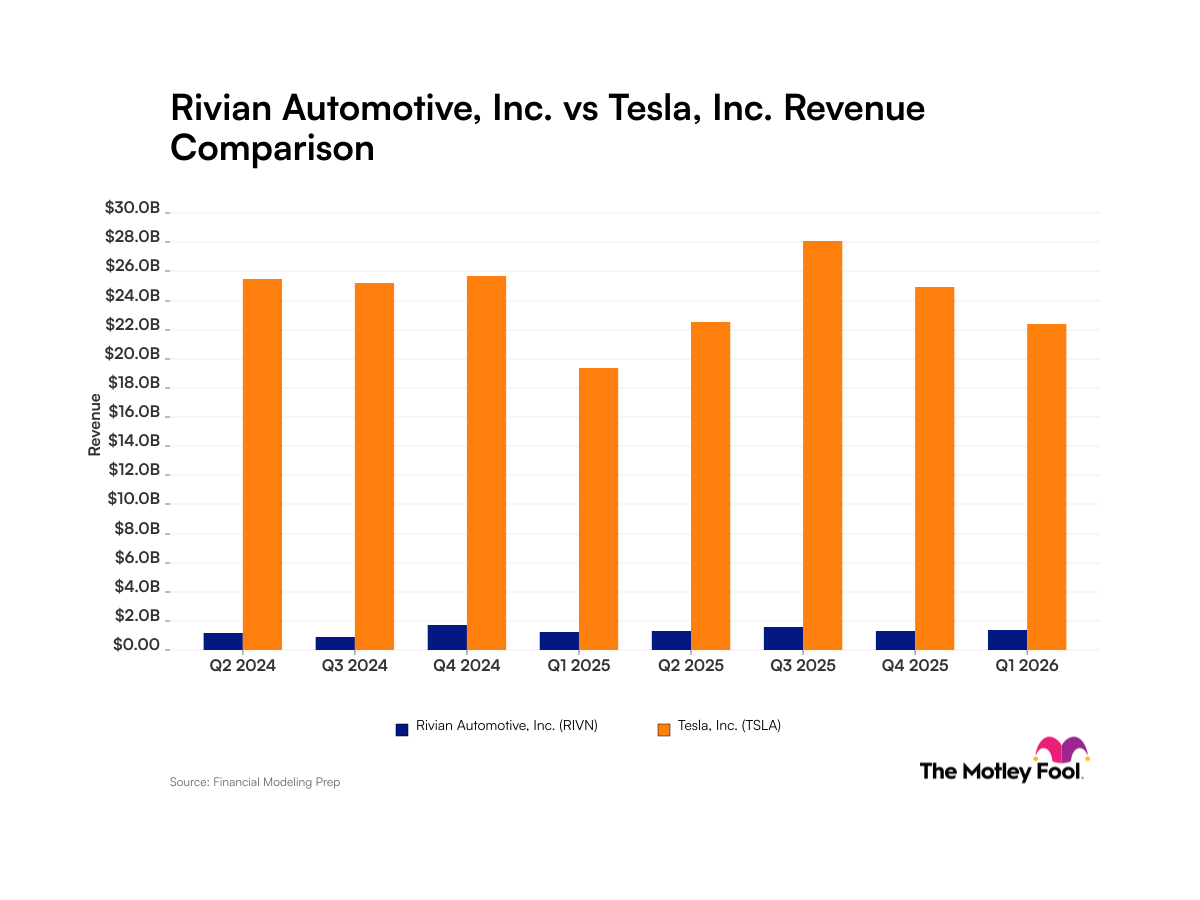

Tesla (TSLA +0.22%) stock has risen 800% over the past 12 months. Yet one analyst thinks there's still significant upside ahead for the stock. The key catalysts that could drive the stock higher? Expanding profit margins and a growing addressable market.

Here's a look at this analyst's extremely bullish view for the growth stock.

Image source: Tesla.

The path to $578

Shares of Tesla could rise to $578 over the next 12 months, according to New Street analyst Pierre Ferragu, a longtime Tesla bull. This optimistic price target represents a more than 35% upside from the stock's closing price on Friday.

The thesis of Tesla becoming a profitable premium car manufacturer is increasingly becoming accepted as fact, the analyst says. This differs from years past, when many investors debated whether the company would even survive. Further, Ferragu believes demand will be robust for the company, with the only limiting factor to Tesla's growth over the next five years being its ability to ramp up production. This will lead to strong pricing power and an expanding margin for this core segment, Ferragu says.

Looking beyond vehicles, the analyst points to the company's growing bet on the energy market. The automaker's solar power and battery-powered energy storage products help Tesla tap into an incremental $750 billion addressable market, according to Ferragu.

Tesla's energy business

Tesla has said it believes that its energy business could eventually rival its auto business.

Image source: Tesla.

"And the mission of Tesla is to accelerate sustainable energy, so I can't emphasize enough: Yes, [Tesla's] battery and solar [businesses] will both be enormous, and they kind of have to be in order ... [for] us to have a sustainable future," explained Tesla CEO Elon Musk in the company's second-quarter earnings call. Musk also notes that he believes the addressable market energy is ultimately bigger than autos, creating a significant opportunity for the company to gain market share.

Tesla isn't all talk when it comes to its nascent energy business. The company's new utility-scale energy storage product, Megapack, is already profitable, and orders are robust. "[T]here's a lot of demand for the product," explained Senior Vice President of Powertrain and Energy Engineering Drew Baglino in Tesla's second-quarter earnings call, "and we're growing the production rates as fast as we can for that product."

But here's the catch: Tesla's energy business still pales in comparison to its automotive business. Of Tesla's total revenue in Q2, only 6% came from energy generation and storage. Further, this segment's revenue only increased by $1 million year over year in Q2, growing from $369 million to $370 million. It's too early to know if Tesla can win in this segment the way it is in electric cars.

Ferragu's optimism for Tesla stock is bold, but his upbeat view of the company's energy business should be taken with a grain of salt.