The tech sector can be fertile ground for profitable investments -- if you know where to look. With that in mind, we asked four Motley Fool contributors covering technology companies to name their top tech stock to buy right now. Their answers: Google (NASDAQ: GOOG) (GOOGL +1.55%), Cisco (CSCO +4.44%), IBM (IBM +2.92%), and Micron Technology (MU +7.70%). Read on to see why.

Source: Google.

Joe Tenebruso (Google): Google's move to reorganize itself under its new Alphabet structure is brilliant, as it helps to send a clear message of what the company has become: a collection of businesses with investments in a far-ranging array of exciting technologies that are poised to pay increasing dividends to shareholders in the years ahead.

The new holding company structure will allow disparate businesses -- such as Google Fiber, Internet of Things device maker Nest, and the longevity-focused Calico -- to be run and scaled independently. Management believes this will give these exciting opportunities their best chance at receiving the resources and attention they need to succeed over the long term.

Google will remain the largest of these initiatives, and will operate as a fully owned subsidiary of Alphabet. In fact, the biggest near-term benefit for shareholders may be that this new structure will place Google's true earnings power on full display, unencumbered by the heavy investments that Alphabet is making on long-term projects that have yet to produce any meaningful revenue. I believe investors will be surprised at just how profitable Google truly is when the company implements segment reporting in its fourth-quarter results, making now a great time to consider buying shares.

Source: Flickr/Prayitno.

Tim Green (Cisco): Cisco, the dominant player in the networking hardware market, benefited tremendously from the growth of the Internet over the past few decades. Cisco is now entering a new era, where its growth will be driven by what former CEO John Chambers once called the second generation of the Internet.

The Internet of Things is mostly a buzzword today, but however it ultimately plays out, the amount of data being transmitted over the Internet is set to increase dramatically in the coming years. As networking becomes more complex, driven by this deluge of data as well as cloud computing, Cisco is set to benefit once again. The company is positioning itself as a seller of networking solutions, not just hardware, and its current dominance gives Cisco an enormous advantage.

While The Internet of Things will play out over many years, the recent market turmoil has knocked Cisco's stock down to bargain levels. Adjusted for the excess cash sitting on its balance sheet, Cisco trades at about 11 times 2015 GAAP earnings, a valuation that seems awfully low for a company with significant competitive advantages and long-term growth potential.

Tim Brugger (IBM): At first glance, it's easy to see why IBM's stock price is down about 8% year to date, as of this writing. After all, its second-quarter earnings release announced on July 20 wasn't exactly anything to write home about -- at least not at first glance.

But IBM's top line only tells part of the story. The hit IBM took last quarter nearly across the board would look much different if not for currency headwinds and a charge to divest itself of its former System X unit. But for investors in search of value -- let alone a dividend yield near 3.5% -- it's the growth of IBM CEO Ginni Rometty's "strategic imperatives" that really matter.

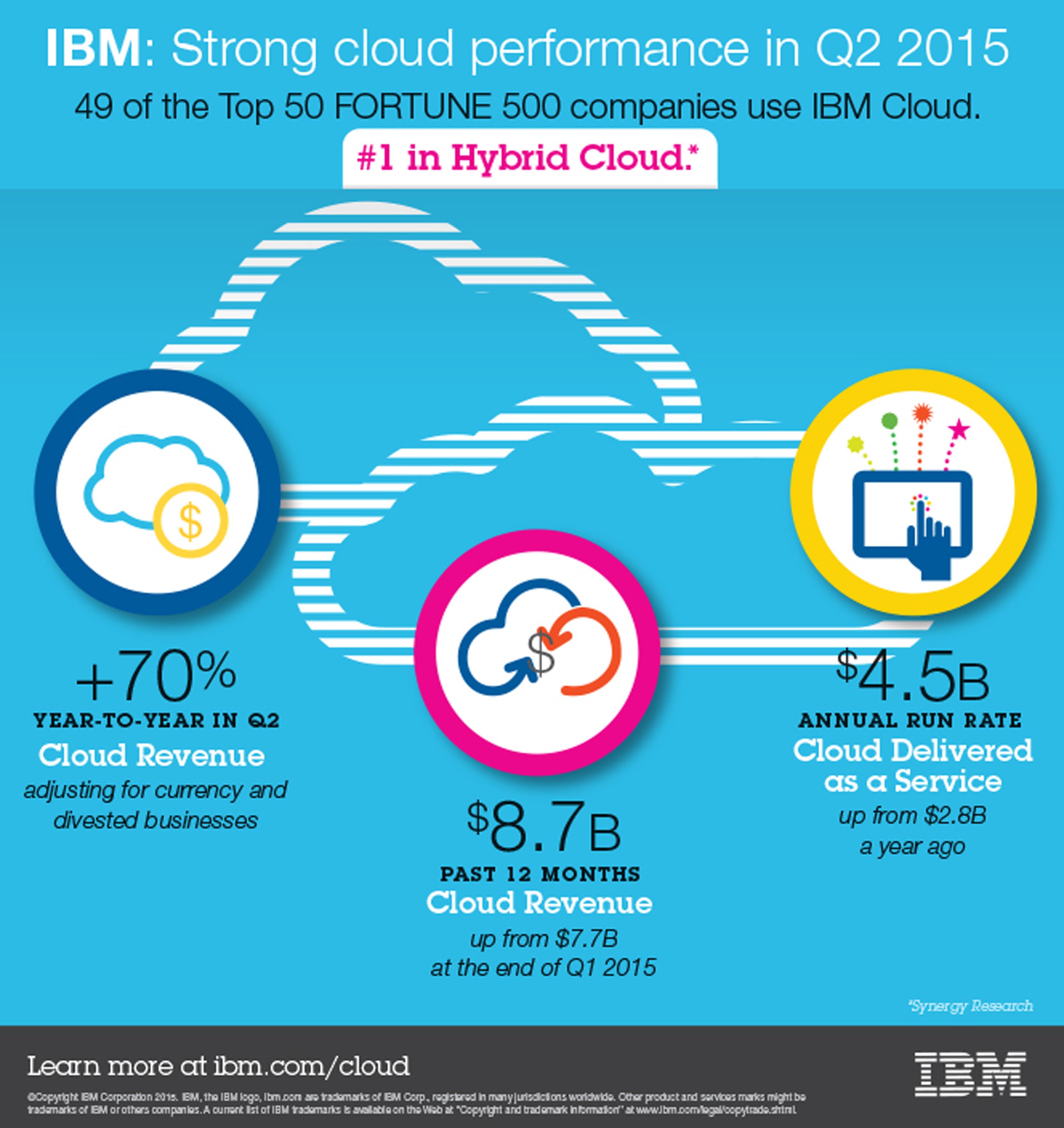

Like others in the tech industry, IBM is in the midst of transitioning to new markets, including the cloud, big data, and analytics. And in these key areas, IBM has consistently delivered. The second quarter was no exception. On the cloud front, revenues were up over 70% last quarter accounting for currency and one-time items, and IBM now boasts an annual run rate of $4.5 billion. Though late to the game, IBM is already one of the leaders in the fast-growing cloud market.

Source: IBM.

Business analytics, particularly those related to big data -- the assimilation and analysis of today's unprecedented reams of information -- also jumped last quarter, by more than 20% excluding the impact of currency rates. For long-term investors, the results of IBM's strategic imperative results is where its bread is buttered, and that's why it's a top tech stock in September.

Anders Bylund (Micron Technology): Memory chip manufacturer Micron Technology has fallen on hard times in 2015. The stock fell 20% in August alone and more than 50% year to date.

Micron has indeed slowed down from the fantastic revenue and earnings growth it delivered in 2013 and 2014, mostly due to falling sales in the PC systems market. If you expected uninterrupted growth, following Micron's game-changing buyout of Elpida, you're surely disappointed these days.

MU Revenue (TTM) data by YCharts.

But then, I'd say you're investing in the wrong sector to begin with.

The memory market has always been extremely cyclical, even by the standards of computer component builders. Memory technologies are very well understood and relatively easy to implement in high-volume production runs. This occasionally leads to massive oversupply and vicious price wars, followed by a period of prosperity and consolidation.

The industry is down to only three serious players these days. Further consolidation is unlikely, but so is another round of brutal price wars. The remaining players are both large and equal enough to treat this market with more restraint. The growth-hungry upstarts are all gone; the adults are running this show today.

Micron has new technologies up its sleeve, and if the PC market actually goes pining for the fjords someday soon, there's still plenty of demand from markets like mobile devices, the Internet of Things, and automotive computing.

Micron shares trade at bargain-basement levels today, fetching just 5.4 times trailing earnings. The stock is priced for absolute disaster, but the business is only taking a brief breather. Invest accordingly.