Wheaton Precious Metals (NYSE: WPM) and Franco-Nevada Corp (FNV +1.89%) are both great ways to get exposure to silver and gold. While their basic business models are similar, there are some important differences between the two companies. My pick of the pair is Franco-Nevada. Here's why.

The streaming model

Wheaton and Franco-Nevada are both streaming companies. That means they provide miners cash upfront for the right to buy gold and silver at reduced rates in the future. This allows the companies to avoid the headache and risk of actually running mines. It also locks in low prices and wide margins. To put a number on that, Wheaton's average price for gold is around $400 an ounce and its average price for silver is around $4 an ounce (both are materially lower than spot prices for those metals today).

Image source: Getty Images.

So, at their core, these two companies have roughly similar business models. But where each company has chosen to go from here is a little different.

Three is the charm

The first big difference is size, something that actually comes in two flavors. Wheaton is an $8.5 billion market cap company. Franco-Nevada is much larger at nearly $15 billion. Wheaton's business, meanwhile, is backed by a smaller number of larger deals, with a portfolio of 29 projects, 21 of which are currently operating and eight that are in some phase of development. Larger Franco-Nevada has 46 producing mines, 41 development projects, and 172 exploration investments.

As you might expect based on its size, Franco-Nevada is a more diversified company. However, it's important to note that it has a lot more development-stage projects in the pipeline. It has, basically, spread its bets out. Smaller Wheaton Precious Metals is more selective and focused. Neither one is the inherently better choice, but I tend to err on the side of diversification.

How streaming works, according to Wheaton. Image source: Wheaton Precous Metals.

When looking at diversification, however, you also need to step back from precious metals. The second key difference here is that, in addition to precious metals, Franco-Nevada also has 80 investments in oil and gas projects. These investments only accounted for about 6% of revenue in the second quarter and are unlikely ever to become the company's main focus. But management has used the energy downturn that started in mid-2014 to opportunistically diversify into the oil and gas business.

Franco-Nevada is using a similar mode of providing energy companies financing, so it hasn't become an oil and gas driller. But it is not a pure metals play. That may sway you toward Wheaton. However, I find this to be an appealing attribute because it shows that management is willing to take advantage of opportunities if it sees them while continuing to stick close to the core streaming business model. More diversification is a good thing in my eyes.

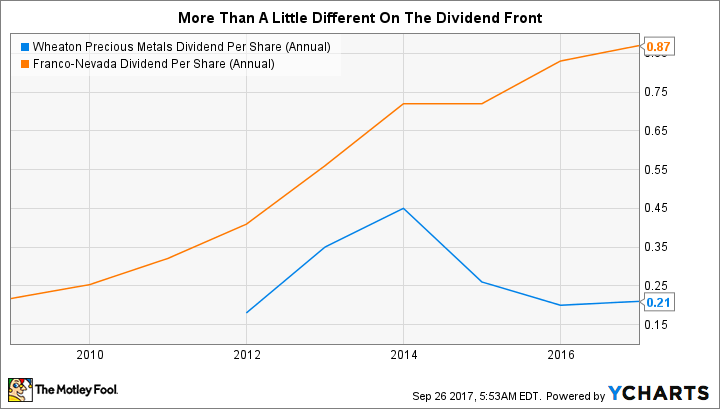

The last big difference is dividend policy. I prefer Franco-Nevada's approach of a steadily increasing distribution. Including 2017, the company has increased its dividend every year for a decade. Wheaton's dividend is tied to the company's performance. Wheaton's approach has merit in that the dividend will increase when gold and silver are doing well, which will often be at times of broader market weakness.

WPM Dividend Per Share (Annual) data by YCharts.

Taking that to the next step, if you want to own precious metals for diversification, Wheaton's dividend could add a little dividend diversification to your portfolio. Effectively, right when other companies in your portfolio are likely to be struggling (which could conceivably include dividend cuts), Wheaton will be rewarding you with dividend increases as investor seek out safe haven assets like gold and silver. I prefer slow and steady hikes, but I can see where Wheaton's approach has value.

Why Franco wins the day

When I put it all together, I'm a fan of Franco-Nevada. It is larger, more diversified, willing to be opportunistic, and has a history of rewarding investors with a steadily increasing dividend. That doesn't mean that Wheaton is a bad company. In fact, it's a great way to gain precious metals exposure as long as you recognize that it has a focused portfolio, sticks closely to its precious metals approach, and has a variable dividend policy. None of that is bad, but in my opinion Franco-Nevada's still got the edge.