The worst oil crash in 50 years has made Wall Street hate pretty much every oil and gas-related stock. That includes even such high-quality midstream MLPs as Holly Energy Partners (HEP +0.00%), which has beaten larger competitors such as Energy Transfer Partners (ETP +0.00%) and the market in general over much of the past decade.

HEP Total Return Price data by YCharts

In fact, Holly Energy Partners is down 30% since its June 2015 highs, creating a potentially spectacular long-term income opportunity that dividend lovers won't want to miss.

Distressed yield ignores rock solid business model

| Company | Forward Yield | 5-Year Average Yield | Price/Operating Cash Flow | 10-Year Average Price/Operating Cash Flow |

|---|---|---|---|---|

| Holly Energy Partners | 8.8% | 5.9% | 6.6 | 12.2 |

| Energy Transfer Partners | 16% | 7.4% | 3.5 | 8.9 |

Both companies are trading substantially below their historic yields and price-to-operating cash flows. However, with yields this high, the market is signaling that it thinks both of their payouts are at risk from crashing commodity prices. In reality, the differences between the payout sustainability at Holly Energy Partners and Energy Transfer Partners couldn't be more stark.

No distribution cut worries here

| Company | Q1-Q3 2015 distribution coverage ratio | Q1-Q3 2015 Excess DCF (Annualized) | 5-Year Projected CAGR Payout Growth |

|---|---|---|---|

| Holly Energy Partners | 1.15 | $24.3 million | 8% |

| Energy Transfer Partners | 0.97 | ($115 million) | 4.3% |

Sources: earnings releases, 10-Qs, Fastgraphs, management guidance.

Both Holly Energy Partners and Energy Transfer Partners' cash flows are predicated on long-term fixed-fee contracts. The main reason Holly Energy Partners' distribution coverage ratio -- the best metric for determining long-term payout sustainability -- is so much better than Energy Transfer Partners' is that almost all of its contracts have minimum volume or revenue commitments that guarantee the security of its distributable cash flow, no matter what energy prices do.

This means that Holly Energy Partners' cash flow is more consistent than Energy Transfer Partners' and because Holly's management is careful to grow the distribution less than the cash flow it's able to maintain a far more sustainable coverage ratio.

In contrast Energy Transfer management is less conservative and attempting to please investors with consistent quarterly distribution growth even if current market conditions and its contract mix make it inappropriate.

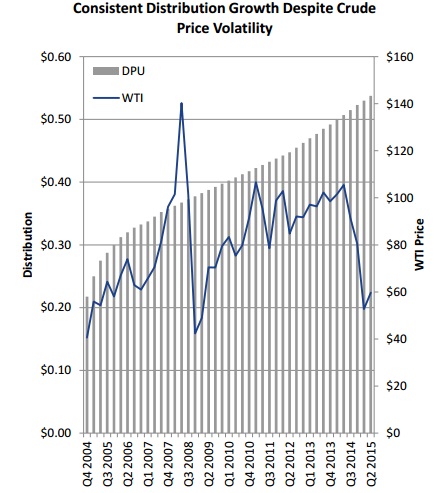

Source: Holly Energy Partners investor presentation.

This situation has allowed Holly Energy Partners to achieve 45 consecutive quarterly distribution increases without large fears of a cut.

What allows Holly Energy Partners to gain such attractive contract terms? The answer lies in its sponsor, manager, and general partner, HollyFrontier Corp. (HFC +0.00%).

Because HollyFrontier Corp. owns a 39% stake in its MLP, as well as the lucrative incentive distribution rights, it has a strong incentive to drop down midstream assets that support its refineries. Since it knows how much volume these assets usually entail, it can provide Holly Energy Partners with an enviable amount of cash flow security that allows for consistent growth in distributions.

Strong balance sheet resulting in highly profitable growth potential

| MLP | Debt/EBITDA (Leverage) Ratio | EBITDA/Interest Ratio | WACC | ROIC |

|---|---|---|---|---|

| Holly Energy Partners | 4.1 | 6.4 | 5.18% | 13.91% |

| Energy Transfer Partners | 7.0 | 4.0 | 6.2% | 5.51% |

The lifeblood of the midstream MLP industry is access to growth capital, which in today's market conditions means that highly leveraged MLPs such as Energy Transfer Partners face a major problem. With such a large debt load and its unit price in the dolfrums, it will be hard to access cheap capital needed to complete the billions of dollars of new projects over the next few years.Should oil prices stay low over that time-frame, Energy Transfer will likely need to slash its payout to use its generated cash flows to fund investment and pay down debt.

On the flip side, Holly Energy Partners' much less levered balance sheet and low weighted average cost of capital means that it's likely to find an easier time of funding highly profitable investments in the years to come. Also keep in mind that Holly Energy Partners' growth capital needs are far smaller than those of Energy Transfer Partners or other large, highly leveraged midstream MLPs.

Bottom line

Given Holly Energy Partners' superb commodity-insensitive business model and realistic growth prospects over the next five years, I think it's clear that Wall Street is greatly undervaluing the company. If it maintains its conservative balance sheet and modest but consistent increases to the distribution, Holly Energy Partners should continue to crush both the majority of its peers and the market at large.