's actual business is doing. But if you're using that adjusted metric, you'd better pay attention to what IBM is getting in exchange for its softer sales.

Big Blue isn't selling divisions willy-nilly. It is trimming the fat of stagnant growth or low profit margins, building a leaner, meaner cash machine around what IBM does best.

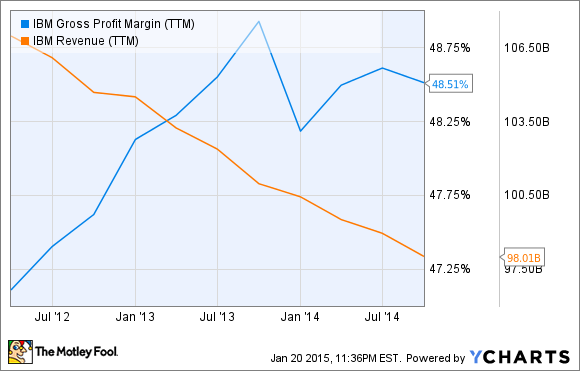

CEO Ginni Rometty took the reins from predecessor Sam Palmisano at the start of 2012. She quickly started reshaping the company, leaning away from the tired hardware operations and deeper into software and services. The effects on IBM's sales and margins have been drastic and obvious:

IBM Gross Profit Margin (TTM) data by YCharts.

Both of those trends continued in the fourth quarter. Alongside that 12% unadjusted revenue drop, gross margin rose from 52.4% to 53.3% year over year.

The net effect of these crossing lines is a remarkably steady bottom line. Pre-tax profit decreased just 2% from the fourth quarter of 2013, while profit margin rose from 27.7% to 30.7%. That's a healthy operating profit, but it was obscured by higher taxes and failed to drop all the way down to the earnings line. Here's how.

In 2013, IBM saw a large tax benefit in the fourth quarter. Three years of tax calculation assumptions were audited and found to overstate IBM's actual tax burden, so a one-time tax credit settled the score. IBM generally assumes that its income tax rate will sit somewhere around 23%. In the year-ago period, the effective rate plunged to 12.5% thanks to that audit-driven credit. Now we're back to normal again, as IBM's tax rate bounced back to 22.3%.

CEO Ginni Rometty is heading over yonder, whether Mr. Market likes it or not. Source: IBM.

So here's the situation. Rometty has refocused IBM on more profitable operations with better growth prospects in the next era of enterprise computing. I'm talking about the Internet of Things, about powerful software suites running on increasingly commoditized hardware, and about mobile computing on a grand scale.

Rometty classifies these products under the banner of "strategic imperatives." Revenue in these segments increased 16% year over year, and they account for 27% of IBM's total sales at the moment. And because the strategic imperatives contain a lot of high-margin software, these rapidly growing segments are raising IBM's overall profit margin as well.

"Our strategic direction is clear and compelling, and we have made a lot of progress," said CFO Martin Schroeter in prepared remarks. This year will be bumpy as the strategic imperatives scale up. After that, all bets are off: "We see the ability to generate low-single digit revenue growth, and with a higher value mix, high-single digit operating earnings-per-share growth, with free cash flow realization in the 90% range."

So it's a new world out there. IBM is adjusting to it very effectively, accepting some short-term pain to build a stronger fundamental business. The stock is selling at a huge discount -- just 9.3 times trailing earnings -- because of that temporary softness.

This is a spring-loaded stock right now. I'm tempted to open an IBM position myself, before the true value of Rometty's new strategy starts paying off on the bottom line.

But there's no rush to pull the trigger, because the rocket isn't quite ready to fly yet. It looks like I'll get several more quarters of rocky results before I'd miss the final countdown.