Tech giant Broadcom (AVGO -1.66%) is a best-in-breed business. The company has a large and thriving semiconductor business that has exposure to a number of lucrative markets, including wireless chips for premium smartphones, network infrastructure silicon, and broadband access chips. Broadcom also recently began a push into infrastructure software, which has not only boosted the company's revenue and free cash flow, but has helped to further enhance its gross margin profile, too.

Broadcom stock has been a winner in recent years, handily outperforming the overall semiconductor sector as measured by the iShares PHLX Semiconductor ETF over both the last year and the last five years.

Image source: Getty Images.

While that strong performance has obviously been great for investors in Broadcom thus far, those looking to establish new positions or add to their existing ones should be asking the following question: How much upside is there left in Broadcom shares?

No investment is a guarantee, but I think Broadcom stock can continue to outperform its semiconductor peers over the next five years. Here's why.

A great business on the cheap

Broadcom is a great business that has consistently delivered growth in revenue and free cash flow through a combination of both organic efforts -- such as selling increasingly capable and, therefore, expensive components to customers -- as well as through the acquisition of other best-in-breed businesses. (Broadcom also has a knack for optimizing the businesses that it acquires to maximize sustainable free cash flow generation.)

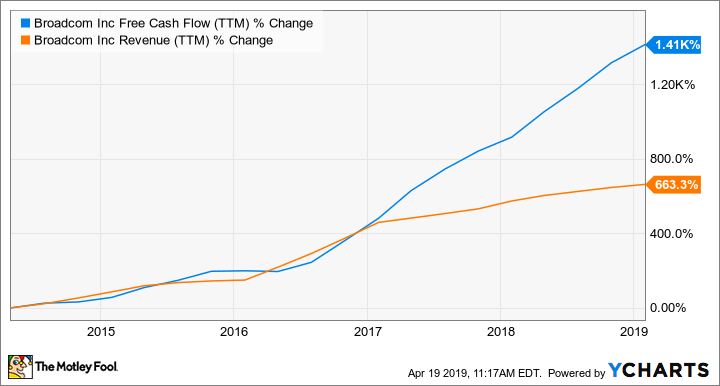

Indeed, over the last five years, Broadcom's revenue has grown by 663% and its free cash flow has surged by about 1,410%, illustrating the significant leverage in the company's business model.

Broadcom Revenue and Free Cash Flow, data by YCharts.

What's really interesting, though, is that despite years of solid financial execution (underpinned by a combination of strong technical execution and business acumen), Broadcom shares are still quite cheap. Management expects free cash flow to reach $10 billion this year. At the company's current market capitalization of about $126 billion, investors are valuing the stock at 12.6 times expected 2019 free cash flow.

That's the kind of multiple that would be appropriate for a business that's not growing particularly quickly. Relative to Broadcom's apparent long-term growth prospects, this is downright cheap.

Weighing the long-term prospects

Broadcom has historically been a semiconductor-only business. However, with its recent entry into the infrastructure software business, it now has a collection of solid semiconductor franchises as well as significant exposure to higher-margin software. These all seem like segments that can drive long-term growth.

Indeed, while Broadcom's chip business is currently suffering a slump -- something that is being driven "almost entirely by the [seasonal] drop in wireless," according to CEO Hock Tan -- the company is betting that the second half of the year will be a lot better.

"But looking to the second half, we are confident that [the] semiconductor business will resume very meaningful growth," Tan said. "This will be driven by strong product cycles in both wireless and networking coupled with a recovery in broadband."

Broadcom's infrastructure software business -- which the company built with its recent acquisitions of Brocade and, more importantly, CA Technologies -- is already proving its worth. Unlike the semiconductor business, which is facing a relatively rough first half of fiscal 2019 followed by an expected recovery in the second half, Broadcom's infrastructure software segment "is expected to sustain throughout the year."

So, Broadcom has a collection of generally excellent semiconductor franchises spanning a range of applications including network infrastructure, broadband access, and wireless chips. Meanwhile, its relatively new infrastructure software business is delivering substantial revenue and is boosting the company's gross margin profile (Broadcom's gross margin in the first quarter of fiscal 2019 was 71.4% -- up 660 basis points year over year).

I think that Broadcom's existing businesses offer meaningful and sustainable long-term growth potential. A key pillar of Broadcom's growth strategy, though, is that it routinely identifies excellent acquisition targets, leverages the financial wherewithal to complete them, and then does the necessary legwork to shape those newly acquired businesses to fit in with the company's overall strategy, which is to own and fuel a collection of best-in-breed businesses that can predictably throw off a lot of free cash flow.

Investor takeaway

Ultimately, it boils down to this: Broadcom is a cheap stock that's underpinned by a highly successful business. The company is somewhat unorthodox with its strategy of acquiring good businesses and transforming them into veritable free cash flow generating machines, but it's a strategy that has worked and continues to work for Broadcom.

Considering that excellent long-term potential, coupled with a generous dividend yield of about 3.3% (Broadcom commits to paying out no less than half of its previous year's free cash flow in the form of a dividend in any given year), this chip stock could continue delivering market-beating returns for years to come.