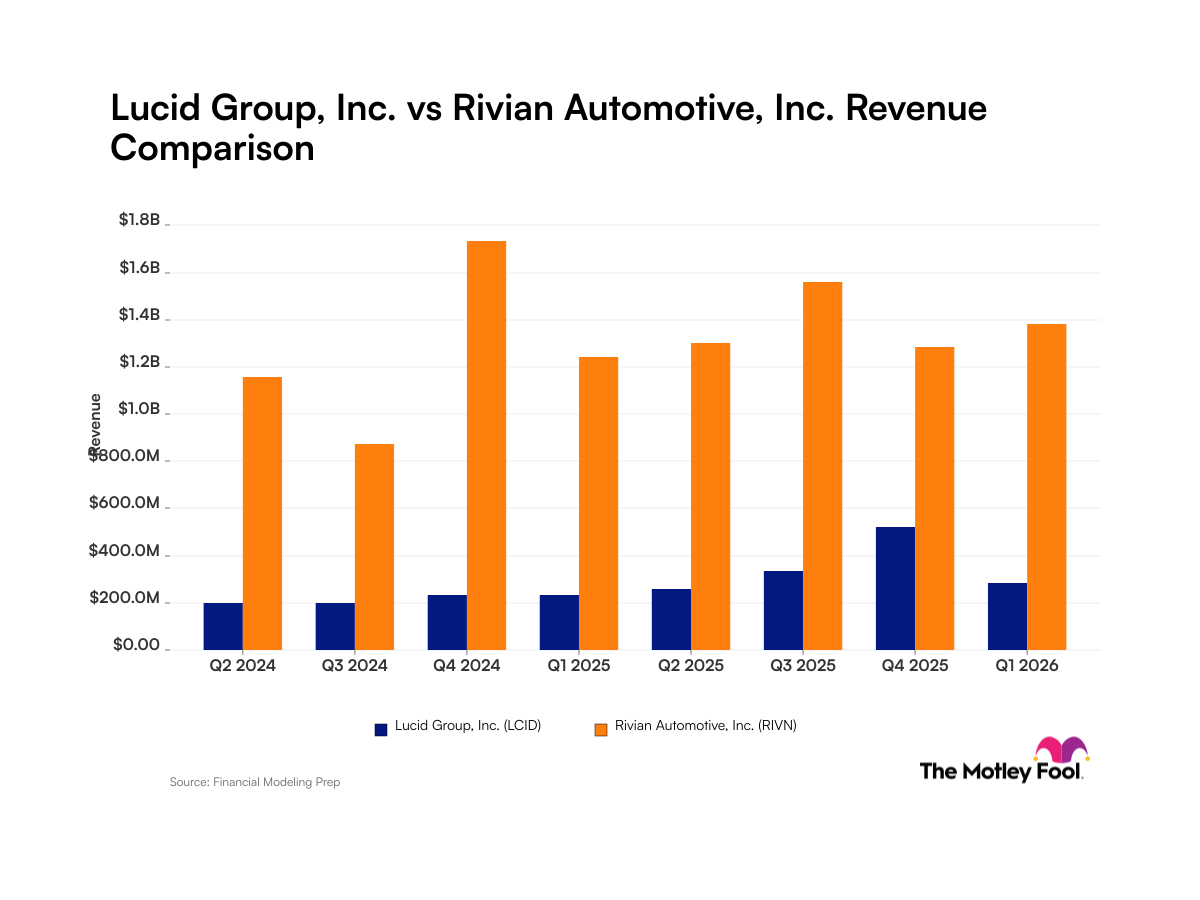

Lucid Group (LCID 4.75%), a U.S.-based electric vehicle manufacturer known for its luxury sedans and SUVs, reported its second-quarter earnings on August 5, 2025. The company’s revenue increased compared to Q2 2024 and it delivered a record number of vehicles, but operating losses continued and cash use accelerated. Revenue (GAAP) came in at $259.4 million, just above the $259.35 million analyst estimate, while Non-GAAP earnings per share (EPS) of $(0.24) missed the forecast by $0.02. The overall quarter showed progress in deliveries and partnerships but also highlighted ongoing cost pressures and a reduction in the production outlook.

| Metric | Q2 2025 | Q2 2025 Estimate | Q2 2024 | Y/Y Change |

|---|---|---|---|---|

| EPS (Non-GAAP) | $(0.24) | $(0.22) | $(0.29) | 8.6 % |

| Revenue (GAAP) | $259.4 million | $259.35 million | $200.6 million | 29.3 % |

| Adjusted EBITDA | $(632.1 million) | $(647.6 million) | 2.4 % | |

| Free Cash Flow (Non-GAAP) | $(1,012.9 million) | $(741.3 million) | (36.6 %) | |

| Vehicles Delivered | 3,309 | 2,394 | 38.2 % |

Source: Analyst estimates for the quarter provided by FactSet.

Business Overview and Critical Success Factors

Lucid operates in the premium electric vehicle (EV) space, developing and selling luxury sedans (the Lucid Air) and, more recently, sport utility vehicles (the Lucid Gravity). The company’s business model relies on technological innovation, direct-to-consumer sales, and vertical integration. Lucid designs its electric powertrain, battery systems, and much of its vehicle software in-house, aiming for both product differentiation and operational efficiency.

Recently, the company has focused on advancing proprietary technology, increasing production scale, and forming strategic partnerships. Key factors for success remain expanding production, managing costs, and building out its direct sales and service network. The ability to control manufacturing and technology development gives Lucid flexibility.

Quarterly Highlights and Key Developments

Vehicle deliveries reached a new high, with 3,309 vehicles delivered, up 38.2% from the prior year. Management stated, The company did, however, lower its full-year production guidance, now expecting 18,000 to 20,000 vehicles, down from a previous target of 20,000.

GAAP revenue increased by 29.3% compared to Q2 2024. and was slightly above analyst forecasts. Despite this growth, cost of revenue (GAAP) remained high at $531.8 million, Cost of revenue was more than double total sales, which resulted in another period of negative gross profit. Research and development spending fell about 4.6% compared to Q2 2024, while Selling, general, and administrative expenses (GAAP) rose 22.2% compared to Q2 2024. Operating losses and net losses to common stockholders (GAAP) both widened versus Q2 2024, with Net loss (GAAP, diluted) was $(855.3) million.

Lucid continued to emphasize its proprietary technology development efforts. The period saw the expansion of DreamDrive Pro, its advanced driver assistance system (ADAS), which now includes more autonomy features like hands-free and automated lane change. In parallel, Lucid entered a high-profile partnership with Uber (NYSE:UBER) and Nuro to deploy at least 20,000 Lucid Gravity SUVs with integrated Level 4 autonomous driving technology developed by Nuro over the next six years. Lucid's expanding access to Tesla (NASDAQ:TSLA) Supercharger stations further increases practicality for current and prospective owners of its EVs.

Despite these developments, the company’s financial performance reflected ongoing challenges. Free cash flow (non-GAAP) was negative, at $1.01 billion in outflows, and Total liquidity at period-end was $4.86 billion.

Looking Ahead: Management Outlook and Investor Considerations

Management provided a revised production target for fiscal 2025, lowering projections to 18,000 to 20,000 vehicles. No further quantitative outlook for top-line growth, margin, or profitability was given for coming quarters or the full year. Management instead signaled priorities such as ramping up Lucid Gravity production, tightening cost controls, and leveraging technology licensing and partnerships for future revenue streams. The leadership team is focused on executing its current model launches and building on recent strategic agreements such as the Uber-Nuro robotaxi collaboration.

For investors, important areas to watch include quarterly progress on delivery and production volumes, and developments in technology and new business partnerships. Monitoring cash burn, liquidity levels, inventory movements, and updates on the utilization and economics of new partnerships will be essential in evaluating Lucid’s operational progress and any future capital requirements. LCID does not currently pay a dividend.

Revenue and net income presented using U.S. generally accepted accounting principles (GAAP) unless otherwise noted.