Medical device makers were some of the best-performing companies on the market last year. In this week's episode of Industry Focus: Healthcare, host Shannon Jones and Motley Fool contributor Brian Feroldi talk about three medical device monopolies that investors might want to take a closer look at. Listen and find out what makes Intuitive Surgical (ISRG +5.72%), Abiomed (ABMD +0.00%), and NovoCure (NVCR +9.00%) stand out from the crowd, dominate their niches, and improve patient lives. Plus, learn the key metrics investors should watch, what long-term risks to be aware of, which of the companies faces the most competitive risk, some of the most exciting opportunities still ahead, and more.

Check out the latest earnings call transcript for Intuitive Surgical, Abiomed, and NovoCure.

A full transcript follows the video.

This video was recorded on Feb. 20, 2019.

Shannon Jones: Welcome to Industry Focus, the show that dives into a different sector of the stock market every day. Today is Wednesday, February 20th, and we're talking Healthcare. I'm your host, Shannon Jones, and I'm joined via Skype by Foolish contributor and medical device guru Brian Feroldi. Brian, how are you?

Brian Feroldi: Hey, Shannon! How's it going?

Jones: It's going well! I'm so glad to have you back, really excited to have you back for this topic in particular. We're talking about medical device monopolies, specifically three stocks we think could really drive shareholder returns for the long term. Brian, I'm excited to have you on the show to talk about these three stocks.

Before we jump into the stocks, though, let's level-set. I think it's important when we talk about medical device monopolies to really define what we mean by that. Do you want to give any context to that word, monopolies? I think there's a negative connotation, but from an investor's perspective, it's actually a real great thing.

Feroldi: When we talk about monopolies, we just mean that a company essentially utterly dominates its category, either through having immense market share or from having a lack of competition. That can happen for a variety of reasons. Sometimes regulatory, sometimes they're inventing a new category and they're growing it organically themselves, in which case they have nobody to compete against. But from an investor perspective, a monopoly is a wonderful thing because then the company can set prices, it can grow as the category grows, and it can deliver huge shareholder returns over time.

Jones: Absolutely. You talk about competition. That doesn't necessarily mean that these companies are in a class all by themselves. It may mean that there's limited competition or there's competition on the horizon, but it doesn't necessarily mean they're out on an island by themselves. As you mentioned, that comes down to more market share for them, and, more importantly, pricing power. I think that's really the advantage that these companies bring, especially those that have come as a first-to-market and they've been the pioneers in many of these device classes.

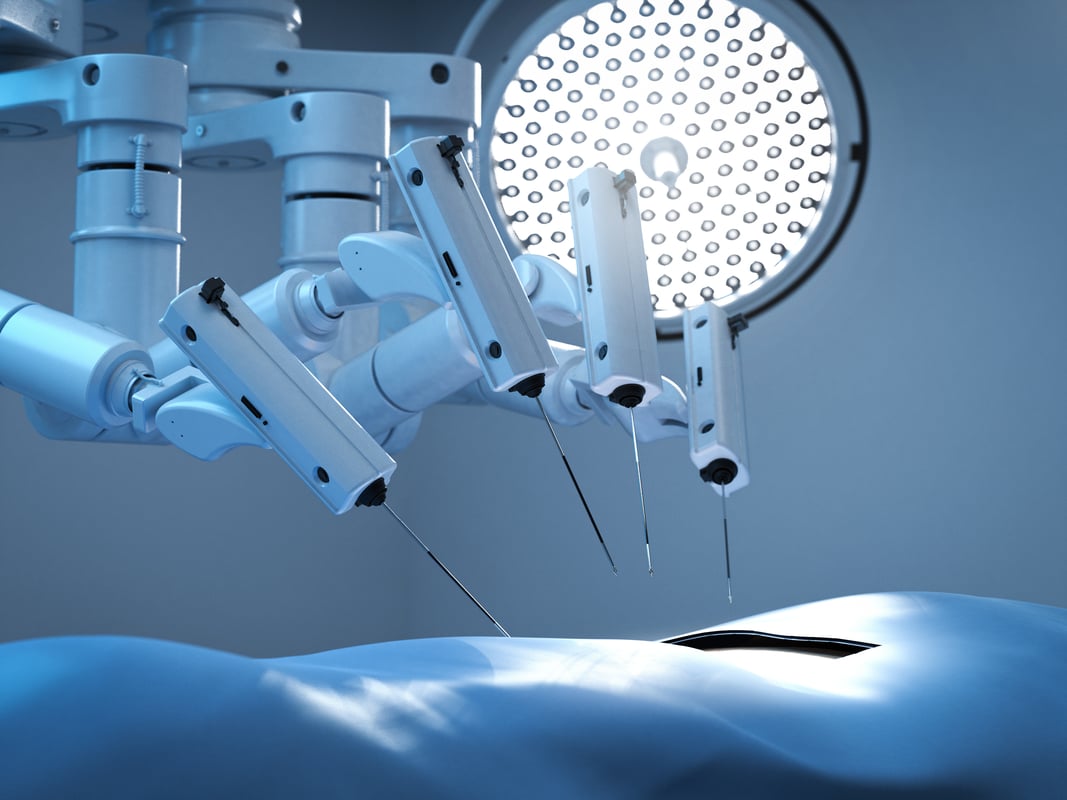

Let's dive right into the first one. This one is probably no shocker to many of our listeners. This is a Fool favorite. The first company is Intuitive Surgical, ticker ISRG, truly a medical device powerhouse. The company right now is sporting a market cap of about $62 billion. Again, true pioneers in this space. Brian, what can you tell us about Intuitive Surgical?

Feroldi: Intuitive Surgical was the first company to grow the concept of robotic surgery. These guys launched their system, which is called Da Vinci, literally 20 years ago in 1999. The idea was to use the robot, which has multiple arms, to assist surgeons with a variety of laparoscopic procedures. The advantage of using a robot was that the incision size would be much smaller. Robots have far more precision than the human hand can. You can go in, do the surgery, and close up the patient with much less scarring, much less blood loss, and that enables faster recovery time.

Intuitive Surgical focuses on a few surgical areas. It's expanded over time, but right now they're really big in urology, gynecology, and a catch-all category that they call general surgery. These guys have basically had this market all to themselves for the last two decades. They are the gold standard in robotic surgery. To date, there are 5,000 of their da Vinci systems placed around the world.

Jones: And it's really not even about just the systems here, Brian. It's also about the instruments that are used with the systems and all of the accessories that have to be replaced every single time they do a surgery. This is one of those tried-and-true business models, the razor and blades business model, that Intuitive Surgical has used in this space and used it very well. It's all of the instruments and the accessories that are replaced that, No. 1, is a recurring revenue stream for them. It's also a high-margin revenue stream for them. Right now, that makes up about 71% of total revenue for Intuitive Surgical.

If you look out over the last 10 years, the company's revenue and earnings have more than quadrupled. I think this will be a very long-term growth story for them. Really, again, pioneer in the use of robotic surgery. We'll talk about competition in a second. With that, you're going to have entrants that are going to want to come in and take advantage of the high revenue streams and high-margin products.

As you're diving into this company, one of the things I think to really watch for them is procedure growth. Brian, you mentioned urology, gynecology, general surgery. They're going to be expanding into indications beyond those. That'll be one thing to watch. Also, how many procedures they do in general. For 2019, they're guiding for about 13% to 17% growth in procedures. Compare that to fiscal year 2018, where they were guiding initially, at the beginning of the year, about 9% to 12% in procedure growth. Over the course of the year, they actually came out about 18% in procedure growth. I think for FY19, with their guidance, that 13% to 17% range, definitely doable. They've basically been able to prove that they can beat those numbers.

All in all, I like the long-term growth story. But as we talked about, Brian, competition is certainly right around the corner.

Feroldi: Yeah, you can't grow into a $60 billion business without other medical devices companies wondering what you're doing. There are a number of players that are really taking an interest in the robotic surgery market now that Intuitive Surgical has proved the category out. Two of the bigger ones for investors in Intuitive to keep an eye on are Johnson & Johnson, who actually has a partnership in place with Alphabet's Life Science division. They created a company called Verb Surgical. It's still in the clinical stage right now, but obviously, with J&J and Alphabet backing you, you have an unlimited source of funding to develop a system that will eventually compete with Intuitive. We haven't seen anything yet, but that could be on the horizon.

Medtronic is a medical device giant that has recently taken an interest in this category, too. They acquired a company called Mazor Robotics a year or two ago. Mazor had a robotic surgical system, but they focused on spine surgery. It was a different category of surgery than Intuitive. There's been a couple of companies like that that have come along. Another one is called MAKO Surgical, that was acquired a couple of years ago by Stryker. Those companies focused on surgery of the spine and the hips. They wouldn't compete directly with Intuitive because Intuitive is focused on minimally invasive surgery. But there's no doubt that a lot of large-cap companies have seen Intuitive's success and want in on the action.

Jones: Really, again, can't highlight how important it was for Intuitive to be the pioneer in this space. I saw an interesting stat, Brian. 84% of its U.S. customers at academic institutions actually use the da Vinci virtual reality simulator for training. What that means is, all of these new surgeons coming out of medical school are being trained on Intuitive Surgical's devices. That's huge! That means not only are they being trained on it, more than likely many of these large hospital systems which are connected with these academic centers are going to be continuing to use the same Intuitive Surgical devices beyond their training. Now you're looking at really high switching costs. So why would they go and buy one of these competitor products when their surgeons have already been trained on these devices, they know it well? I think this is a huge, huge advantage that Intuitive Surgical has.

Just looking at it, not only is that a huge advantage for them, but they've also got a growth story internationally as well. We talked about the U.S., but internationally, really, it'll come down to places like India, Taiwan, and China, where they're already starting to enter those markets. I think that'll be really a key story to watch as well.

Feroldi: I 100% agree with you there. Competition certainly will start to creep into this space, but one of the reasons that I personally love medical device companies is there is an enormous training component that has to happen on the healthcare provider level. Once a doctor, a nurse, a physician sits down and takes the time to learn and get really comfortable with the system, there becomes enormous switching costs for them to switch over to a competing system just because they're already set up, they're already happy, and they already have a system in place. I sold medical devices for 10 years and I saw that reluctance to learn something new firsthand. It's one of the reasons that I think the medical device industry is a wonderful place for investors to park long-term capital.

Jones: Absolutely! Next up, let's talk about another medical device company, one that was actually one of the top performers of the S&P 500 in 2018. That company is Abiomed, ABMD. It was up over 73% in 2018. Brian, here's another medical device company really focused on minimally invasive techniques and products. This is a company you actually got an opportunity to interview recently as well. What can you tell us about this company?

Feroldi: Abiomed has just been one of the best investments you could have made over the last couple of years. I believe their stock is up tenfold over the last, say, three or four years. That's because they've posted unbelievable revenue and profit growth as their Impella system, as it's called, has caught on. The Impella system is a miniaturized pump that is placed directly into a patient's heart either after they've had a heart attack or before they're about to undergo a very high-risk heart procedure. By placing this pump into their heart, it helps to keep the blood flowing throughout the body and it eases the stress placed on the heart either after the heart attack or before the surgery. Doing that allows the heart to heal much better than it would on its own.

In Abiomed's case, they're the only FDA-approved minimally invasive heart pump, miniaturized heart pump, that is on the market right now. They literally have a monopoly in their category. They're actually displacing an older technology that isn't nearly as clinically effective as the Impella system is.

Jones: I love how laser-focused this company is on the cardiology space. They've got the Impella device for, as you mentioned, these high-risk procedures, especially after a heart attack. But they're looking to expand into other cardiac therapeutic indications as well. They've got a long runway.

One thing that I noticed, a recent study showed that the Impella device actually increased survival rates by 24% in patients that went into cardiogenic shock. Not only is it helping to expedite recovery, but it's really helping increase survival, as well.

The reorder rate for the Impella devices, Brian, astounds me. The heart pump continues to be strong at 100%. It's going to be tough for any sort of competition to try to come into this space, I think.

Feroldi: Yeah. One of the questions that I had for the management team when I got to sit down with them was, "What's going to prevent somebody from coming in and knocking you guys off your perch?" And they had a number of answers for that. One of the big ones was just the training. I've seen this company's training facility. They fly doctors in from all over the world. They host regular chats and video conferences to make sure that people that are using this device really understand it fully. This is a company that is laser focused on training and developing as many relationships as possible with worldwide leaders in heart surgery. They have a tremendous, tremendous lead right now.

The thing that I find really compelling about their story is that in the U.S., which is their most developed market by far, their penetration rate is only about 10%. Only about 10% of procedures that could use Impella are currently using it. If you zoom out to the rest of the world, right now, they're only in Germany and they just recently launched in Japan. This company still has a tremendous runway for growth ahead of it, and that's super attractive given that they are, again, the only FDA-approved miniaturized heart pump on the market.

Jones: It doesn't just stop there. There are a lot of competitive advantages that I think Abiomed brings to the table. First of all, it's got over 200 patents right now and several hundred waiting to be approved. Not only that, you're talking about support. Brian, you mentioned the training that's involved. Seventy percent of Impella procedures have an Abiomed employee right there, which obviously strengthens that relationship between the company and many of these larger hospital systems. And then its data. I was fascinated by this. All the Impella devices that are in use actually send back data in real time to the company, which then allows them to provide continuous support. To start, I could see that data continuing to be used in other ways as well. They've got a number of really interesting competitive advantages in and of themselves.

This is another company to watch, also, when it comes to international expansion. You mentioned Germany, you mentioned Japan. Japan is actually the second-largest medical device market in the world. I think that's going to be critical to their long-term growth story as well.

Feroldi: Yeah, I 100% agree with you there. And there are so many other countries for this device to be used in over time. They also have multiple clinical studies going to expand the number of procedures that it can be used in today. The market opportunity is huge.

With that in mind, there are of course a number of companies that want in on this space. Again, the same names we keep hearing about over and over. Medtronic has eyes on this. There's also Abbott Labs, and there's a couple of companies that are no slouches themselves -- Edwards Lifesciences, Boston Scientific. They're all interested in this space and they're all developing their own technology to eventually compete with Abiomed one day. But for those devices to get on the market, they would have to clear a significant regulatory hurdle. And then, again, right now, Abiomed has a huge head start, a multiyear lead, on all these companies. I have a hard time seeing anybody else come into this market and knocking Abiomed off its perch.

Jones: Totally agree. Let's talk about our last stock. This one is so interesting to me. No. 1, I don't think it's nearly as well known or recognized as the other two that we talked about. But I'm even more fascinated by its technology. The company we're talking about is actually targeting one of the hottest areas of investment in healthcare, and that's cancer, oncology. We've talked about it a lot on Industry Focus: Healthcare. But I would say this is probably the riskier of the bunch. The company is called NovoCure, ticker NVCR. Brian, what can you tell us about their innovative approach to treating cancer?

Feroldi: NovoCure is really an odd duck in the healthcare world. They're a medical device company that's targeting cancer. They developed this therapy which they call tumor treating fields, TTFields. What they basically found was that if you create an electric field and tune it to specific frequencies, it inhibits cell division in cancerous tumors. This is a device that they have FDA approved, it's on the market. You put it on your head. It looks like a swimming cap, basically, with some cords coming off. And this cap creates a continuous flow of electric fields that disrupt cell division in brain cancer tumors right now. That's what it's FDA approved for.

It sounds crazy because there are no side effects. It's just something you wear on your head. But they have clinical data that proves that if you use this device alongside standard-of-care chemotherapy and radiation, it leads to better health outcomes, a longer life. In fact, they recently came out with a study that showed the longer you wear it, the higher the benefits, which makes sense, given that the therapy itself works.

These guys were laughed at when they first came out because the concept was so radically different than anything else that was out there. Most people are used to treating cancer with either surgery or with different chemotherapy. The idea of treating it with a medical device was basically crazy. But these guys have been at it now for over 15 years, and they've had it on the market for more than four years now, and they have long-term data that basically proves that using this device does work.

Jones: What's fascinating to me -- I have to admit, I was a little skeptical when I first heard you mention this company. But No. 1, they've already got one FDA approval. It looks like they've got indications that could expand their total addressable market so much further. Right now, you're looking at about, 12,000 to 14,000 just in the glioblastoma space, and that's really aggressive brain cancer. But they also have a few phase 3 trials, one in lung cancer. Lung cancer has been a very hot area specifically within oncology, as you've got your checkpoints and potentially at one point CAR-T therapy could even be used for that. But solid tumors continue to be the holy grail of oncology. You've also got pancreatic cancer, and then you've got your brain metastases. The stat that I came across, an estimated 24% to 45% of all cancer patients, not just those with brain cancer, in the United States have these cancer cells that have made their way to the brain. That could widely expand their total addressable market if they go after that. Right now, it looks like that's in a phase 3 trial in and of itself.

You've got multiple shots on goal with this company. I think what's even more interesting is being able to see this therapy in combination with some of those tried-and-true therapies like checkpoint inhibitors, like CAR-T therapy. I think it becomes a much more interesting concept, and even more importantly, potentially a more efficacious treatment, if you can combine the physics behind this company with also the pharmacokinetics that are happening with many of these drugs.

All in all, a lot to like with this company. We'll have to wait and see if they're able to expand their pipeline and get some more approvals. But a really, really interesting one to watch. I'd say, Brian, of the three, probably this one is riskier out of the bunch. Would you agree?

Feroldi: Oh, absolutely! I mean, NovoCure is still unprofitable. But one of the things that attracts me to this business is they've already proven out that the device works in brain cancer. Since it's a device that has no side effects -- literally no side effects at all -- when you compare that to other forms of cancer treatment, I think the odds of it working in other solid tumors that you mentioned, especially lung cancer, if they can prove that it works and win FDA approval, this company's total addressable market just explodes. You're talking about over 10 times, in terms of the size difference between what they can be approved for in the future.

The other thing I like about this company is, I dug through this company's 10-K. There's literally no other company that they know of that is working to develop TTField therapies. The only competition that they could think of was to talk about other biotech drugs that could potentially render their technology useless one day. This is a company that, if TTFields is the real deal, you do not have to worry about anybody else coming in and encroaching on their space at all. That's very attractive.

Jones: Great! Brian, to close us out, any closing thoughts? Any words of wisdom for investors out there thinking about investing in these medical device monopolies?

Feroldi: I would just say, get to know them! One of the things that I love about the medical device industry is that once a company shows success and gets out there and gets training, it becomes huge. The switching costs to go to a rival device are just huge. I got to see that firsthand when I was working in the industry.

I know that medical device stocks don't get enough attention, enough attraction from investors because they can be hard to understand. But they can be a very lucrative place to invest, so give them a chance.

Jones: That's right. 2018 was the year of medical devices. Those were the stocks that outperformed even the biotechs that are out there. A lot to like in this space. Brian, we'll have to do this again, maybe give some updates on some of these top stocks.

Feroldi: Sounds like a plan to me!

Jones: Sounds like a plan! Well, that's it for this week's Industry Focus: Healthcare show. Thank you so much for tuning in! As always, people on the program may have interest in the stocks they talk about, and The Motley Fool may have formal recommendations for or against, so don't buy or sell stocks based solely on what you hear. This show is produced by Austin Morgan. For Brian Feroldi, I'm Shannon Jones. Thanks for listening and Fool on!