Shares of electric-car pioneer Tesla (TSLA +0.76%) have rocketed higher by 65% since the beginning of December, after two and a half years of up-and-down performance. This big jump reflects growing anticipation for Tesla's upcoming Model 3 sedan, continued strong sales for its pricey Model S and Model X vehicles, and improving investor confidence regarding Tesla's other green energy ventures.

Tesla's huge rally has boosted its market cap to about $49 billion, even though the company is still unprofitable. That figure puts it ahead of No. 2 U.S. automaker Ford Motor. Tesla is now closing in on industry leader General Motors' (GM +0.52%) $51 billion market cap.

Tesla stock price and market cap growth; data by YCharts.

Barring a huge setback, Tesla is almost certain to surpass GM's market cap eventually, and it will probably be soon. Nevertheless, General Motors is a better bet for investors -- even those with a long-term mindset.

Tesla has been on a roll

There's no doubt that Tesla has been firing on all cylinders in the past few months. In the company's most recent earnings report, Tesla revealed that orders for the Model S and Model X combined were up 49% year over year in Q4. It also confirmed that it is on track to begin limited production of the new Model 3 in July.

Tesla reported more good news last week, announcing that it built 25,418 vehicles during the first quarter and delivered just over 25,000. That was important, because while Tesla has never had trouble selling cars, production snafus have been a recurring problem.

If Tesla is finally ironing out its operations, that's a very good sign for shareholders. CEO Elon Musk envisions building 1 million vehicles annually within a few years, way above the record of 76,230 deliveries reached last year. Achieving that goal (or even getting close) will require Tesla to master the complexities of mass production.

Tesla is gearing up to start production of the Model 3 sedan. Image source: Tesla.

But cash flow matters -- a lot

Notwithstanding Tesla's strong growth trajectory, the company is still losing money and burning cash at a rapid rate. Tesla has had to raise capital repeatedly in the past few years by selling more shares and raising debt (mainly convertible notes).

By contrast, General Motors has become extremely profitable. In 2016, it generated a record adjusted operating profit of $12.5 billion and adjusted automotive free cash flow of $6.9 billion. While investors seem to be very worried that U.S. auto sales have peaked, GM's management has said the company will produce EPS of $6.00-$6.50 this year, in line with or slightly higher than last year's record mark of $6.12.

General Motors' strong earnings and cash flow have allowed the company to start returning lots of cash to investors. GM stock has a strong dividend yield above 4%. Furthermore, the company has spent more than $6 billion on share buybacks over the past two years and plans to repurchase another $5 billion of stock in 2017.

GM's cash flow trajectory may be bumpy going forward, but it is well positioned to increase its free cash flow over the next five to 10 years. First, the company's decision to jettison its money-losing European operations will improve its annual free cash flow by about $1 billion.

GM's decision to sell its Opel/Vauxhall division will boost its free cash flow. Image source: General Motors.

Second, General Motors is in the early stages of a long-term plan to move all of its vehicles to as few as four major platforms (or "vehicle sets") to reduce costs. If this effort succeeds, it could reduce GM's annual capex requirements further, boosting free cash flow. That situation would allow it to return even more cash to shareholders.

Focus on total return, not market cap

Many investors seemingly fail to appreciate the fact that GM is returning more and more cash to shareholders, while Tesla is steadily issuing more shares to fund its growth.

There's nothing wrong with either capital allocation strategy, per se. General Motors is a mature company, so it's appropriate for it to focus on generating free cash flow and returning most of that cash to shareholders. By contrast, Tesla is still in the early innings of its growth, so it's quite sensible for the company to be investing heavily to drive future growth.

However, this distinction means that investors shouldn't be comparing changes in the two companies' market caps. Instead, they should be focusing on GM and Tesla shares' total return, including dividends.

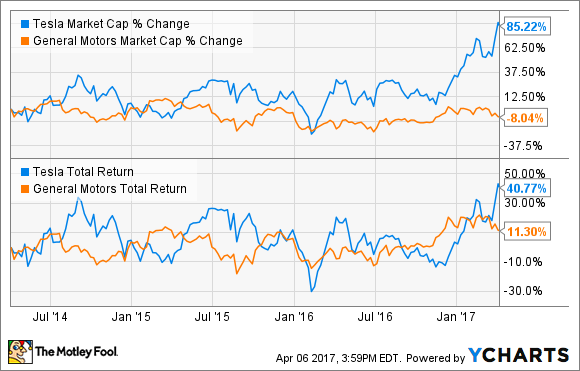

Thanks to its frequent share issuances, Tesla's market cap has nearly doubled in the past three years, while GM's market cap has declined. But on a total return basis, Tesla's lead over GM is much smaller -- and it was trailing by a significant margin just a few months ago.

Tesla vs. General Motors market cap and total return performance; data by YCharts.

General Motors stock currently trades at a depressed price because investors are extremely pessimistic about its long-term prospects. Conversely, Tesla stock has a lofty valuation because of investors' optimism about its growth trajectory.

However, in the very long run, free cash flow drives share price performance. Every year General Motors generates strong free cash flow and returns it to shareholders, existing GM shareholders will get a bigger proportional stake in this cash machine. Every year Tesla issues more shares, investors see their stake in the company's future profits decrease.

This gives GM a huge advantage over Tesla in the long run from an investing standpoint. If the company's initiatives to become more efficient and increase its cash flow are even halfway effective, General Motors stock is likely to deliver bigger gains for investors than Tesla stock over the next five to 10 years.