Vacation travel specialist TripAdvisor (TRIP +4.23%) is set to announce second-quarter earnings results before the market opens on Wednesday, August 9. The stock is limping into this week's report, down sharply so far in 2017.

Below, we'll look at the key trends investors will be watching that might deepen that slump -- or flip the trajectory into a positive one.

Image source: Getty Images.

Hotel shopping rebound

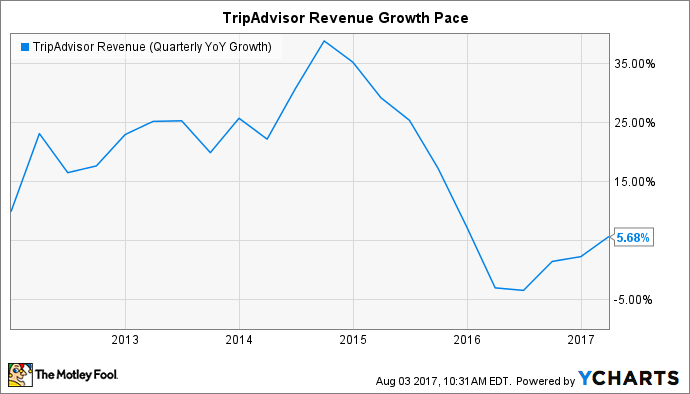

TripAdvisor posted an encouraging growth uptick last quarter as revenue gains improved to a 6% pace from the 1% drop the company posted for the full 2016 fiscal year. The key contributor to the turnaround was a rebound in its hotel segment, which benefited from a 12% spike in click-based and transaction revenue compared to no growth in the year-ago period.

That segment has been pushed lower by TripAdvisor's new instant booking functionality that traded an improved shopping experience for lower direct revenue. But now that a full year has passed since instant booking was rolled out, the company faces easier growth comparisons going forward. In fact, the pace of gains in revenue per shopper has now improved for four straight quarters. After setting a low in the first quarter of 2016 at a brutal negative 21%, the hotel shopper spending growth hit a two-year high of 2% last quarter.

TRIP Revenue (Quarterly YoY Growth) data by YCharts.

That's ideally just the start, though. TripAdvisor is expecting to build on that modest rebound this quarter -- and through the year -- with help from increased hotel room supply, upgrades to the shopping experience, and a new TV advertising campaign.

Non-hotel growth

TripAdvisor has done a good job over the past few years in growing its non-hotel segment into a significant part of the business. These products include attractions, restaurants, and vacation rentals, and as a group, they hit 20% of sales in 2016 compared to 9% two years earlier.

It was easily TripAdvisor's fastest-growing niche to start fiscal 2017, too. In fact, non-hotel revenue spiked 18% last quarter to $58 million. The gains were powered by a 40% surge in the supply of bookable attractions and by a 20% spike in restaurant reservation supply. In addition to continued progress on the revenue side, investors will be looking for this division to finally begin contributing to profit growth. 2017 marks the end of a planned three-year investment phase in the segment, so TripAdvisor is targeting positively adjusted profits for the full year.

A refreshed outlook

Management's latest annual operating outlook paired modest growth expectations with almost zero earnings improvement. The company warned investors back in May that it will allocate a big chunk of excess cash toward a brand-building advertising campaign.

CEO Stephen Kaufer and his executive team believe the marketing spending will support double-digit sales growth overall and a double-digit gain in click-based and transaction revenue on hotel bookings. The non-hotel division should also show material profits for the first time this year.

Over the longer term, look for the instant booking business to achieve rising profitability so that the company can build on the $350 million in adjusted earnings it logged last year. Yet for the stock to shake off its recent funk, TripAdvisor will also need to show a sustained improvement in its sales growth pace. Such a boost would point to market share gains in the massive -- but highly competitive -- online travel industry.