Image source: The Motley Fool.

Advanced Micro Devices (AMD +7.91%)

Q3 2021 Earnings Call

Oct 26, 2021, 5:00 p.m. ET

Contents:

- Prepared Remarks

- Questions and Answers

- Call Participants

Prepared Remarks:

Operator

Hello, and welcome to the AMD third-quarter 2021 earnings call and webcast. At this time, all participants are in listen-only mode. A question-and-answer session will follow the formal presentation. [Operator instructions] As a reminder, this conference is being recorded.

It's now my pleasure to turn the call over to Laura Graves, corporate vice president, investor relations. Please go ahead, Laura.

Laura Graves -- Corporate Vice President, Investor Relations

Thank you, and welcome to AMD's third-quarter 2021 financial results conference call. By now, you should have had the opportunity to review a copy of our earnings press release and accompanying slideware. If you have not reviewed these documents yet, they can be found on the Investor Relations page of amd.com. Participants on today's conference call are Dr.

Lisa Su, our president and chief executive officer; and Devinder Kumar, our executive vice president, chief financial officer, and treasurer. This is a live call and will be replayed via webcast on our website. Before we begin, I would like to note that we will host our Accelerated Data Center Premiere virtually on November 8, with feature presentations by Dr. Lisa Su; and Data Center executives Forrest Norrod and Dan McNamara.

This event will also be available on amd.com. Dr. Su will also attend Credit Suisse's 25th Annual Technology Conference on Tuesday, November 30. Ruth Cotter, senior vice president, worldwide marketing, human resources, and investor relations, will attend the Barclays Global Technology, Media and Telecom Conference on Tuesday, December 7.

And our fourth-quarter 2021 quiet time is expected to begin at the close of business on Friday, December 10. Today's discussion contains forward-looking statements based on current beliefs, assumptions and expectations, speak only as of today and as such, involve risks and uncertainties that could cause actual results to differ materially from our current expectations. Please refer to the cautionary statement in our press release for more information on factors that could cause actual results to differ. We will refer primarily to non-GAAP financial measures during this call.

The full non-GAAP to GAAP reconciliations are available in today's press release and in the slides posted on our website. Now with that, I'll turn the call over to Lisa. Lisa?

Lisa Su -- President and Chief Executive Officer

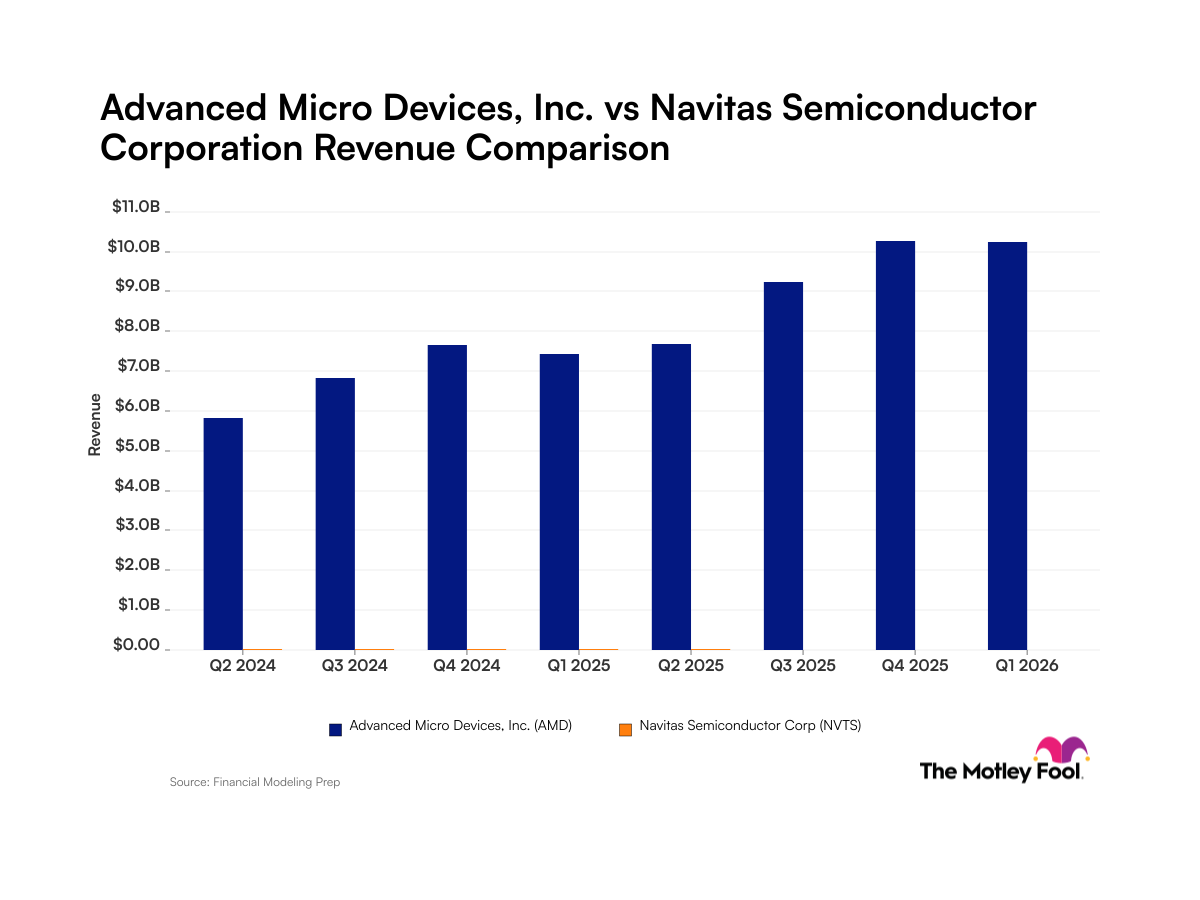

Thank you, Laura, and good afternoon to all those listening in today. Our business performed extremely well in the third quarter as our leadership product portfolio and strong execution drove record quarterly revenue, operating income, net income, and earnings per share. We delivered our fifth straight quarter of greater than 50% year-over-year revenue growth, with each of our businesses growing significantly year over year and data center sales more than doubling. Third-quarter revenue grew 54% to $4.3 billion.

Gross margin expanded by more than 4 percentage points and operating income doubled year over year. Turning to our computing and graphics segment. Third-quarter revenue increased 44% year over year to $2.4 billion, driven by our latest generation Ryzen, Radeon, and AMD Instinct processors. In client computing, sales grew by a strong double-digit percentage year over year and declined slightly sequentially.

Ryzen 5000 processor shipments increased by a double-digit percentage sequentially, resulting in a richer product mix as we believe we gained revenue share for the sixth straight quarter. In desktops, we launched our Ryzen 5000 processors with integrated Radeon graphics for the channel to strong demand as third-party reviews highlighted the leadership computing and graphics capabilities and energy efficiency of these processors. In notebooks, Acer, Asus, HP, and Lenovo, all expanded their mobile offerings powered by Ryzen 5000 mobile processors as we continue gaining momentum in the premium consumer, gaming, and commercial markets. Commercial client growth year over year was based on new deployments across public sector and Fortune 1000 technology, energy, and automotive customers as the number of AMD-based commercial notebook designs available from the largest OEMs increased significantly year over year.

We're also seeing strong growth in the workstation market. According to IDC, Threadripper PRO processors now powered the best-selling workstations in their category in both North America and EMEA as we continue winning high-volume deployments across key verticals including media and entertainment, engineering, architecture, and automotive. In graphics, revenue more than doubled year over year and grew by a strong double-digit percentage sequentially, driven by shipments of our next-generation AMD CDNA 2 data center GPUs and demand for Radeon 6000 GPUs in the channel. AMD RDNA 2 GPU sales grew significantly in the quarter as we ramped production and expanded our top to bottom portfolio with the launch of the midrange Radeon RX 6600 XT cards that deliver leadership 1080p gaming performance at their price point.

Data center graphics revenue more than doubled year over year and quarter over quarter, led by shipments of our new AMD CDNA 2 GPUs for the Frontier exascale supercomputer at Oak Ridge National Laboratory. Frontier was architected specifically to deliver breakthrough HPC and AI compute performance and provide a blueprint for how supercomputing, enterprise, and cloud customers can enable exascale-level performance over the coming years by combining AMD CPUs, GPUs, and software. We are very pleased with the performance of our AMD CDNA 2 GPUs and look forward to providing more details on their leadership performance next month. Turning to our enterprise, embedded and semi-custom segment, revenue increased 69% year over year to $1.9 billion, driven by strong growth in EPYC processor and semi-custom sales.

Semi-custom revenue grew sequentially and year over year as demand for the latest Microsoft and Sony consoles remains very strong. We expect semi-custom revenue to increase sequentially in the fourth quarter as we further ramp supply to address the ongoing game console demand. Turning to server. We delivered our sixth straight quarter of record server processor revenue as sales more than doubled year over year and grew by a significant double-digit percentage sequentially.

Third-gen EPYC processors continue ramping faster than the prior generation and contributed the majority of our server CPU revenue in the quarter. In cloud, multiple hyperscalers expanded their third-gen epic processor deployments to power their internal workloads. And both Microsoft Azure and Google announced multiple new AMD-powered instances. Cloudflare, Vimeo, and Netflix also all recently announced new deployments powered by EPYC processors, with Netflix highlighting how they doubled their streaming throughput per server while also reducing their TCO.

Enterprise growth was particularly strong in the quarter as the more than 100 third-gen EPYC processor platforms from Dell, HPE, Lenovo, Supermicro, Cisco, and others ramp into broader end customer deployments. We expanded our wins in the quarter with Fortune 1000 financial services, automotive, and aerospace companies and see significant ongoing growth opportunities as our enterprise server pipeline has more than doubled year over year. In supercomputing, we won multiple installations in the quarter, highlighted by Argonne National Laboratory selecting third-gen EPYC processors to power the new Polaris supercomputer that will be used to test and optimize software in preparation for future exascale class systems. Overall, we are very pleased with the momentum we have built in our data center business as server CPU and GPU revenue grew to a mid-20s percent of overall revenue in the quarter.

Turning to our Xilinx acquisition. We are making good progress toward securing the required regulatory approvals and remain on track to close by the end of the year. The Xilinx acquisition provides significant benefits to AMD, including expanding our product portfolio with leadership adaptive computing and AI solutions and further diversifying our customer base into complementary markets, including wired and wireless communications, industrial and automotive. In closing, our record third-quarter results and the significant acceleration of our business in 2021 demonstrate that we have the right products and strategies to drive best-in-class growth and significant shareholder returns.

We continue growing faster than the market, driven by our consistent execution and the investments we have made to build leadership products. Our supply chain team has executed extremely well in a challenging environment, delivering incremental supply throughout the year, supporting our strong revenue growth. We are also investing significantly to secure additional capacity to support our long-term growth. Our product portfolio and road maps have never been stronger, and I look forward to sharing more details about our next-generation server CPUs and GPUs at our Accelerated Data Center Premiere on November 8.

Now I'd like to turn the call over to Devinder to provide some additional color on our third-quarter financial performance. Devinder?

Devinder Kumar -- Executive Vice President, Chief Financial Officer, and Treasurer

Thank you, Lisa, and good afternoon, everyone. AMD had another excellent quarter. Our leadership products and growing data center momentum are driving record revenue, record profitability, and significant cash flow generation. Third-quarter revenue was $4.3 billion, up 54% from a year ago, driven by strong revenue increases across all businesses and up 12% from the prior quarter.

Gross margin was 48%, up 440 basis points from a year ago, driven by strong revenue mix and competitive products. Operating expenses were $1.04 billion, compared to $706 million a year ago as we continue to invest in our long-term product road maps and scaling our business. Operating income more than doubled to $1.06 billion, up $530 million from a year ago, driven primarily by revenue growth. Operating margin was 24%, up from 19% a year ago.

Net income grew to $893 million, up $392 million from a year ago. Diluted earnings per share was $0.73, compared to $0.41 per share a year ago. This includes a 15% effective tax rate, compared to 3% a year ago. Now turning to the business segment results.

Computing and Graphics segment revenue was $2.4 billion, up 44% year over year, driven by significantly higher client and graphics processor revenue. Computing and graphics segment operating income was $513 million or 21% of revenue, compared to $384 million or 23% a year ago. The increase in operating income was primarily driven by higher revenue, which more than offset higher operating expenses. Operating margin was slightly lower year over year, primarily due to investments in R&D and go-to-market.

Enterprise, embedded, and semi-custom segment revenue was $1.9 billion, up 69% from $1.1 billion the prior year. The strong revenue increase was primarily driven by significantly higher EPYC processor and semi-custom sales. EESC operating income was up significantly at $542 million or 28% of revenue, compared to $141 million or 12% a year ago. Operating income growth was primarily driven by higher revenue and richer product mix, partially offset by higher R&D and go-to-market expenses.

Turning to the balance sheet. Cash, cash equivalents and short-term investments were $3.6 billion. We utilized $750 million to repurchase more than 7 million shares of common stock in the third quarter of 2021 as part of our ongoing stock repurchase program. Free cash flow was $764 million, compared to $265 million in the same quarter last year and $888 million in the prior quarter.

On a quarter-over-quarter basis, free cash flow was lower as we made strategic investments in long-term supply chain capacity to support future revenue growth. Inventory was $1.9 billion, up $137 million from the prior quarter in support of continued revenue growth. Let me now turn to the fourth-quarter outlook. Today's outlook is based on current expectations and contemplates the current global supply environment and customer demand signals.

We expect revenue to be approximately $4.5 billion, plus or minus $100 million, an increase of approximately 39% year over year and approximately 4% sequentially. The year-over-year increase is expected to be driven by growth across all businesses. The quarter-over-quarter increase is expected to be driven by higher server and semi-custom sales. In addition, for Q4 2021, we expect non-GAAP gross margin to be approximately 49.5%; non-GAAP operating expenses to be approximately $1.15 billion; non-GAAP interest expense, taxes and other to be approximately $170 million; and the diluted share count to be approximately 1.22 billion shares.

For the full-year 2021, we now expect revenue to increase approximately 65% over 2020, driven by growth across all businesses, up from the prior guidance of 60%. In addition, we continue to expect gross margin to be approximately 48% for the full year. In closing, we delivered another outstanding quarter with very strong year-over-year revenue growth, significant financial momentum, and record profitability. Our leadership products position us well to drive future growth, significant cash generation and strong shareholder returns.

With that, I'll turn it back to Laura for the question-and-answer session. Laura?

Laura Graves -- Corporate Vice President, Investor Relations

Thank you, Devinder. Operator, we're ready for our first question.

Questions & Answers:

Operator

Thank you. We'll now be conducting your question-and-answer session. [Operator instructions] One moment, please, while we poll for questions. Our first question today is coming from Blayne Curtis from Barclays.

Your line is now live.

Blayne Curtis -- Barclays Investment Bank -- Analyst

Hey, good afternoon and great results. Thanks for taking my questions. Just kind of curious, the overall outlook for Q4. So computing graphics being down.

I was just curious if that was more the supply. You're still growing sequentially. And obviously, I would assume you prioritize servers. Just kind of curious what you're seeing in the computing graphics market.

And is it anything related to supply constraints for you that would be down sequentially or maybe downstream constraints? And then maybe for Devinder. Just curious, you're still growing gross margin. I'm assuming embedded, semi-custom, and service kind of offsetting. So just kind of walk us through the nice increase in gross margin for Q4.

Lisa Su -- President and Chief Executive Officer

Yeah. Sure, Blayne. Thanks for the question. So as it relates to the fourth quarter and where we are.

Look, we're overall very pleased with our performance in terms of the second half of the year. It's playing out about what we expect it to be in the PC market. So as you're asking about computing and graphics. We had seen that the PC market and user demand is strong overall, but there are some matched set constraints in the PC market.

And so for that reason, we've called the PC market really flattish. I would not have said down. I would have called it flattish as we look into the fourth quarter. However, as we look overall at the business, I think the data center business has performed very well, and we see strong demand there, and we're continuing to see that.

And as well, the console business, overall gaming is also quite strong. And so we see growth in servers and semi-custom as we go into the fourth quarter. And then on the margin dynamics, Devinder, do you want to cover that?

Devinder Kumar -- Executive Vice President, Chief Financial Officer, and Treasurer

For Q4?

Lisa Su -- President and Chief Executive Officer

Yeah.

Devinder Kumar -- Executive Vice President, Chief Financial Officer, and Treasurer

Yeah. So Q4, you know, it is up slightly based from our guidance, 1 point from Q3, and that's really product mix, higher margin from server, offset by semi-custom revenue also been higher going from Q3 to Q4. So we're very pleased with the progress on the gross margin. As you look at the Q3 results, up 440 basis points from last year, up 80 basis points from last quarter and the progression into Q4, obviously driven by the server, our revenue growing.

I'm very pleased with that also.

Blayne Curtis -- Barclays Investment Bank -- Analyst

Thanks.

Lisa Su -- President and Chief Executive Officer

Thanks, Blayne.

Operator

The next question today is coming from Vivek Arya from Bank of America. Your line is now live.

Vivek Arya -- Bank of America Merrill Lynch -- Analyst

Thanks for taking my question, and congratulations on the strong results and the consistent execution. Lisa, how are you feeling about the spending environment in the data center as you look over the next several quarters? And especially your server road map versus the competition because they are planning to launch several new and important products early next year. So I was just wondering how you're thinking about the competitive landscape and the spending landscape over the next year.

Lisa Su -- President and Chief Executive Officer

Sure. So thanks, Vivek, for the question. I think overall, we're feeling very, very good about the server business or the data center market. I think from a market standpoint, we've seen a strong market year in 2021 in both cloud and enterprise and we see that continuing into 2022.

I think from a competitive position standpoint, I think Milan is extremely well-positioned. So we were very pleased with sort of the adoption rate of Milan. We said that we expected it to grow faster than Rome, and it has. And so the crossover with Milan and Rome in the third quarter is an important metric for that.

Going into the fourth quarter, we continue to see a strong environment. And then as the competitive environment goes into 2022, we always expect the competition to be strong, but our focus has been consistent execution of our road map, and we feel very good about Zen 4 and Genoa in 2022. I think we feel very good about the competitive positioning there. And we continue to believe that data center is the most strategic part of our business, and we're making good progress with our customers and partners.

Vivek Arya -- Bank of America Merrill Lynch -- Analyst

Got it. And for my follow-up, Lisa, AMD has done very well in terms of gaining share at the hyperscalers. Where are you in that journey? Is there still a lot of share gains to be had at hyperscalers? And importantly, can you repeat that in the enterprise? Or do you think your competitors' incumbency limits the share gain opportunity in the enterprise? Thank you.

Lisa Su -- President and Chief Executive Officer

Yeah. So Vivek, what I would say there is, our business has been more cloud weighted with the hyperscalers than enterprise, that continued here in the third quarter. I do believe that there is significant additional opportunity for us in the cloud. So as we work with these partners, it is about sort of expansion of workloads.

Really, there's more tailoring of workloads, as well as we go forward. And then there's also just more customers and broader penetration in both Tier 1 and Tier 2 cloud guys. So I think that's a good market for us. On the enterprise side, I would say, we saw a very strong enterprise quarter here in the third quarter.

I think the strength of Milan with our OEMs in terms of the breadth of the platforms, is very good, and we're seeing a good traction with sort of Fortune 1000 companies. So I would say, overall, I think we see a growth trajectory for both our cloud and enterprise business. I think in the enterprise, the key thing has been to get more familiarity with EPYC, and we've made very good progress there. And so I feel very good about where that's going.

Vivek Arya -- Bank of America Merrill Lynch -- Analyst

OK. Thank you, Lisa.

Lisa Su -- President and Chief Executive Officer

Thanks.

Operator

Our next question is coming from Matt Ramsay from Cowen. Your line is now live.

Matt Ramsay -- Cowen and Company -- Analyst

Obviously, Lisa has some really strong progress with data center crossing, I guess, a quarter of the business here with the results. I did want to ask a question specifically on your server business in China. Your competitor called out China and some of the turmoil that's gone over there as a reason why some of their cloud business had some headwinds in the third quarter. And maybe you could comment on how you see spending over the last quarter and then in the next couple of quarters, specifically in that end market in China.

And then I have a follow-up. Thanks.

Lisa Su -- President and Chief Executive Officer

Sure, Matt. So, again, what I would say is our data center business performed very well in the third quarter, that was across both cloud and enterprise. And in cloud, that was across geographies. So we haven't seen anything particular as it relates to China or there.

What I would say is we continue to work with the breadth of customers. And we're in the process of really rolling out sort of broader adoption across the customer set. So I think we saw a pretty normal environment for demand.

Matt Ramsay -- Cowen and Company -- Analyst

Thanks for clearing that up. As my follow-up, kind of unrelated. You guys mentioned in the comments, still plans to get the Xilinx deal closed by the end of the year. And I think that's important as then there's a lot of things that you can talk about more, maybe more openly about the heterogeneous compute strategy for the business over the long term.

Lisa, maybe you could walk us through to the extent that you can talk about it, obviously, there are some things that you can't talk about. But to the extent you can, what milestones you've achieved behind the scenes that make you feel confident, and what hurdles are still there to have the confidence? I mean I guess we've got weeks till we get into the month of December and things kind of slow down a little bit regulatory-wise. So I just wonder what gives the confidence that we can get there and what we should expect. Thank you.

Lisa Su -- President and Chief Executive Officer

Sure, Matt. So look, we've been working diligently on the closure of the Xilinx acquisition. I would say we're through the vast majority of what we need to do in the regulatory front. We're finishing up here.

And there's very good progress on the integration side. So we've done a lot on the integration. I think we're excited with the plans that we have. And then on the regulatory front, again, as I said in the prepared remarks, we've made good progress, and we believe we're on track to close at the end of the year.

Operator

Thanks. Our next question --

Lisa Su -- President and Chief Executive Officer

Operator, go ahead.

Operator

Certainly. Our next question is coming from Toshiya Hari from Goldman Sachs. Your line is now live.

Toshiya Hari -- Goldman Sachs -- Analyst

Hi, good afternoon. Thank you so much for taking the question and congrats on the strong results. Lisa, I had two questions as well. First, on your outlook for 2022.

I realize it's early, and I certainly don't expect you guys to provide a point estimate. But I think people are kind of concerned that you've been sort of overgrowing, if you will, relative to your long-term growth rate. You grew 45% last year. You're on track to grow 65% this year, given your long-term through-cycle growth target of 20%.

Again, there is concern that you could decelerate going into next year, given PC dynamics and competitive dynamics and so on and so forth. So, again, I don't expect you to give any quantification of next year, but if you could describe the year qualitatively, what are the potential pluses and minuses at this point, that would be super helpful? And then I've got a quick follow-up.

Lisa Su -- President and Chief Executive Officer

Sure. So look, as you said, it's a little bit early to talk about quantitatively. I'll cite qualitatively, what we see is, look, we see a positive demand environment. And that's a market statement, but that's also an AMD statement, right? I think the strength of our product portfolio has multiple growth vectors.

Data center continues to be a very important one for us. I think we're -- we continue to make progress in the graphics market, and we think graphics is a good growth vector. Our console business, we would expect would be -- I mentioned earlier that it'd be up in the fourth quarter, and we would expect it to be up in 2022, just given the strength of the demand environment there. And so on the PC side, the comments I'll make on the PC side are -- the end-user demand appears to be strong.

So there's a good amount of refresh going on, whether you're talking about consumer and your high-end consumer or commercial or gaming. There are some supply constraints around matched sets that we believe will continue into the first half of the year. That being the case, what we're using from a planning assumption standpoint, is that the PC market may be flattish as we go from 2021 into 2022. But even within that environment, we think there are opportunities for us to continue to grow.

So, overall, I think we're very focused on execution, very focused on working with our customers to make sure that we're aligned with what they need and overall feel very good about our product portfolio going into 2022.

Toshiya Hari -- Goldman Sachs -- Analyst

Got it. That's super helpful. Thank you. And then as my quick follow-up, a similar question on gross margins.

I'm not sure if this is for Lisa or Devinder. You're guiding Q4 to 49.5%, which is obviously significant progress from a year ago. Given some of the dynamics you've talked about whether it be the growth potential in server CPU, the mix within server CPU, and I'm sure the mix dynamics on the client side, I think most of us do expect a pretty nice positive trajectory into 2022, potentially with a five handle in terms of, again, gross margins. But any risks or any headwinds that we should be aware of? I think your foundry partner is raising pricing.

There is cost inflation generally across the board, but any risk items that we should think about at this point? Thank you.

Devinder Kumar -- Executive Vice President, Chief Financial Officer, and Treasurer

I wouldn't say it, but I think is about managing the situation. As Lisa said, with the growth factors that we have, we expect to continue making progress from where we are currently and especially predicated on the competitive leadership products we have. We're very pleased with the progress we've made over the last few years. But without getting to specifics, I think you can assume that we continue to make progress with the mix of revenue, mix of products, and the competitive products that we are introducing also into 2022.

Toshiya Hari -- Goldman Sachs -- Analyst

Thank you.

Operator

Thanks. Our next question is coming from Stacy Rasgon from Bernstein Research. Your line is now live.

Stacy Rasgon -- Sanford C. Bernstein -- Analyst

Hi, guys, thanks for taking my questions. My first one, I wanted to ask about data center GPU. I know you said it more than doubled. But can you give us an approximate feeling for how big that is it? Are we still talking like tens of millions of dollars? Or is it larger than that? And what are your expectations for how that's going to ramp as Frontier and some of the other supercomputers that a lot of that stuff is going into our ramping over the next like couple of years?

Lisa Su -- President and Chief Executive Officer

Sure. So Stacy, on the data center GPU side, the third quarter was a larger quarter for the data center GPU. This is where we shipped the Frontier shipments that are now in the build cycle. It is still a relatively small business compared to the CPU side.

So our expectation is that going into the fourth quarter, it's a lumpy business for us. So Q3 was a strong quarter given the shipments of -- for Frontier. We would expect, as we go into the fourth quarter, that it will be down sequentially quarter on quarter. But still, it's a strong growth year overall for a business that we think is a significant strategic growth driver for us over the next few years.

Stacy Rasgon -- Sanford C. Bernstein -- Analyst

Thank you. For my follow-up, I just wanted to ask about Q4. So obviously, you would sort of give an implied guidance for Q4 last quarter. The guidance now is obviously decently higher.

Can you just talk a little bit about what is driving that upside relative to where your expectations were last quarter?

Lisa Su -- President and Chief Executive Officer

Devinder, you want to talk about that? Or --

Devinder Kumar -- Executive Vice President, Chief Financial Officer, and Treasurer

On the revenue, I think -- go ahead.

Lisa Su -- President and Chief Executive Officer

I'm sorry. Were you asking about revenue or margin, Stacy?

Stacy Rasgon -- Sanford C. Bernstein -- Analyst

Well, both, if you're willing to answer both, both.

Lisa Su -- President and Chief Executive Officer

OK. All right. Let me start and then let -- I want to make sure I answer your question. How's that? So look, on the revenue side, when we look at the sequential growth, we have been able -- look, the supply chain, this is about really supply chain optimization.

And we have been able to secure some additional supply, given some of the work that we've been doing. And we see strong demand across the board. But sequentially, what we're guiding to is stronger server demand, as well as gaming, and gaming includes the semi-custom game consoles, as well as our graphics business is doing quite well as well. And then in terms of the sequential margin, it's similar.

I mean we're having servers, some improved mix and graphics driving upside. And that's partially offset by the consoles which are below corporate average. But net-net, I think it's a positive sequential both on revenue and margin.

Stacy Rasgon -- Sanford C. Bernstein -- Analyst

I guess what I'm asking is, for example, are your expectations for servers into Q4 now higher than they were three months ago when you gave implied guidance for Q4?

Lisa Su -- President and Chief Executive Officer

Yes. Yes, it is.

Stacy Rasgon -- Sanford C. Bernstein -- Analyst

Got it. OK. Thank you very much.

Lisa Su -- President and Chief Executive Officer

Sure.

Operator

Thanks. Our next question today is coming from Joe Moore from Morgan Stanley. Your line is now live.

Joe Moore -- Morgan Stanley -- Analyst

Thank you. I'm wondering if you could talk about graphics a little bit. It seems like that's the business that's probably struggled the most to get silicon and you've shown some pretty nice growth there. What's the prognosis for that business going forward? And in the past, you've said you're comfortable that there's relatively low cryptocurrency exposure there.

Is that still the case?

Lisa Su -- President and Chief Executive Officer

Yes. Sure, Joe. Look, the graphics business did have a strong third quarter. I think that's true for graphics gaming, as well as data center GPU.

I think the portfolio that we have there with RDNA 2 has turned out really well. So we're pleased with how it's positioned competitively in the marketplace. And overall, gaming has been a secular trend that has continued with very strong demand. In terms of crypto, our view is that it's really negligible revenue for us in the third quarter.

It's not a segment that we have been servicing. We've tried very much to try to keep our gaming graphics focused on gamers. And we were able to increase some of the supply for graphics, and that's one of the reasons that we saw the sequential growth that we saw. And going into the fourth quarter next year, again, I think we see gaming overall as a strong segment for us, and the product set is very good.

So we feel good about it.

Joe Moore -- Morgan Stanley -- Analyst

Great. Thank you very much.

Lisa Su -- President and Chief Executive Officer

Thanks.

Operator

Thank you. Our next question is coming from Aaron Rakers from Wells Fargo. Your line is now live.

Aaron Rakers -- Wells Fargo Securities -- Analyst

Yeah. Thanks for taking the question. I have two quick questions, if I can as well. Just kind of sticking on the expectations in the next year, appreciating that you're not going to give a full guide.

I'm just curious how we should think about the semi-custom business given how sizable that's been to the overall growth in 2021. Any framing of how you expect 2022 to shape up at this point?

Lisa Su -- President and Chief Executive Officer

Sure, Aaron. So, you know, again, if you look at the overall growth that we had in 2021, I would say it was actually quite balanced across all of our businesses. The semi-custom business was in the second year of ramp, and demand has exceeded supply. We've been able to ramp that as we've gone through the year.

As we look into 2022, the historical view of game consoles has been year 4 is the peak, at least that's what it was in the last generation. What we expect in this generation is, again, very strong demand going into 2022. So we would expect it to grow into 2022, which would be the third year of the cycle, and then we'll see what happens after that. But overall, I think our view is we have a very balanced business with multiple growth drivers across data center, PCs, graphics, as well as consoles.

Aaron Rakers -- Wells Fargo Securities -- Analyst

That's very helpful. And then the follow-up question is on your own supply chain side. I know in the prepared comments you said working on securing adequate supply given your growth trajectory. Are you currently able to meet on the goal of the demand that you currently see? And can you give any color of what -- how we should think about the supply situation on your end?

Lisa Su -- President and Chief Executive Officer

Yeah. So, I mean, we've been working on ramping the supply chain really for more than a year. If you think about sort of dynamics here. What I'd like to say is, overall, the demand has been very, very high.

So the fact that we can grow revenue this year 65% year on year, I think, is a testament to the supply chain work. I think if we had more supply, we could certainly ship more. That being the case, I think we're prioritizing in the most strategic segments. And we have invested significantly in capacity for additional capabilities, and we'll see some of that come online as we go through 2022.

And we're going to continue to be aggressive to secure additional capacity because we believe our product portfolio will enable that growth.

Aaron Rakers -- Wells Fargo Securities -- Analyst

Thank you.

Lisa Su -- President and Chief Executive Officer

Thanks.

Operator

Thanks. Our next question today is coming from John Pitzer from Credit Suisse. Your line is now live.

John Pitzer -- Credit Suisse -- Analyst

Good afternoon, guys. Congratulations, Lisa. Lisa, my first question is back on the supply side of things. I'm just wondering if you can help me better understand, was it more of an issue in your PC business or your server business? And I guess, especially as we look into next year, as supply begins to loosen up, this year, given how tight the overall ecosystem was, competing on price didn't make a lot of sense.

As supply begins to accelerate across the ecosystem, how are you thinking about pricing, especially in lieu of your large competitor kind of resetting their gross margins for next year? In your view, does that give them more wiggle room? Or do you think that they're being pretty benign on the pricing side of things on that gross margin reset?

Lisa Su -- President and Chief Executive Officer

Yeah. So maybe let me -- there's a lot of various aspects to that, John. So let me try to take it in pieces. As it relates to current supply, I want to make sure that we're clear.

I mean we have brought on a tremendous amount of additional supply, and that's part of the reason that we overachieved the Q3 results and then we guided higher in Q4. So I do think that we have done a lot of work on our supply chain. In the PC market, in particular, I think the market is not necessarily constrained on CPUs, but more constrained on matched sets. And so we're trying to ensure that we're not building inventory in the channel.

And that's part of the optimization that we do is to ensure that as we ship sell-in processors that we see matched sets to sell through. And so from that standpoint, we think inventory is very healthy at the OEMs, and that's an important factor as we go into 2022. As it relates to what happens with the pricing environment as supply eases up. I think, right now, what we see is a -- again, it's an environment where most people are prioritizing supply.

As we go into 2022, though, I think this is all about the product. And what we view is -- our focus in sort of our product line has been moving up the stack, ensuring that we're providing significant value to our customers in terms of total cost of ownership on the server side and innovative features and capabilities on the PC side and the graphics side. And we're going to continue to do that. I mean we're excited about our product portfolio into 2022.

We're going to continue to be very aggressive on the overall road map. And with that, I think our game plan is exactly what it was, what it always has been, which is lean into the product cycle, and the deep customer relationships and continue to build that out over time.

John Pitzer -- Credit Suisse -- Analyst

That's helpful. And then as my follow-up, Devinder, you did a good job kind of explaining the year-over-year changes in operating margins in the compute and graphics business. I'm wondering if you could talk a little bit about sequentially what happened. Revenue was up and op margins were down a little bit.

Is that just the influence of the very strong growth in GPUs going into the data center? Because it sounds like in the core compute business mix probably got better sequentially for you. So I'm just trying to make sure I understand all the dynamics you play.

Devinder Kumar -- Executive Vice President, Chief Financial Officer, and Treasurer

So, if you're talking about the CG segment, it's investments, right? Some investments in R&D and go to market. And also, we have a lot of new products coming into 2022, and there's expenditure involved ahead of the curve before you introduce the products in the next year. And that's really what happened in the transition quarter over quarter.

John Pitzer -- Credit Suisse -- Analyst

Perfect. Thank you.

Operator

Our next question today is coming from Chris Caso from Raymond James. Your line is now live.

Chris Caso -- Raymond James -- Analyst

Yes. Thank you. Good evening. First question is about the supply constraints and how that affects seasonality as we go into the beginning of next year.

And obviously, you're making efforts to bring on more supply. You spoke about in PC these constraints with regard to matched sets. I'm sure at this point, you don't want to provide guidance for Q1, but how should we be thinking about seasonality for Q1 as we contemplate these supply constraints?

Lisa Su -- President and Chief Executive Officer

Yeah, Chris, I think it's a little bit early to talk about Q1. I mean I think -- let's see what would we say about seasonality. I don't have a lot to say other than typically, Q1 is down from Q4. That's typically what the pattern is, given the consumer-related businesses.

It might be a little bit subseasonal as we go into this first quarter just given the demand environment, but we'll have to see how things play out over the next couple of months.

Chris Caso -- Raymond James -- Analyst

All right. A little bit of a bigger picture question for my second question. And we've heard and seen from some of the hyperscalers is a trend of, in some cases, doing some custom designs, doing it on their own, often with ARM-based designs. Do you consider that an opportunity or a threat for AMD? And to what extent are you engaged with some of those hyperscalers on some of these custom designs because you do have an IP portfolio yourself?

Lisa Su -- President and Chief Executive Officer

Yeah. Chris, on that, we definitely view it as an opportunity, right? So I think what's happening in the data center market is that as the need for compute gets larger, sort of this tailoring of compute for the various workloads is an important trend. I think our IP portfolio today is very strong. I think it will even be stronger given some of the things that we have in plan to allow more tailoring.

And we are working very closely with a number of hyperscalers on sort of the vision of compute over the next few years and how we might put together some different solutions between our CPU, GPU, interconnect capability and then with the addition of Xilinx as well coming into our portfolio. So, lots of opportunity there for customization. I think that's a key trend that we're certainly going to lean into.

Chris Caso -- Raymond James -- Analyst

Thank you.

Laura Graves -- Corporate Vice President, Investor Relations

Thank you, Chris. Operator, two more questions, please.

Operator

Certainly. Our next question is coming from Ross Seymore from Deutsche Bank. Your line is now live.

Ross Seymore -- Deutsche Bank -- Analyst

Thanks. Let me ask a question echoed with a congrats of other people on the strong results. Lisa, I just wanted to ask about the comparison on your CNG side between the C and the G and specifically on the client graphic side of things. Clearly, this year has been a really strong year for AMD.

Can you just talk about the go-forward on the client side in that? I think we're all pretty well aware of what's going to happen in the data center GPU side. But how do we reconcile your commentary on where you think the PC market would be in the flattish area versus the strength you've had in GPUs this year in a strong GPU market? Do you think that continues next year? How much of it is AMD specific? Or if the PC market is weaker, is that something that's a little bit of a headwind for AMD?

Lisa Su -- President and Chief Executive Officer

Yeah. So again, what I would say is our market share is still, I would say, underrepresented, whether you're talking about the client sort of CPU or APU side or the GPU side. I think what we have seen here in the third quarter and then into the second half of the year is our graphics business has performed quite well. It is channel driven in the sense that there's still strong demand among gamers for GPUs.

As we go into 2022, though, I don't view sort of the PC market as a headwind for the company. I think as we look at all of these markets, of course, we do a bunch of scenario planning if the market is up or if it's down. I think there are many who think that the market may be up. There are some who think that market may be down.

And that's why we're choosing to model sort of the base case is flattish. But even within that market, whether you're talking about client CPUs or -- client GPUs, we think we have opportunities to gain share and grow in that business, just given the strength of our product portfolio and the fact that we are sort of underrepresented to we think the -- sort of what we can expect given those products.

Ross Seymore -- Deutsche Bank -- Analyst

Thanks for that. And I guess as my follow-up, just one for Devinder on the opex side, and I'll give the same disclaimer that I know you're not going to give any specifics about next year, but you guys have done a great job of lowering your opex intensity throughout this year. I think you're going to be closer to 24% versus your 26% to 27% entering the year and 25% as of last quarter. So, great expansion there in margins and better leverage.

As we look forward, though, I think the third quarter was the first time where you guys spent enough that it actually impacted a segment where the operating margin fell a little bit. And I think we all understand why you're doing that and it feeds great growth. So it's not a negative. But as I look into '22, do you think next year can be another year where your operating leverage is positive? Or do you expect to be able to spend closer to your former targets in kind of the 25% to 27% of sales range?

Devinder Kumar -- Executive Vice President, Chief Financial Officer, and Treasurer

I think, fundamentally, and what you observe is right, very disciplined from an opex standpoint, investing in the growth is important. Many of the things that Lisa talked about earlier is all about growth in many different vectors. And obviously, that requires funding from an opex standpoint, whether it's R&D, go-to-market, hiring, which we are doing from a viewpoint of the growth in the company. And I think from a modeling standpoint, a guidance standpoint, you can assume that the growth in opex will be lower in revenue.

Margin continues to expand, opex flattish or even down. I mean you can model it, but very disciplined on that standpoint and making sure that we are investing for the growth is a top priority for us.

Ross Seymore -- Deutsche Bank -- Analyst

Thank you.

Operator

Thank you. Our final question today is coming from Timothy Arcuri from UBS. Your line is now live.

Timothy Arcuri -- UBS -- Analyst

Thank you for fitting me in. I had two. I guess, first, Lisa, no one has asked about software yet. I was wondering if you can update us on your software efforts.

And maybe as you get close to closing Xilinx, how much that sort of changes things for you on the software side and maybe how your search for software talent has been? And then I had a follow-up.

Lisa Su -- President and Chief Executive Officer

Sure, Tim. So, yes, we continue to invest heavily in software, particularly on the data center GPU side. We -- with our next-generation GPU architecture, MI200, which we'll be talking a little bit about in the next few weeks, we have made significant investments in progress. Our focus has been on using sort of the Frontier beachhead with high-performance computing and expanding that into AI and working with our partners on that software development.

So overall, continue to make good progress there. I think the Xilinx acquisition and bringing in sort of that software talent also provides opportunities to optimize across the overall portfolio in terms of just the software infrastructure that people want in an overall ecosystem. So very strategic area that we're making good progress in.

Timothy Arcuri -- UBS -- Analyst

Thanks a lot. And I guess just last question for me. So server share, if I look at your guidance for Q4, it looks like you're going to be in the 12.5% to 13% share, if I use the entire TAM, and that's up like 500 basis points versus last year Q4. So I guess the question is, like, is that a reasonable trajectory into next year? As if we're sitting to 12 months from now, would you be surprised if you gained another 500 basis points next year? And sort of where do you think about where that share can go?

Lisa Su -- President and Chief Executive Officer

Yeah. So, you know, I think, overall, our server trajectory has been very strong. I mean I think we're very pleased with the trajectory here in 2021. I think having a number of quarters where we're doubling the revenue year on year kind of speaks to the progress there.

As we go into 2022, we still believe we are a share gainer in that environment just given the strength of our portfolio and let's call it, platforms that are still yet to launch across our customer set. So we're continuing to play out the strategy of a data center being a place where our technology is very differentiated. And we think that's true in the third generation with EPYC, and we certainly are very focused on ensuring that the next generation with Zen 4 and Genoa are similarly well-positioned in the marketplace.

Timothy Arcuri -- UBS -- Analyst

Thanks a lot.

Laura Graves -- Corporate Vice President, Investor Relations

Thank you, Tim.

Operator

We reached the end of our question-and-answer session. I'd like to turn the floor back over for any further or closing comments.

Laura Graves -- Corporate Vice President, Investor Relations

We're good. Thank you very much, operator, and thank you to everyone for joining us today. We appreciate your time and participation and your support of AMD. Have a good afternoon.

Operator

[Operator signoff]

Duration: 53 minutes

Call participants:

Laura Graves -- Corporate Vice President, Investor Relations

Lisa Su -- President and Chief Executive Officer

Devinder Kumar -- Executive Vice President, Chief Financial Officer, and Treasurer

Blayne Curtis -- Barclays Investment Bank -- Analyst

Vivek Arya -- Bank of America Merrill Lynch -- Analyst

Matt Ramsay -- Cowen and Company -- Analyst

Toshiya Hari -- Goldman Sachs -- Analyst

Stacy Rasgon -- Sanford C. Bernstein -- Analyst

Joe Moore -- Morgan Stanley -- Analyst

Aaron Rakers -- Wells Fargo Securities -- Analyst

John Pitzer -- Credit Suisse -- Analyst

Chris Caso -- Raymond James -- Analyst

Ross Seymore -- Deutsche Bank -- Analyst

Timothy Arcuri -- UBS -- Analyst