For much of the past three months, Wall Street has been taken on a once-in-a-lifetime ride. Panic surrounding the spread of the coronavirus disease 2019 (COVID-19) wound up pushing the benchmark S&P 500 down as much as 34% in just over a month. Although the market fiercely bounced back in the weeks that followed, the CBOE Volatility Index remains highly elevated from its historic average, and little certainty still exists with regard to a timeline of when business activity will return to normal.

Yet, one sector that's emerged from the coronavirus pandemic relatively unscathed is healthcare. Though there will be pockets of industries that could be strained by COVID-19, such as hospitals and insurers, the bulk of healthcare stocks have been well insulated. That's because people don't get to choose when they get sick or what ailment(s) they'll develop, creating a steady stream of potential cash flow for healthcare companies up and down the supply chain, regardless of how well or poorly the economy is performing.

Of course, no two healthcare companies are created equally. In an ideal scenario, investors want to buy into businesses that offer sustainable competitive advantages for a long time to come. I believe that's exactly what you're going to get with the following three healthcare stocks.

Image source: Getty Images.

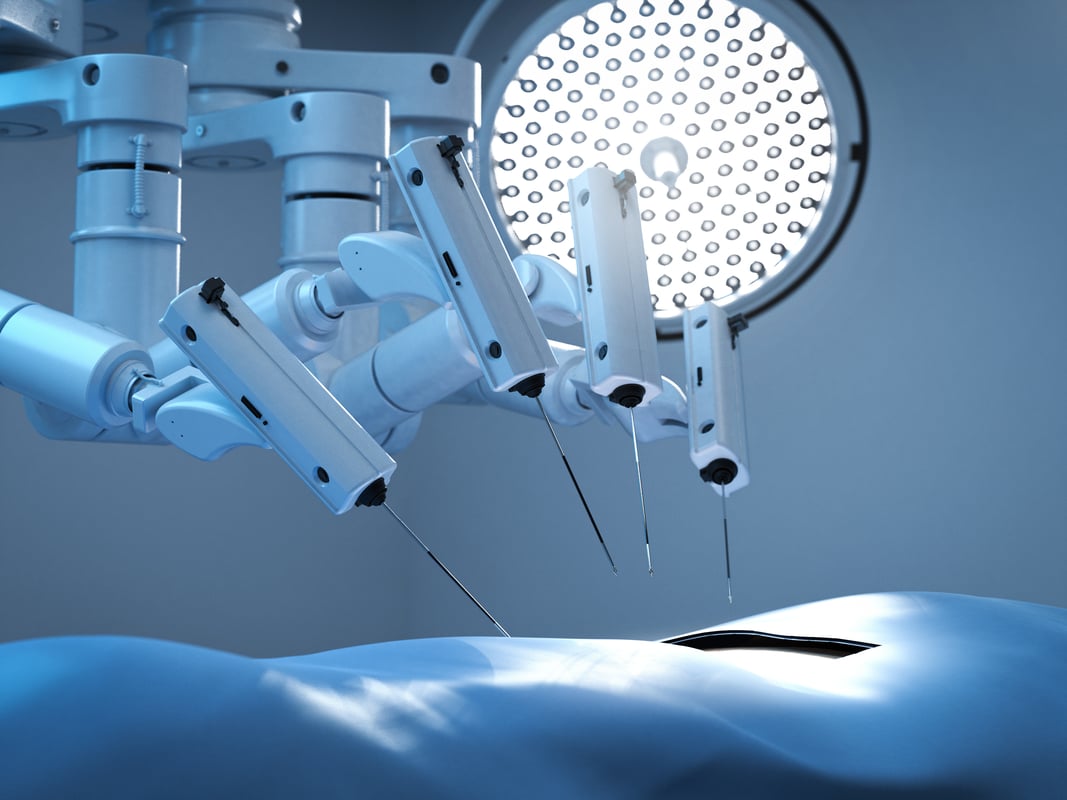

Intuitive Surgical

It's been my contention that the most sound company in the entire healthcare space is surgical system manufacturer Intuitive Surgical (ISRG 0.46%), and that has a lot to do with its unique competitive advantages in the surgical-assistance space.

At the end of the first quarter, Intuitive Surgical had 5,669 of its da Vinci surgical systems installed around the world. You could add up all of the company's competitors and you wouldn't even come close to hitting the number of systems Intuitive Surgical has in operation. Not only does this make Intuitive Surgical the logical go-to for a hospital or surgical center in the market for an assistive surgical system, but it makes it highly unlikely that the company will experience any future client churn.

The best part of having the most popular surgical system in the world is that Intuitive Surgical's margins are built to keep improving over time. You see, the da Vinci system, while costly at $0.5 million to $2.5 million per machine, isn't a high-margin product. It's an intricate system that's costly to build. Intuitive generates the bulk of its margin from selling instruments and accessories with each procedure, as well as in servicing its machines. As the number of installed da Vinci systems has grown, these higher-margin revenue streams have combined to dwarf system sales.

Intuitive Surgical also has an extensive runway when it comes to building up its soft tissue surgical market share. Though already dominant in gynecology and urology procedures, the expectation is that the da Vinci system can gain significant share in thoracic, colorectal, and general surgical procedures in the decade to come.

At the moment, no competitor stands a chance of dethroning this surgical king.

Image source: Getty Images.

Alexion Pharmaceuticals

Investors should also keep an open mind about specialty drug developers. Despite the finite patent exclusivity period of brand-name therapies, a handful of drug developers, such as Alexion Pharmaceuticals (ALXN +0.00%), can maintain a nearly impenetrable moat.

For quite some time, Alexion has made its living by riding the coattails of blockbuster drug Soliris, which is approved to treat a handful of ultra-rare indications. By focusing on these exceptionally rare indications, Alexion hasn't had to deal with much in the way of competition. That's opened the door for it to capture pretty much all of the share in select indications, as well as charge a very high price point for Soliris (in the neighborhood of $500,000 per year).

However, there'd been concern that generic forms of Soliris could eventually disrupt Alexion's growth trajectory. That's why it was so important for Alexion to develop and introduce its next-generation therapy Ultomiris last year. Ultomiris is designed to eventually replace Soliris in its existing indications. The best part is that Ultomiris only needs to be administered once every eight weeks, as opposed to once every two weeks with Soliris, meaning it's an improvement in patient quality of life. That tosses the idea that generic Soliris is going to be a threat out the window.

Alexion has also turned to acquisitions to maintain its moat. Earlier this month, it announced that it would be purchasing Portola Pharmaceuticals for $1.4 billion to get its hands on Andexxa, the only approved Factor Xa inhibitor reversal agent.

The point being that Alexion's cash flow has been well-protected for more than a decade, and should continue to remain that way for many years to come.

Image source: Getty Images.

Livongo Health

A third healthcare stock that appears to boast a considerable and sustainable competitive advantage is solutions provider Livongo Health (LVGO +0.00%).

What differentiates Livongo from a sea of medical device and solutions companies is the fact that it's leaning on a mountain of data aggregation and artificial intelligence to help change the behavioral habits of persons with chronic conditions, such as diabetes and hypertension. For the time being, diabetes is Livongo's primary focus.

Within the U.S., the Centers for Disease Control and Prevention estimates that 34.2 million people (10.5% of the population) have diabetes, with another 88 million demonstrating prediabetes symptoms. This represents a massive potential patient pool that seemingly keeps growing every year. And while the co-morbidities associated with diabetes can be troublesome for patients, their inaction with regard to staying on top of their disease (e.g., taking blood glucose readings) can be a major factor in their overall health. Livongo's solutions help incite behavioral change and ensure a healthier lifestyle.

The best part for long-term investors is that Livongo is just scratching the tip of the iceberg in terms of the number patients it's assisting. It ended the first quarter with more than 328,000 Diabetes Members, representing a doubling the previous year. Yet, this doesn't even represent a full 1% of the total number of diabetics in the United States.

Furthermore, as a subscription-based service, the revenue Livongo Health generates tends to be highly predictable, allowing management a clear outlook with which to make capital expenditure decisions.

Livongo Health has all the tools necessary to grow into a healthcare giant.