Quick-turn manufacturer Proto Labs (PRLB -4.71%) is set to report its fourth-quarter 2014 earnings on Feb. 5 before the market opens. Going into the report, Wall Street expects Proto Labs' revenues will grow by 23.9% year over year to $54.6 million, translating to $0.42 in earnings per share. Beyond the headline expectations, investors should also key in on how Proto Labs' underlying business is faring by examining company-specific metrics that help determine whether the long-term investment thesis remains intact. Here are three key metrics to familiarize yourself with before Proto Labs' upcoming earnings.

Product developers served

Central to Proto Labs' growth story is the number of product developers it serves during a given quarter. Ultimately, a growing base of product developers translates to more revenue-generating opportunities for Proto Labs and indicates that the company's visibility and influence in the rapid-manufacturing world is growing. Historically, Proto Labs has done an excellent job growing the number of product developers it serves across its Protomold injection molding and Firstcut CNC machining services, which represented nearly 94% of its revenue last quarter. Any divergence from this trend without a reasonable explanation could be potentially worrisome.

Source: SEC filings.

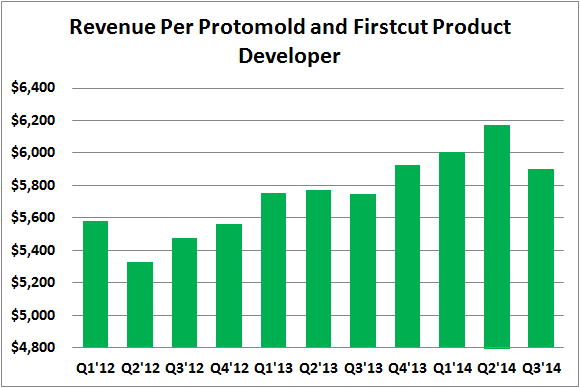

Revenue per product developer

The amount of revenue that Proto Labs generates per product developer could also prove to be helpful in determining how the company's underlying business is faring. After all, Proto Labs' ability to drive increased sales per existing product developer suggests that customer loyalty is on the rise, and its manufacturing services may command a level of pricing power in the marketplace. At the end of the day, if Proto Labs can continue building a growing base of satisfied customers who keep coming back for more, it should bode well for the business longer-term. During the third quarter, Proto Labs' revenue per product developer declined on a sequential basis, but the company still managed to drive a 2.6% increase in customer spending year over year.

Source: SEC filings and author's calculation.

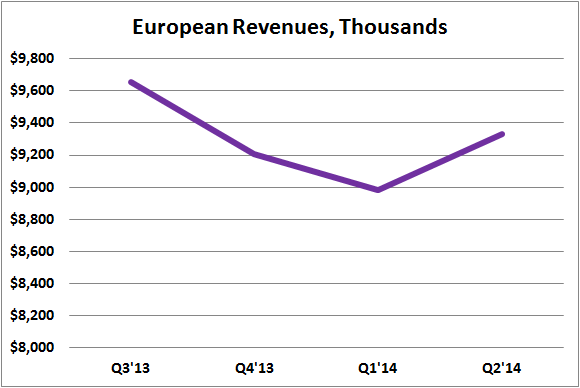

European revenues

One potential problem area for Proto Labs' fourth quarter earnings may stem from the revenue it generates abroad, particularly in Europe, where economic activity has been sluggish compared to its North American and Asian counterparts. Over the past year, Proto Labs' European revenue growth has stalled relative to the company's overall revenue trajectory, and management recently acknowledged a "notable" slowdown in the Eurozone area. During the third quarter, Proto Labs' European operations represented 17.1% of the company's total revenue, meaning it's simply too big of an area for investors to ignore.

Source: SEC filings and author's calculation.

Bottom line

When Proto Labs reports its fourth-quarter earnings on Thursday, Foolish investors should focus on how the underlying business has been performing, rather than how investors react to the news. Monitoring the number of product developers Proto Labs serves, the revenue it generates from each product developer, and how its European business is faring are all great ways to start determining if Proto Labs' business remains on track for potential long-term success.