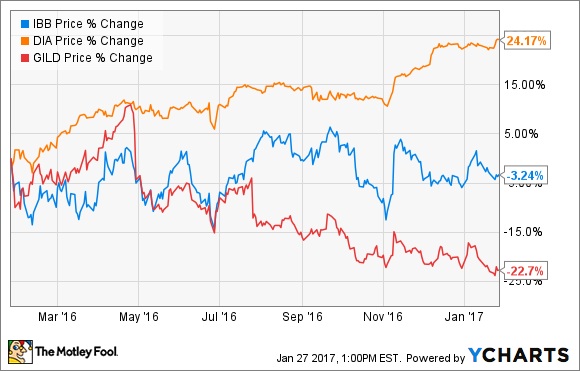

With the Dow Jones Industrial Average blasting through the 20,000 mark, many stocks are currently trading at or near their all-time highs. Unfortunately, biotechnology investors have largely been left out of the rally. The iShares Nasdaq Biotechnology ETF (NASDAQ: IBB) is in the red over the past year, and a few individual companies -- such as Gilead Sciences (GILD -1.25%) -- have performed far worse than that.

Gilead's stock has been in free-fall over concerns that the company's best days are behind it. However, a few Motley Fool healthcare contributors do not agree with that assessment at all. Read on to find out why they plan on hanging on to their shares of Gilead Sciences for the foreseeable future.

Profit lurking in its pipeline

Todd Campbell: I'm not going to sugar-coat it; it's been a horrific year for Gilead Sciences' shareholders. The stock has tumbled in the wake of decelerating hepatitis C sales and trial failures that include the shuttering of trials on its once-promising leukemia drug, Zydelig.

However, investors might not want to focus too much attention on the company's past stumbles, because other drugs are quietly progressing through the company's pipeline that could be multibillion-dollar blockbusters.

Image source: Gilead Sciences.

One of those drugs is filgotinib, an autoimmune disease drug Gilead Sciences is co-developing with Galapagos NV. Filgotinib recently entered phase 3 studies for use in rheumatoid arthritis, Crohn's disease, and ulcerative colitis. A clean safety profile in mid-stage studies and oral dosing could make it a top-seller someday.

Gilead Sciences is also working on therapies for non-alcoholic steatohepatitis, an increasingly common cause of liver transplant. Also, Gilead Sciences is also in the midst of rolling out next-generation HIV drugs that include TAF, a safer formulation of the commonly prescribed Viread. So far, launching drugs that include TAF has been a big success, boosting HIV sales by more than 20% year over year in the third quarter alone.

Admittedly, no one knows if -- or when -- drugs in its pipeline could get commercialized, but with a proven track record, I think Gilead Sciences' pipeline potential is undervalued.

Every metric says that this stock is cheap!

Brian Feroldi: With U.S. stock markets currently trading near their all-times highs, it can be quite shocking to learn just how cheap Gilead's stock has become. Pick any valuation metric you'd like -- trailing PE ratio, forward PE ratio, price to free-cash-flow, price to sales -- and they all show that Gilead is trading at levels it has never seen before.

GILD PE Ratio (TTM) data by YCharts.

I think the most interesting figure on this chart is the company's price to free-cash-flow ratio. Over the past 12 months, Gilead has cranked out more than $17 billion in free cash flow, and yet the company's current market cap is only $94 billion. Those figures suggest that the company could theoretically buy back all of its outstanding shares in less than six years' time! Or, put another way, if Gilead paid out 100% of its free cash flow as a dividend, its yield would be 18%!

If Gilead was in danger of collapsing, these metrics would make sense. However, the company continues to crank out cash flow, invest in its future, and return cash to shareholders through buybacks and dividends. While the company's near-term growth prospects do not look great, this is hardly a company in danger of falling apart.

While I won't advocate that Gilead Sciences is my favorite investing idea at the moment, I do think this company's shares are so cheap that the smart play is to hang on.

Ready to make a deal

Keith Speights: For those who think Gilead's future looks dim, remember that the biotech's stock nearly tripled over the past five years primarily because of an acquisition. Back in November 2011, Gilead bought Pharmasset for $11 billion, picking up the hepatitis C virus (HCV) drug later to be known as Sovaldi. Combinations of Sovaldi with other drugs led to the successful commercial launches of two other HCV drugs, Harvoni and Epclusa.

Gilead has more money -- and more motivation -- to make a game-changing acquisition than it did a little over five years ago. The biotech reported $31.6 billion in cash, cash equivalents, and marketable securities at the end of the third quarter of 2016. With its strong operating cash flow, Gilead undoubtedly has more than that now.

CEO John Milligan has publicly stated that the company is focused on "augmenting [its] portfolio with external opportunities, particularly in the field of oncology." However, Milligan didn't limit Gilead's acquisition prospects to only oncology.

I don't expect the biotech to merely throw money at an acquisition in the hopes that it pays off; Gilead's management team is too disciplined to make a rash decision. However, it won't surprise me if Gilead makes one or more deals in 2017 that pay off for investors over the long run.