Alcoa Inc (AA +0.00%) is planning to break into two companies. That's pretty much the culmination of a corporate makeover directed by CEO Klaus Kleinfeld. But there are some notable questions to ask, like who's going to be left paying for the transformative acquisitions?

Before the beginning

Before Kleinfeld joined Alcoa in 2007, the company had roughly $16 billion in debt. Today, the company's debt stands closer to $25 billion. That's a $9 billion jump, or an increase of more than 50% in less then a decade. That sounds pretty significant, and it is, but it isn't a full picture.

Alcoa's CEO Klaus Kleinfeld. Image source: Alcoa.

Looking at that another way, in 2006, Alcoa's debt made up around 30% of its capital structure. At the end of the third quarter, that was up to around 40%. So, it's not as big a jump as it might at first appear. But Alcoa operates in a cyclical industry, so less debt is better -- a fact that comes into keen focus when you're in the throes of a downturn.

As an example of what too much debt can do, look at Freeport-McMoRan Inc (FCX +6.98%). In mid-2013, the copper miner entered the oil and gas market in a big way, spending $20 billion to buy McMoRan Exploration Co. and Plains Exploration. That pushed the company's debt from around $3.5 billion to about $20 billion in a year. Debt remains at around that level today, roughly two years later. The jump was bigger at Freeport, though, with debt going from 15% of the capital structure to, at this point, around 50%. And now that oil has joined the commodity downturn, Freeport is having trouble making ends meet.

Getting better

The more notable difference between Freeport and Alcoa, though, is probably what the debt paid for. In Freeport's case, it was a commodity business that's now struggling. In Alcoa's case, the debt supported a shift from commodity products to more specialized fare that is less cyclical, has higher profit margins, and more growth potential. Acquisitions played a big role in that, but not the only role, and that leads right to the break-up.

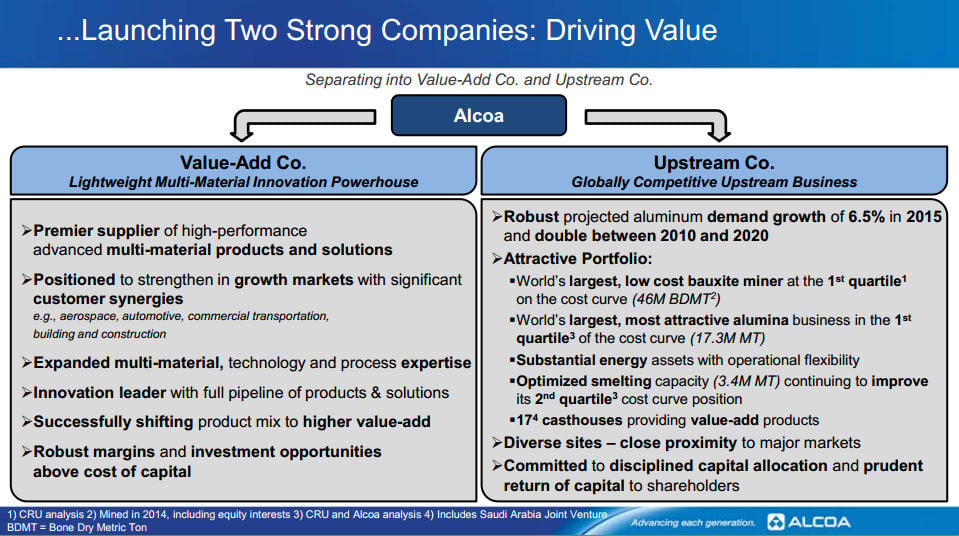

Alcoa is going to split into what is essentially a commodity aluminum company and a specialty aluminum company that makes high-end parts for end-markets like automobiles and airplanes. The idea is to free up the "Value-Add Company," as Alcoa is calling it, from the weight of the commodity business, which is suffering from global overcapacity and low prices.

The break up. image source: Alcoa.

That sounds like a solid idea. But here's the question: Who gets the debt that was used to build up the Value-Add Company? At this point, Alcoa says it is targeting an investment-grade credit rating for the Value-Add Company and a "strong" non-investment grade rating for the assets that get left behind in old Alcoa.

But here's the wrinkle: According to the company, the current debt of Alcoa "would be retained by the Value-Add Company." Wouldn't that leave old Alcoa with a pristine, debt-free balance sheet? Sure, it would have to deal with pension liabilities and the like, but it's hard to believe that would push it below investment grade if the spin-off takes all of the debt. Something seems amiss, here. Is old Alcoa going to start life debt-free only to pile on the debt once it's a stand-alone company?

Watch this issue

The spinoff of the Value-Add Company isn't going to happen until around the second half of 2016, so there's still a lot up in the air. And while Alcoa's debt isn't overbearing, it is still notable for a commodity business. In the end, where that debt ends up could make a big difference to the long-term success of both the Value-Add Company and what gets left behind.

Don't get caught up in the excitement of the spinoff; debt--more specfically, how that debt is split up-- is one issue you'll want to pay close attention to as Alcoa moves closer to its break-up.