Following a $2,000 price bump in November, the price of Tesla's (TSLA +0.22%) Model S is about to go up even further. That's because the company is preparing to discontinue the current entry-level 60 kWh model, including both the single-motor version as well as the dual-motor version that costs an extra $5,000. Tesla has sent out emails notifying customers of the change, and Electrek confirmed the plans with Tesla. The last day that prospective customers can purchase the 60 kWh version will be April 16, 2017.

Tesla says it is making the change because most customers subsequently purchase the upgrade to a 75 kWh battery, which is unlocked via a software update, and the company is streamlining the ordering process. Assuming no other pricing changes, the single motor 75 kWh Model S starts at $74,500.

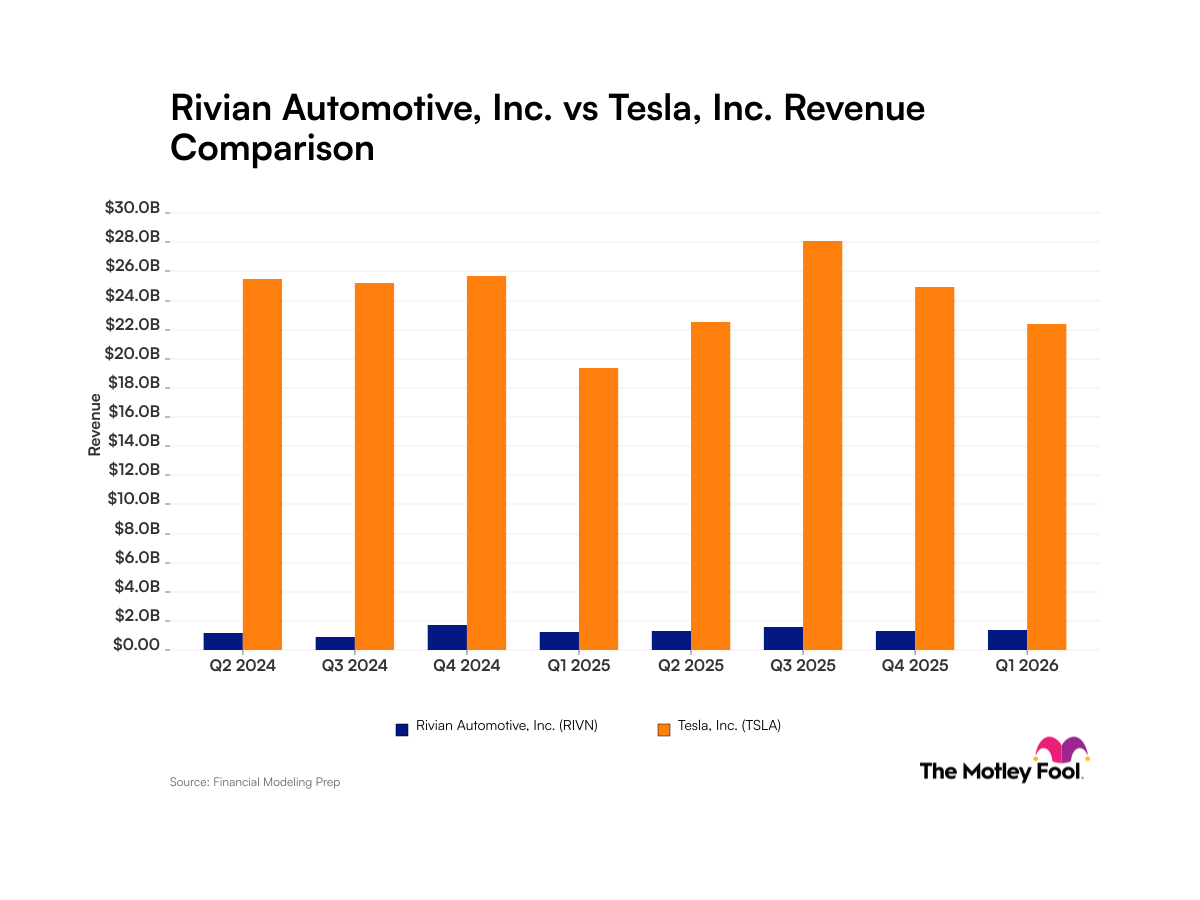

Image source: Tesla.

Following in Model X's footsteps

The discontinuation of the Model S 60 comes shortly after Tesla made similar moves with the Model X last year. The electric-car maker introduced a more affordable 60 kWh version of its Model X SUV (only available in dual motor) in July 2016, which was similarly a 75 kWh battery pack that was software-limited to 60 kwh and started at $74,000. That variant didn't last long, as it was discontinued in October 2016, just four months later. Tesla never provided an official reason. The Model X 75D starts at $88,800.

The software-limited 60 kWh Model S lasted a bit longer, as it was also introduced slightly earlier than the comparable Model X, but it appears to be following in the Model X's footsteps.

Why is Tesla doing this?

The software-limited approach has been controversial from the very beginning. On one hand, there was initial backlash at the idea that customers were being needlessly prohibited from accessing the full battery capacity of a product they had paid for. On the other hand, they paid a lot less for a software limited 60 kWh pack.

From Tesla's perspective, there was a certain amount of risk associated with the approach, since it was still including 75 kWh of capacity, which comes at a cost. The hope was that the lower price point would attract more buyers, who would later upgrade. If the customer is content with 60 kWh and never upgrades, Tesla ends up taking a meaningful hit on margins.

On the earnings call shortly after the software-limited 60 kWh pack was introduced, CEO Elon Musk said that most people that were buying the base 60 were optioning up to where average transaction prices were "over $80,000," while acknowledging lower margins:

Because people are optioning up the 60, it actually ends up being decent. I mean it's not...maybe it is 15% to 20% gross margin whereas say something, like if somebody orders the performance dual motor, that might actually be more like a 30%, 35% gross margin. But there's just a small number of people that want high-performance cars and are willing to pay triple digits, or six digits I should say. But it also remains to be seen how many who order the 60 then choose to do the upgrade to 75 kilowatt hour rate.

There is going to be some number, it's too early to tell, of people who buy it at 60, realize they want the extra range, and then they can just order it kind of like an in-app purchase on the car screen and unlock it. I suspect we will see a pretty decent number of people do that. But we don't, it is still very early, so it's hard to say what number that would be. And if they do do that, then it would push gross margins up into the 20s [percent], like mid-20s [percent] or something.

For reference, Tesla's adjusted automotive gross margin last quarter was 22.2%, which was down sequentially due to delayed Autopilot-related software updates; the company said it recognized "almost no new Autopilot-related revenue" during the quarter.

Tesla's justification that the move is meant to streamline ordering doesn't pass the sniff test. More than likely, the S 60 is being discontinued for financial reasons, if the upgrade rate is lower than Tesla had previously anticipated. A large concentration of non-upgraded 60s with a 15% to 20% gross margin could put pressure on profitability, while discontinuing the option pushes the margin on those vehicles to the 20% to 25% range with the potential downside of losing some customers who aren't willing to pay more.

Hopefully, the margin upside offsets any lost sales.