Costco (COST +0.23%) stock recently dipped into negative territory for the year to put it well behind the broader market's 10% increase. At first blush, the sell-off looks like shortsightedness on the part of investors. After all, sales growth is ticking up even as the retailer introduces its plans for higher membership prices.

Long-term shareholders shouldn't be rattled by a little volatility. However, with Costco shares barely keeping pace with the market over the last five years, it's worth looking at the prospect for a continuing disappointing stretch for the business.

Image source: Getty Images.

Growth hits a wall

Sales growth is speeding up lately, with comparable-store sales improving to a 5.9% pace in August from 5.3% in the prior month. That's an encouraging sign for the business, especially as many retailers are enduring flat or slightly negative comps lately. Rival Kroger (KR +0.83%), for example, just saw its comps drop into negative territory after 12 consecutive years of increases.

Costco's longer-term results show that it isn't immune to the competitive pressures hitting Kroger and its other retailing peers. The warehouse giant's comps gains hit a six-year low of 4% in fiscal 2016. They're running at about the same sluggish rate over the past 12 months, too.

Comps excluding fuel sales and currency exchange shifts. Data source: Costco. Chart by author.

Part of the reason why investors assign such a premium to Costco's stock is that the company consistently outgrows its rivals. If that gap shrinks -- or disappears -- it makes sense that the shares would command a lower valuation going forward.

Peer pressure

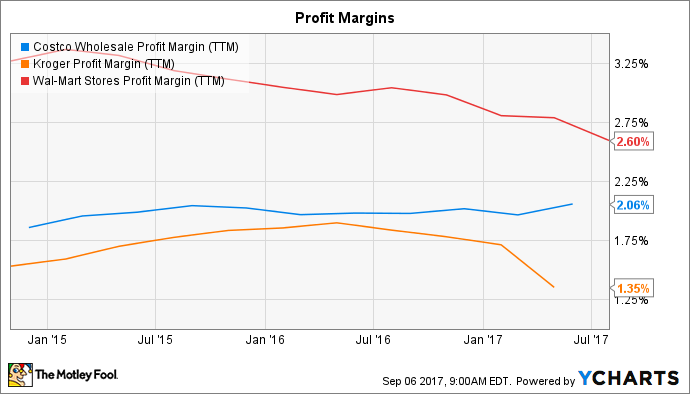

Many of Costco's key rivals are warning investors to brace for declining profits. Wal-Mart (WMT -0.44%) has seen its operating income slump as it pours resources into increasing its wages and spending on employee training and education. Kroger lowered its full-year earnings outlook as management promised to meet market-share competition with more cost cuts. "Kroger has invested more than 3.8 billion to lower prices for our customers" in the last 15 years, CEO Rodney McMullen said. "We have no intention of giving up the momentum we've gained on low prices," he added.

COST Profit Margin (TTM) data by YCharts.

Costco already invests heavily in its employees, and its above-average pay ensures some of the lowest turnover in the industry. The retailer's price-leadership strategy also leaves it well protected against peers aiming to sacrifice profits to steal market share.

Still, these moves are likely to add pressure on Costco to invest more in retaining employees and in attracting customers through low prices. That could translate into reduced earning power over time.

Looking ahead

Costco's short-term profit outlook is positive, given that its membership fee increase will start lifting bottom-line results in fiscal 2018. Most of the retailer's earnings come from these annual club membership costs. And, even as comps can swing from year to year, the fees tend to climb steadily as more members get added to the pool. Subscriber income reached $2.6 billion last year, up from about $1.6 billion in 2010.

Costco's growth plans include aggressively expanding is store base, especially in international markets. Its loyalty card switchover, meanwhile, appears to be delivering big gains to members and to the business, which implies increased customer satisfaction.

As a result, while I'll be watching comps and profit trends, I wouldn't start worrying about my Costco investment unless the company starts losing ground with its members. The good news is subscriber renewal rates are above 90% and holding steady right now.

I'd expect that rate to tick higher as the company recovers from the negative impact of last year's credit card switchover. And, as Costco has demonstrated in the past, a big base of happily renewing customers forms the foundation for market-beating sales and profit growth.