Usually when you see a stock or MLP yielding 9.6%, as Energy Transfer Partners (ETP +0.00%) currently is, this is a sign that Wall Street doesn't have confidence in the security or growth potential of the payout. However, in this case Energy Transfer's yield isn't a valid or accurate representation of the MLP's underlying business model, assets, and cash flow-generating abilities. Rather, it's an overreaction resulting from the combination of the oil crash and recent market correction.

Let's explore three reasons the market is dead wrong about Energy Transfer Partners and, more importantly, how you can profit from Wall Street's short-sighted fear, uncertainty, and doubt.

Energy Transfer's yield shouldn't be this high ...

ETP Dividend Yield (TTM) data by YCharts

Energy Transfer's yield is at the highest it's been in the six years since the dark days of the financial crisis, when economic and financial conditions were far bleaker than they are today.

In fact, in its latest quarter, Energy Transfer reported that three- and six-month distributable cash flow, or DCF -- from which the quarterly payout is funded -- was up 20% and 10%, respectively, over the same period last year.

True, the three- and six-month distribution coverage ratios, or DCRs, decreased 33% and 38%, respectively, yet this doesn't necessarily mean Energy Transfer's distribution is at risk, as Wall Street is insinuating with its current valuation. Rather, there are good reasons for the decreased DCR; reasons that should help Energy Transfer secure strong, sustainable payout growth for years to come.

... because the distribution isn't in danger though future payout growth might be slower

Energy Transfer's three- and six-month DCRs were both a sustainable 1.03, in line with management's long-term target of approximately 1.05. The reason for their sharp decline from 2014's levels -- despite such a large increase in DCF -- was because of a 36% increase in unit count compared to Q2 of 2014.

While that amount of potential investor dilution may at first appear alarming -- and this investor dilution could slow per unit distribution growth in the future -- it's actually due to two major deals Energy Transfer made over the past year: its $1.8 billion acquisition of Susser Holdings and its $18 billion merger with Regency Energy Partners, which created 15.8 million and 172.2 million new units, respectively.

Thanks in part to these two deals today, Energy Transfer Partners is one of America's largest energy transportation operators, with 62,500 miles of natural gas, natural gas liquid, and oil pipelines; over 65 processing, treatment, and fractionation plants; 59 million barrels of liquid storage capacity; and over 5,600 gas stations in the Eastern U.S. and Texas.

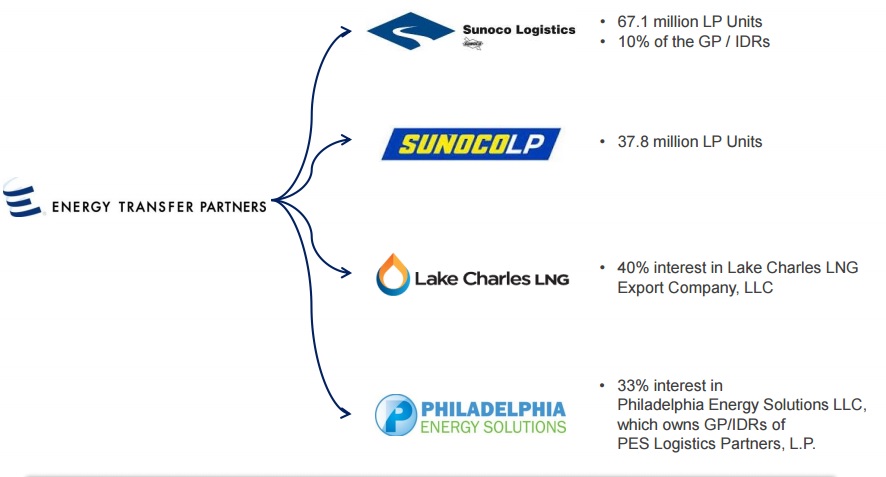

Better yet, Energy Transfer Partners' empire includes various equity stakes in several general partners and MLPs, as well as 40% ownership in a $9.6 billion LNG export project. Together, Energy Transfer Partners' assets and subsidiaries combine to create a vast and growing river of predictable, fee-based, commodity-insensitive, and recurring cash flow with which to secure and grow its generous distribution.

Source: Energy Transfer Partners investor presentation.

The MLP isn't in financial distress

Energy Transfer Partners has an investment-grade credit rating and debt-to-EBITDA ratio of 4.59, which management wants to lower to a long-term target of 4.5.Because of its good credit and vast scale, Energy Transfer Partners has access to a vast amount of untapped low-cost credit. In fact, it has $6.5 billion remaining on $7.8 billion of total credit revolvers for it and its subsidiaries to fund its growth efforts.

As additional projects come online -- Energy Transfer has invested over $4 billion in growth projects in just the last six months alone with another $1.6 billion slated for the second half of 2015 -- the additional EBITDA they generate should lower the MLP's credit ratio and allow it to tap its vast credit sources to fund its massive growth plans.

Further growth capex funding will come from drop downs Energy Transfer Partners plans to do with its subsidiaries such as Sunoco LP (SUN +0.17%) in 2016.

Future payout growth prospects are good

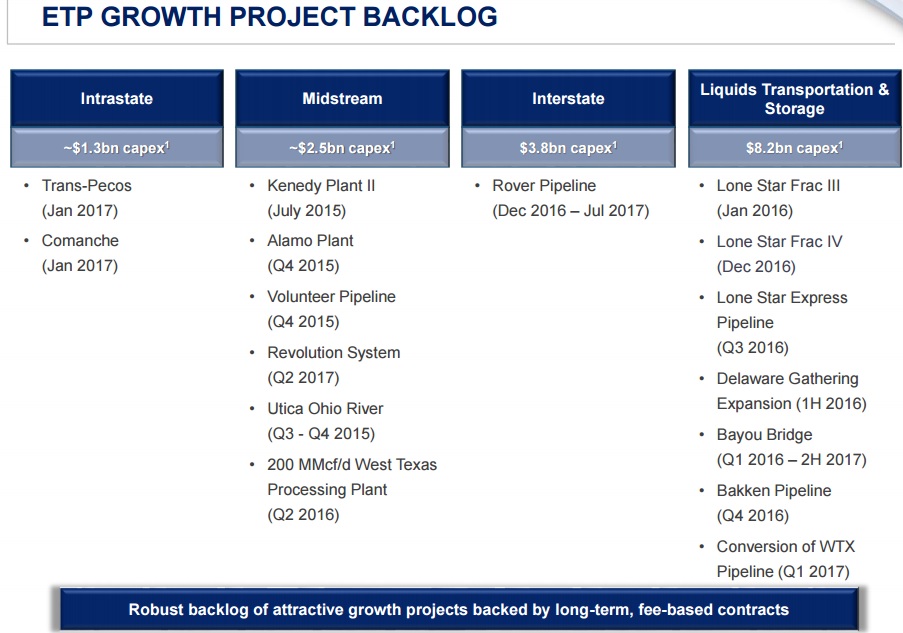

Source: Energy Transfer Partners investor presentation.

In the next 2.5 years, Energy Transfer and its joint venture partners will complete almost $16 billion in growth projects, of which Energy Transfer's net investment will be over $10 billion.

Over the past year, the MLP brought online $1.9 billion in new projects. Through the end of 2017 it plans to more than double that rate of project completion which -- when combined with the DCF accretive effects of the Regency Energy merger which don't kick in until after 2015 -- should easily help Energy Transfer Partners achieve moderate and sustainable distribution growth.

Takeaway: Energy Transfer Partners is being valued as a cigar butt when it's actually a solid long-term investment

Super high-yielding securities usually indicate an underlying problem with a company's business model that threatens the security of the payout as wells as its long-term growth prospects. However, Energy Transfer Partners looks like one of America's largest and most diversified midstream operators, with enormous access to liquidity and a promising and massive growth backlog that should result in sustainabl distribution growth over the next several years.

When combined with the MLP's current sky-high-yield, Energy Transfer makes for a very appealing value-based income growth proposition, and long-term income investors should consider adding to it to their diversified dividend portfolios at today's ridiculously undervalued price before Wall Street realizes its mistake.