The consumer products industry is still trying to break out of its global funk. Unilever (UL +0.33%) this week announced flat sales volume as the company faced pressure from rivals and major weather disruptions in key markets. Still, Unilever's management team kept its full-year outlook in place and said they were encouraged to see early signs of a rebound in several geographies.

Let's take a closer look at the results.

Image source: Getty Images.

What happened this quarter?

Organic sales growth was surprisingly weak as big gains in emerging markets were tempered by declines in the U.S. and Europe. Unilever gave up some market share this quarter, particularly in its European ice cream business. But the bigger factor was a sales disruption caused by hurricanes that hit the Caribbean and the key U.S. markets of Texas and Florida.

Highlights of the quarter include:

- Unilever's 2.6% organic growth pace marked a step down from the prior quarter's 3% gain. That growth once again depended entirely on price increases as sales volumes stayed flat.

- Each of the company's four divisions expanded, with the refreshment segment posting the best results thanks partly to innovation in the Ben & Jerry's and Magnum ice cream brands offsetting weakness in ice cream sales due to weather and competition. The personal care division, anchored by the Dove and Signal franchises, managed the smallest gains.

- By geography, Unilever grew organic sales by 6% in the Asia segment and by 6.6% in Latin America. China and India stood out as particularly strong growers. Yet those emerging market gains were mostly offset by declines in the U.S. and Europe.

What management had to say

CEO Paul Polman focused his comments on broader trends. "While conditions in our developed markets remain challenging," he said in a press release, "we are starting to see signs of improvement in some of our biggest emerging markets including India and China."

Executives are encouraged by the results out of their cost-cutting efforts, too. This initiative is running ahead of their targets, in fact, which is adding flexibility for extra investment in growth areas like advertising and marketing. "The new organization is delivering increased innovation speed and our savings programs are allowing us to step up investment behind new growth opportunities. We expect to reap the benefits over the coming quarters," Polman explained.

Looking forward

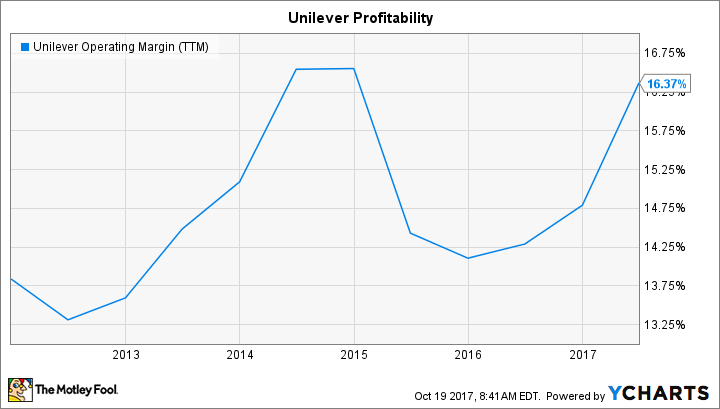

Executives affirmed their full-year outlook that predicts organic growth of between 3% and 5%. They still believe operating margin will improve by about a full percentage point, too, on its way to reaching 20% of sales by 2020.

UL Operating Margin (TTM) data by YCharts

That growth forecast implies that the company will expand sales at a pace that isn't much stronger than that of the overall industry this year. Executives aren't happy with that level of performance, which is why their focus is on speeding up organic sales so that Unilever is gaining market share again.

Management plans to get to that result through a mix of innovative product launches, portfolio shifts toward high-growth areas, and major brand acquisitions. These moves should lift results over the next few quarters, they say.

At the same time, it will be interesting to see whether developed markets like the U.S. and Europe continue to drag global results lower, or if they finally begin strengthening again to add momentum to the rebound that's happening in emerging markets.