What happened

Shares of Planet Fitness (PLNT 0.54%) weren't looking so fit last month. The discount gym's stock dropped 18%, according to data from S&P Global Market Intelligence.

There was no company-specific news out on Planet Fitness. Rather, the stock seemed to drop as investor sentiment turned after the stock peaked over the summer. Meanwhile, investors seemed to be moving away from growth stocks more generally. A number of high-priced stocks fell last month, as investors instead piled into value plays in the retail and energy sectors, among others.

Image source: Planet Fitness.

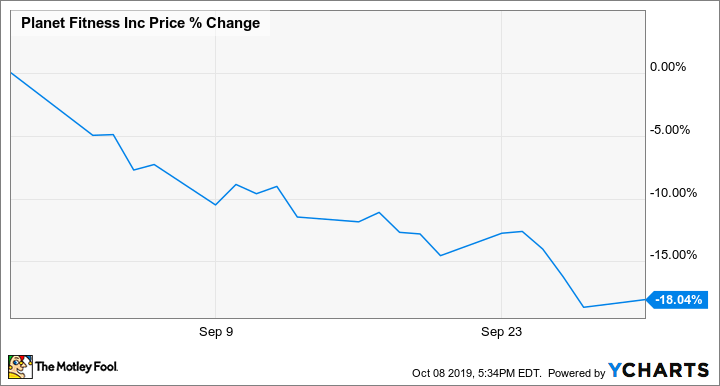

The stock slid steadily over the course of the month, showing that no single event caused the sell-off:

So what

The subscription-based budget gym has been an outperformer since its 2015 IPO, having risen as much as 400% since its debut. The company has benefited from a changing retail environment that has seen mall vacancies spike, leading to landlord demand for tenants like Planet Fitness that can bring in customers frequently.

However, for a commodity business, the valuation often looks stretched. And the market seems to have called the end of the rally, given that September marked the second straight month of double-digit losses for Planet Fitness.

What also may have contributed to the sell-off last month was the disappointing debut of Peloton (PTON 0.87%), the maker of at-home interactive bike and exercise machines. Although Peloton, which sells its machines for upwards of $2,000, is not a direct competitor of Planet Fitness, which caters to a more a price-sensitive customer, the weak performance of Peloton may signal the market's lack of interest in fitness stocks.

Peloton shares are down 20% from their IPO two weeks ago.

Now what

Despite the sell-off last month, Planet Fitness' growth path continues to look solid. The company has nearly 2,000 locations and sees room in the market for 4,000, and its franchise model has been able to generate high margins. However, at a P/E ratio of 46, the stock is still pricey by conventional standards. The stock has fallen by about 3% so far in October, a sign that the stock may have further to slide before it reaches an equilibrium point.