Over the last few years copper and gold miner Freeport-McMoRan Inc. (FCX -1.42%) has faced headwinds ranging from bad investment choices to commodity price weakness to complicated relationships with foreign governments. It's been a hard stretch to say the least. On the other hand, Wheaton Precious Metals' (NYSE: WPM) biggest shift recently may have been changing its name to better reflect the breadth of its portfolio. Here's why Freeport's troubles show why Wheaton is the better buy.

Oh what a tangled web

The current chapter in Freeport's story starts with the commodity downturn that began in 2011. There's not a whole lot a miner can do about this issue, but the impact is pretty notable. The company's earnings peaked in 2011 at nearly $4.80 a share, then declined in each of the next four years, at which point the company was deep in the red. The only thing Freeport could do about it was focus on reducing costs by trimming operating expenses and capital investment plans.

Image source: Getty Images

Freeport, however, also made an investment decision that proved, in hindsight, to be a disaster. In 2013 Freeport completed a deal to buy two oil and natural gas drillers that increased its long-term debt obligations from $3.5 billion at the start of that year to $20.4 billion by the end of it. When oil prices started to tank in mid-2014 this diversification move turned into an albatross. Although Freeport had largely extracted itself from the oil business by 2017, its debt levels remain elevated at $12.5 billion at the end of the third quarter -- a nasty leftover from an ill-timed investment.

Freeport's core mines. Image source: Freeport-McMoRan

And then there's the trouble Freeport is currently facing with its Grasberg mine in Indonesia. This single asset accounts for around 30% of the miner's copper reserves and nearly all of its gold reserves. It's currently in a dispute with the Indonesian government about the ownership of the mine. They have a general framework for a solution, but they are still hammering out the fine details. Something will likely be worked out eventually, but the process hasn't been smooth and has cast a pall over Freeport's future.

A different way to do things

I don't want to suggest that Freeport is somehow a bad company, but it certainly isn't appropriate for most investors right now. All of the issues it's faced, however, help explain why Wheaton Precious Metals is a better choice in the metals space.

Wheaton isn't actually a miner, it's a streaming company. That means it gives miners cash up front for the right to buy silver and gold at reduced prices in the future. This model locks in low prices and, more importantly, wide margins -- for example, Wheaton's price for silver is around $4 an ounce. For gold it's $400 an ounce.

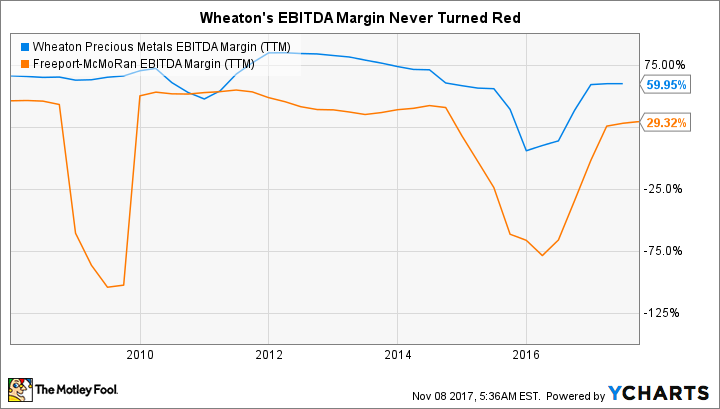

Even during the commodity downturn, when other miners saw their EBITDA margins dip deep into the red, Wheaton's margins were still soundly in positive territory. It can't escape the impact of low silver and gold prices, but it has a wider buffer because it doesn't have to deal with running mines -- it just collects its precious metals at contractually low prices after all the work has been done.

WPM EBITDA Margin (TTM) data by YCharts

In fact, the commodity downturn was an opportunity for Wheaton to ink new streaming deals. For example, in 2015 it provided financially struggling miners Vale and Glencore with cash to shore up their balance sheets. Those deals helped lead to record sales volumes in 2016. In other words, downturns can actually be opportunities for Wheaton to expand while miners like Freeport are retrenching.

But even Wheaton makes mistakes. For example, it invested in Pascua-Lama, a mine project that has struggled to get off the ground. The mine's owner, Barrick Gold (ABX -0.12%), has had to deal with legal, government, environmental, and commodity price issues. Barrick has to shoulder all of the costs and time associated with the mine, however, while Wheaton's cost for the project is capped by its up-front investment. There's a time value of money issue, but no ongoing expenses.

This single investment, meanwhile, is just one of the 20 operating mines and eight development projects in which Wheaton has invested. It will be unfortunate if it doesn't work out, but certainly not the end of the world. Most miners don't have that level of diversification -- Freeport, for reference, only has 10 mines, half as many as Wheaton.

Go with Wheaton

There's been a lot going on at Wheaton in recent years, but nothing that has derailed, altered, or imperilled its basic business model. Which is why Wheaton's recent name change from Silver Wheaton to Wheaton Precious Metals (to highlight the increasing role of gold and other metals in its portfolio) is probably the most notable change at this streaming company. The steady, boring nature of streaming is really highlighted when you compare Wheaton with the troubles at Freeport. Most investors will be better off avoiding the mining side of the business and sticking with a streamer like Wheaton.