What a difference a year can make.

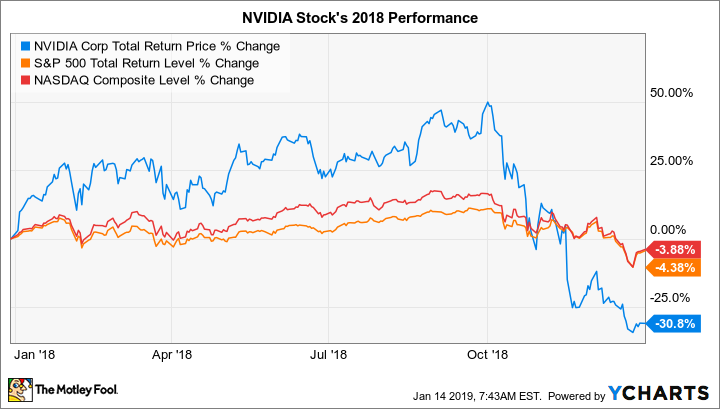

In one year, NVIDIA (NVDA +3.47%) stock went from being belle of the stock market ball to something akin to an evil witch casting spells on investors' portfolios. After returning 227% and 82% in 2016 and 2017, respectively, shares of the graphics processing unit (GPU) specialist declined 30.8% (including dividends) in 2018.

For context, the S&P 500 declined 4.4% (including dividends), while shares of NVIDIA's discrete GPU archrival Advanced Micro Devices gained 79.6% last year.

As for 2019, NVIDIA stock has returned 11.5%, through Friday, Jan. 11, when it closed at $148.83. That's much better than the S&P 500's 3.6% return, but it's still 49% off NVIDIA stock's all-time closing high of $289.07, set on Oct. 1, 2018.

Here's what investors should know.

Image source: Getty Images.

Before we dig into what went wrong for NVIDIA in 2018, let's consider the bigger picture. Despite getting pummeled last year, NVIDIA stock is still a massive winner -- it's returned 410% over the three-year period through Jan. 11. While this is little consolation for folks who bought near or at the stock's high, it's something for long-term-focused investors to keep in mind.

Data by YCharts.

Thanks to its powerful 2018 showing, AMD stock has performed better than NVIDIA stock over the three-year period -- it's gained a whopping 766%. However, NVIDIA remains the champ over longer periods. Over the five-year period, for instance, shares of NVIDIA returned 895%, versus AMD's 386% rise.

NVIDIA stock's poor 2018 performance: Two main catalysts

Shares of NVIDIA were flying high last year until October, as the chart below shows. We can attribute the stock's poor performance in 2018 largely to the following two factors, the second of which is company-specific and has two components:

- The major market sell-off in October that hit highly valued tech stocks particularly hard. Concerns about rising interest rates, a slowing global economy -- and particularly slowing demand for semiconductors -- and the escalating trade war with China were likely the main reasons for the market jitters. NVIDIA stock declined 25% in October.

- NVIDIA's release of third-quarter results along with fourth-quarter guidance on Nov. 15 that disappointed the market. The culprit: the "cryptocurrency hangover," to use NVIDIA CEO Jensen Huang's words.

Data by YCharts.

In the third quarter, NVIDIA's revenue grew 21% year over year, earnings per share jumped 48%, and EPS adjusted for one-time factors rose 38%. While these results are good, they represent a slowdown from the company's recent quarterly results. Moreover, both revenue and adjusted EPS fell short of Wall Street's expectations, while revenue failed to meet NVIDIA's own guidance.

Additionally, NVIDIA's fourth-quarter revenue guidance came in significantly lower than Wall Street was expecting. The company expects revenue of $2.70 billion, representing a decline of about 7% year over year. Wall Street was projecting $3.4 billion in revenue. The market is forward-looking, so we can probably attribute the pummeling of NVIDIA stock after its earnings release more to the fourth-quarter guidance than the third-quarter results.

The reason for the weak outlook is management's expectation that the "crypto hangover" will continue for another quarter or two. This term refers to the excess inventory of midrange Pascal GPU-based graphics cards in the sales channel due to the cryptocurrency market bust that occurred in early 2018. Some cryptocurrency "miners" had been using NVIDIA's gaming graphics cards, rather than its application-specific boards, for mining digital currencies.

What's an investor to do?

Certainly, investors should not bail on NVIDIA stock. As I wrote after the company released third-quarter earnings:

Nothing has changed with respect to the gaming market's rosy long-term growth projections or NVIDIA's position as the dominant supplier of graphics cards to gamers. Moreover, the company's growth opportunities from AI [artificial intelligence] and driverless vehicles remain powerful.

As for AI, NVIDIA's GPUs are the chip of choice for training AI systems.

Investors who have been eyeing NVIDIA for some time might want to start nibbling on the stock. Shares are more reasonably valued than they've been in several years. They're trading at 20.8 times the company's expected forward earnings -- quite reasonable for the stock of a high-quality company that Wall Street expects to grow earnings at an average annual rate of 15.1% over the next five years. Moreover, shares could be even more reasonably priced than they appear. That's because the Street's long-term earnings growth estimate could prove too conservative, as NVIDIA routinely beats Wall Street's expectations.

Check out the latest NVIDIA earnings call transcript.