If you're retired, or getting close, you shouldn't avoid stocks completely. Yes, any investments you'll need to sell for income in the next few years should be held in less-volatile holdings like bonds, or kept in cash. But with the average retiree living into their 80s now, you still need to think long term. And stocks continue to be one of the very best long-term generators of wealth for the average person.

But that doesn't mean you need to make risky bets to capture solid returns, either, and buying solid companies at reasonable prices can help create a margin of safety and improve your returns, while also decreasing your risk of permanent losses. Three stocks that meet these criteria are small healthcare real-estate specialist Caretrust REIT Inc (CTRE +2.17%), financial services giant Prudential Financial Inc (PRU +0.69%), and energy behemoth ExxonMobil Corporation (XOM +0.97%).

Image source: Getty Images.

These aren't just random ideas, either: Three Motley Fool Investors have identified these particular companies as value stocks perfect for retirement. Why? I'll give you a few hints. All three have strong, profitable businesses, boast solid dividend histories, and trade for a discount to their historical valuations. But that's just the tip of the iceberg. Keep reading for more.

A contrarian value play on a trend retirees are driving

Jason Hall (Caretrust REIT): Recently, investors have eschewed real estate investment trusts -- or REITs -- as interest rates have begun climbing. On the surface, this makes sense, as most REITs rely heavily on debt to fund acquisitions of their properties, and rising rates will increase their expenses and cut into their returns. The irony here is that, historically, REITs haven't done badly when interest rates have increased. Rising rates generally correspond to a healthy economy, which drives earnings growth that outpaces higher rates. One REIT I particularly like is Caretrust REIT, which has seen its share price fall sharply during the REIT exodus.

Caretrust is a great value today, trading for less than 11 times company guidance for 2018 funds from operations, and with a big trend making it an excellent long-term investment: baby boomers retiring in huge numbers in the coming decades.

By 2029, there will be nearly 80 million Americans age 65 or over, with nearly half over 80. This is almost double 2015 levels, and it's going to require a substantial increase in healthcare, skilled nursing, and independent living properties to meet the healthcare and housing needs of this burgeoning population. With fewer than 200 total properties today, Caretrust is well-positioned to grow from both consolidation and industry expansion over the next decade-plus.

In addition to its reasonable valuation and solid long-term prospects, Caretrust also pays a substantial dividend, yielding over 6% at recent prices and with a history of regular increases.

A rock solid business at a dirt cheap price

Chuck Saletta (Prudential Financial): Prudential Financial is a company that's so interested in being considered "rock solid" that it uses an actual rock -- the Rock of Gibraltar -- as its corporate symbol. It has done so since 1896, and that gives it more than 120 years of living up to that promise. In fact, it was one of only a handful of financial giants that was able to not seek out TARP funds in the wake of the latest financial crisis.

For a company in the insurance business like Prudential Financial is, financial strength is critical for the business's long-term survival. Clients are only willing to pay for insurance if they truly believe the insurance will be there for them when they need the coverage. Prudential Financial achieves its strength though a balance sheet that has more cash and short-term investments than debt, giving it the ability to weather tough financial storms.

Its staying power and financial strength make it a great company, but what makes it a value stock perfect for consideration in your retirement is the market's current price for its business. Prudential Financial can be purchased today for around 0.8 times its book value and less than nine times its expected forward earnings. For a company that's expected to be able to increase its earnings by around 11% annualized over the next five or so years, that's a dirt-cheap price to pay if those earnings occur.

In addition, Prudential has regularly increased its dividend over the past decade, and its current yield of just over 3.4% has been achieved despite paying out less than 20% of its earnings as dividends. So even if its stock doesn't light the world on fire, retirees can anticipate a decent income from that dividend, courtesy of buying its rock-solid business at a relatively low price.

Don't count this giant out

Reuben Gregg Brewer (ExxonMobil Corporation): ExxonMobil is one of the world's largest integrated oil and natural gas companies. Its diversified business spans from drilling (upstream) to processing and delivering refined products (downstream). This provides balance, since the downstream tends to benefit when low oil prices are crimping results in the upstream segment. That's the kind of business diversification retired investors should like.

But that's not unique in the energy space. What is unique is that Exxon pairs this diversified portfolio with industry-leading leverage metrics. Its financial debt-to-equity ratio is a modest 0.12 times, easily lower than its closest peers. Debt to EBITDA of roughly 1.1 times is also far below its major competitors. Exxon is not a company you have to worry about very much.

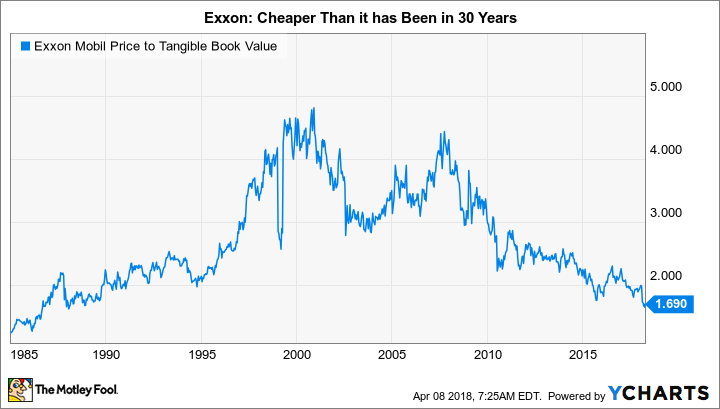

XOM Price to Tangible Book Value data by YCharts.

And it's cheap today. In fact, its price to tangible book value hasn't been this low since the late 1980s. There are some reasons investors are downbeat on Exxon's shares, like falling production and peers catching up to its typically industry-leading return on capital employed metrics, but management has plans to improve results. Only with a giant, conservative business, it may take a couple of years for Exxon to move the needle. In the meantime, value investors can buy on the cheap and collect an over 4% yield why they wait for better days. The dividend, by the way, has been increased an incredible 35 years in a row.