The name United States Steel (X +0.00%) carries a lot of weight, even though the company is no longer as dominant as it once was. In fact, the deep steel industry downturn following the 2007-2009 recession took a huge toll on the company, leading to red ink in all but one year between 2009 and 2016. However, the iconic domestic steel mill has been working to get its business heading in the right direction again. One big step was reducing debt, and there U.S. Steel has made a lot of progress. But is that going to be enough when the next downturn hits this highly cyclical industry?

When it was bad

When the last steel industry downturn hit, U.S. Steel's long-term debt accounted for around 40% of its capital structure. Compare that to Nucor (NUE +2.23%), the largest player in the domestic steel market, where long-term debt was roughly 30% of the capital structure. Nucor's debt levels were clearly lower, but the difference didn't seem that extreme.

Image source: Getty Images

As the downturn progressed, however, the differences between the two companies started to become more obvious. Nucor lost money in 2009, but that was it. It remained solidly profitable thereafter. One of the big reasons for this is the fact that its business is based on electric arc furnaces, which are more flexible than the blast furnaces that underpin U.S. Steel's operations.

With a still profitable business, Nucor was actually able to invest in its operations during the downturn so that it would be better positioned for the next upturn. (That's part of the company's normal playbook, along with modest use of leverage.) Debt never became a big issue.

U.S. Steel's blast furnaces, however, left it with high costs, red ink, and some big asset write downs as steel demand waned. It was basically forced to restructure in an attempt to survive. Long-term debt actually inched higher until 2012 (hitting 53% of the capital structure), when management realized the company had to get serious about its balance sheet and trim its debt load. Asset write downs, which reduced retained earnings and shareholder equity, combined with the ongoing red ink (which also reduce retained earnings), however, continued to keep leverage high. As recently as 2016 long-term debt made up more than half the capital structure.

The turn finally comes

When earnings turned positive in 2017, U.S. Steel's balance sheet started to look a whole lot better. Debt continued to decline, and with shareholder equity moving higher (fueled by an increase in retained earnings), leverage at the end of 2018 was far more modest -- long-term debt made up just 35% of the capital structure. That's within striking distance of Nucor's 30%.

X Total Long Term Debt (Quarterly) data by YCharts

First-quarter results didn't change these figures much. However, what is clear is that U.S. Steel is working with a much stronger financial foundation today than it was during the downturn.

That said, like many of its peers, it has started to invest in its business again now that the domestic steel industry has rebounded. It is notably reopening shuttered mills, while also looking to expand other assets. Between 2019 and 2022 U.S. Steel is looking at roughly $1.2 billion worth of capital investments.

Truth be told, the future would look pretty bright for U.S. Steel today if it weren't for the fact that a significant portion of the business is based on blast furnaces. These assets require high utilization rates to remain profitable compared to more flexible electric arc furnaces. So when the next downturn hits, and it will eventually hit, U.S. Steel's current round of spending could easily get derailed by red ink -- or at the very least cause a notable increase in leverage again.

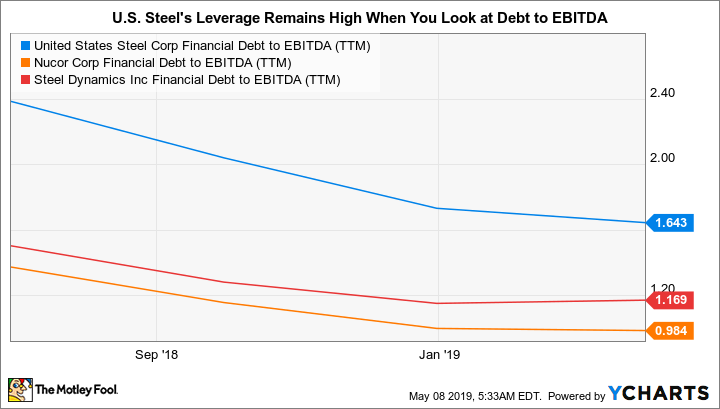

X Financial Debt to EBITDA (TTM) data by YCharts

That's doubly true when you look at leverage by examining the debt to EBITDA ratio, which gives an idea of how a company's financial results are supporting its debt load. Although debt reduction and improved profitability have greatly reduced U.S. Steel's debt to EBITDA ratio, it is still roughly 1.6 times. That's quite a bit higher than Nucor's modest debt to EBITDA ratio of just 0.98 times. Nucor is in a much better position to handle the gales of an industry downturn than U.S. Steel, even after all the work U.S. Steel's management team has done.

Adding insult to injury here, U.S. Steel's operations require a steady supply of iron ore from companies like Cleveland-Cliffs (CLF +15.98%). This iron ore pellet supplier, however, is openly warning that there isn't enough domestic supply to meet projected demand. And it has no intention of adding any new supply unless it gets long-term contracts that ensure it a decent rate of return. So far industry players have been unwilling to sign such deals. This, in turn, could lead to higher input cost prices for a steel mill like U.S. Steel -- that could keep debt to EBITDA troublingly tight even in a good market.

Pick a better proposition... and wait

Steel is a highly cyclical industry. Although U.S. Steel has done an impressive job of fixing its balance sheet, leverage remains a weak spot for the company compared to more financially conservative peers like Nucor. Add in the difference in the technology backing their operations and there's a material likelihood that the next downturn will be harder on U.S. Steel than Nucor.

U.S. Steel will probably muddle through and survive to fight another day, just like it did during the last downturn. But most investors would be better off buying a company like Nucor, that sailed through the downturn (relatively speaking) while expanding its business so it could thrive when the next upturn came around. The vexing problem here for U.S. Steel is that even if times are good it could still face troubles because of the iron ore supply issue that Cliffs is warning investors about today.

That said, an industry upturn like the one the domestic steel market is currently experiencing isn't the best time to buy a cyclical steel company, so neither U.S. Steel nor Nucor is likely to be a great investment choice today. But for investors looking at the steel space, despite the improvements being made at U.S. Steel, Nucor should be on the wish list for the next downturn, while U.S. Steel should probably still be avoided.