The big headlines out of Alcoa Inc (AA +0.00%) are all about the company's pending breakup. And for good reason. But, as an investor, you have to look past the headlines and ask if this change is for the better -- or worse.

What's going on?

Over the last few years, Alcoa CEO Klaus Kleinfeld has been shifting the aluminum giant toward specialty products and away from commodity products. That's been a good decision overall, because specialized products, like jet engine parts, generally have higher margins and growth prospects. For example, the company expects the aerospace market to grow at around a 9% annual rate over the next few years. Older, commodity-like businesses such as producing soda cans, meanwhile, are only expected to expand in the low single digits.

Alcoa CEO Klaus Kleinfeld. Image source: Alcoa.

But this transformational split is about more than that. Essentially, Alcoa is breaking up into an aluminum company and an aluminum products company. One will create the base material, a commodity, that the other uses to make unique products. That's all in-house today, in what's known as vertical integration.

To give you a sense of the internal shift that led to this, roughly 80% of the company's growth spending this year has gone toward specialized products. Meanwhile, Alcoa continues to idle or close base metal facilities around the world. That's been the basic trend for several years and this big split is pretty much the culmination of years of effort.

So Alcoa is, in one move, shifting away from the vertically integrated model. The specialty parts business, what Alcoa is calling the "Value-Add Business," will have to buy aluminum from another company and the old Alcoa, dubbed the "Upstream Business," will have to find new customers to buy its aluminum. Clearly, the two will have a relationship after the break up, but that's the big-picture takeaway on this split.

Looks good to me!

Right now this looks like a great move, at least for the value-add business. That's because aluminum prices, like so many other commodities, have been floundering under the weight of global overcapacity. And, yes, it's China that's a big part of the problem. This means that the upstream business has been facing weak markets while the value-add business has increasingly been able to charge more for its products.

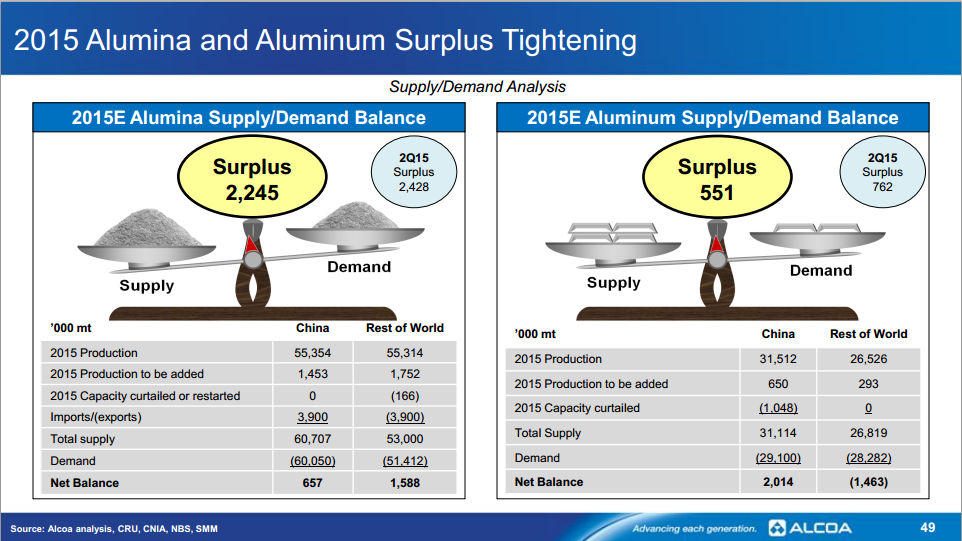

Aluminum supply/demand picture. Image source: Alcoa.

And it just gets better for the value-add business after the split because it can start to shop around for the cheapest aluminum instead of having to rely on an in-house supply, regardless of the cost. But the upstream business will be left selling a commodity product competing largely on price. If you extrapolate today's market into the future, it sounds like the value-add business is getting the better deal here.

But aluminum is a commodity. What happens if -- perhaps when -- prices kick back up? The currently struggling upstream business will be in for a windfall. The value-add business, however, will be dealing with cost headwinds that are largely out of its control. That suddenly becomes a much bigger risk without the upstream business in the fold.

But is it good?

Controlling supply is why companies vertically integrate in the first place. For example, Nucor (NUE +7.17%) is one of the largest recyclers in the United States, recycling 19 million tons of scrap steel in 2014. Scrap is a key input for the steel giant. It's also been investing in plants to make direct reduced iron in house, which is an alternative to scrap, despite low commodity prices. Nucor is, essentially, working toward greater control of its key input costs even though those costs are low today.

Alcoa is going the opposite direction. That could turn out to be a great call for the value-add business over the near term, but it poses a big question mark over the long term. It's worth noting that Nucor's conservative business model has allowed it to increase its dividend for 40 years. Alcoa's dividend, meanwhile, was gutted in the recession, going from an annual $0.68 a share to just $0.12, and it hasn't budged since.

Alcoa and Nucor are different companies in different industries, of course, but they both deal with commodities and specialty products. Although Alcoa may be making the right choice for its specialty products business today, it might end up regretting the loss of control down the line. As an investor, you'll want to keep this soon-to-be-increased risk in the back of your mind when deciding whether or not to keep a broken up Alcoa in your portfolio. If you decide you like the integrated model better, you might want to consider a switch.