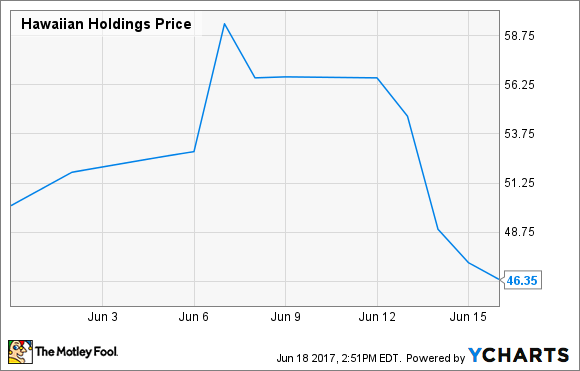

Less than two weeks ago, Hawaiian Airlines was on top of the world. Shares of Hawaiian Holdings (HA +0.00%) -- the airline's parent company -- soared 12% on June 7, ending the day at $59.35, just shy of the stock's all-time high.

It's been all downhill from there, though. Hawaiian Holdings stock fell every single day last week, including a 10.5% tumble on Wednesday, ending the week at $46.35. The stock is now down a whopping 22% from its June 7 peak.

The stock's plunge has been driven almost entirely by the news that United Continental (UAL +1.04%) plans to significantly increase service to Hawaii beginning in December. Yet investors have dramatically overreacted to this news. As a result, Hawaiian Holdings stock once again looks like an extremely appealing investment opportunity.

2017 will be a phenomenal year

Hawaiian Airlines entered 2017 with the most unit revenue momentum of any U.S. airline, and it has continued to thrive in the first half of the year. Revenue per available seat mile (RASM) soared 7.6% year over year last quarter. The carrier also raised its second-quarter revenue guidance recently. It now expects RASM to rise 7.5%-10.5% this quarter.

Unit revenue is soaring at Hawaiian Airlines. Image source: Hawaiian Airlines.

Year-over-year unit revenue comparisons will be tougher in the second half of the year, but Hawaiian Airlines is well positioned to continue posting strong RASM results for the rest of 2017 for several reasons.

First, demand growth will probably continue to outpace supply in the key West Coast-Hawaii market. Second, RASM has finally started to rebound on international routes, due to the stabilization of foreign currencies like the yen and the Australian dollar against the U.S. dollar.

Third -- and most importantly -- Hawaiian Airlines has made significant progress on its aircraft retrofit program in the first half of 2017. This has allowed it to deploy lie-flat premium cabin seats and an increased number of extra-legroom economy seats on additional routes. Other than its interisland flights, Hawaiian Airlines exclusively flies long-distance routes for which many customers are willing to pay a premium for more space.

Hawaiian does face significant cost pressure this year. For the full year, management expects a mid-single-digit increase in non-fuel unit costs. That said, the company will face less non-fuel unit cost pressure in the second half of the year than it has experienced year to date. Moreover, the price of jet fuel recently fell to its lowest level of the year. As a result, fuel cost inflation is on pace to become negligible in the second half of 2017.

2018 should be strong, too -- but for other reasons

Given that Hawaiian Holdings stock has plunged 22% in the span of seven days, it appears that investors are panicking about United's recently announced plan to add flights to Hawaii.

Hawaiian Holdings Stock June Performance. Data by YCharts.

But while United Continental will add flights on 11 routes to Hawaii starting in December, Hawaiian only competes on four of those routes today. The vast majority of Hawaiian's West Coast-Hawaii routes won't be getting extra nonstop competition.

That said, other carriers may add flights to Hawaii for 2018, matching United's capacity increases. Additionally, Hawaiian Airlines will face very challenging year-over-year RASM comparisons, at least in the first half of 2018. As a result, the carrier may be unable to post strong RASM growth again next year, even though it will continue to benefit from its ongoing aircraft retrofit program throughout the year.

But on the plus side, Hawaiian's unit cost performance should be much better next year. The carrier is absorbing significant one-time cost increases in 2017, mainly related to pilot wage increases and the upcoming introduction of its new A321neo fleet.

By contrast, in 2018, Hawaiian Airlines will start to benefit from adding the A321neo to its fleet. The A321neo will have lower unit costs than the aging 767s it is replacing, including much better fuel efficiency. Barring another spike in jet fuel prices, Hawaiian Airlines would probably be able to post earnings-per-share growth next year even with a flat RASM performance.

Hawaiian Holdings stock is extremely cheap

After its recent plunge, Hawaiian Holdings stock trades for just 8.4 times the average analyst earnings estimate for 2017. Furthermore, analysts' EPS estimates could be much too low, in light of Hawaiian's strong unit revenue trajectory and the recent decline in fuel prices.

Wall Street analysts currently expect EPS to decline modestly at Hawaiian Airlines next year. However, the analysts have consistently underestimated this little airline recently. In the past two months, the average EPS estimate for 2017 has increased by a stunning 15% as the company's performance has soared past expectations.

It looks like analysts may be underestimating Hawaiian Airlines again. If that's true, then Hawaiian Holdings stock has huge upside over the next few years.