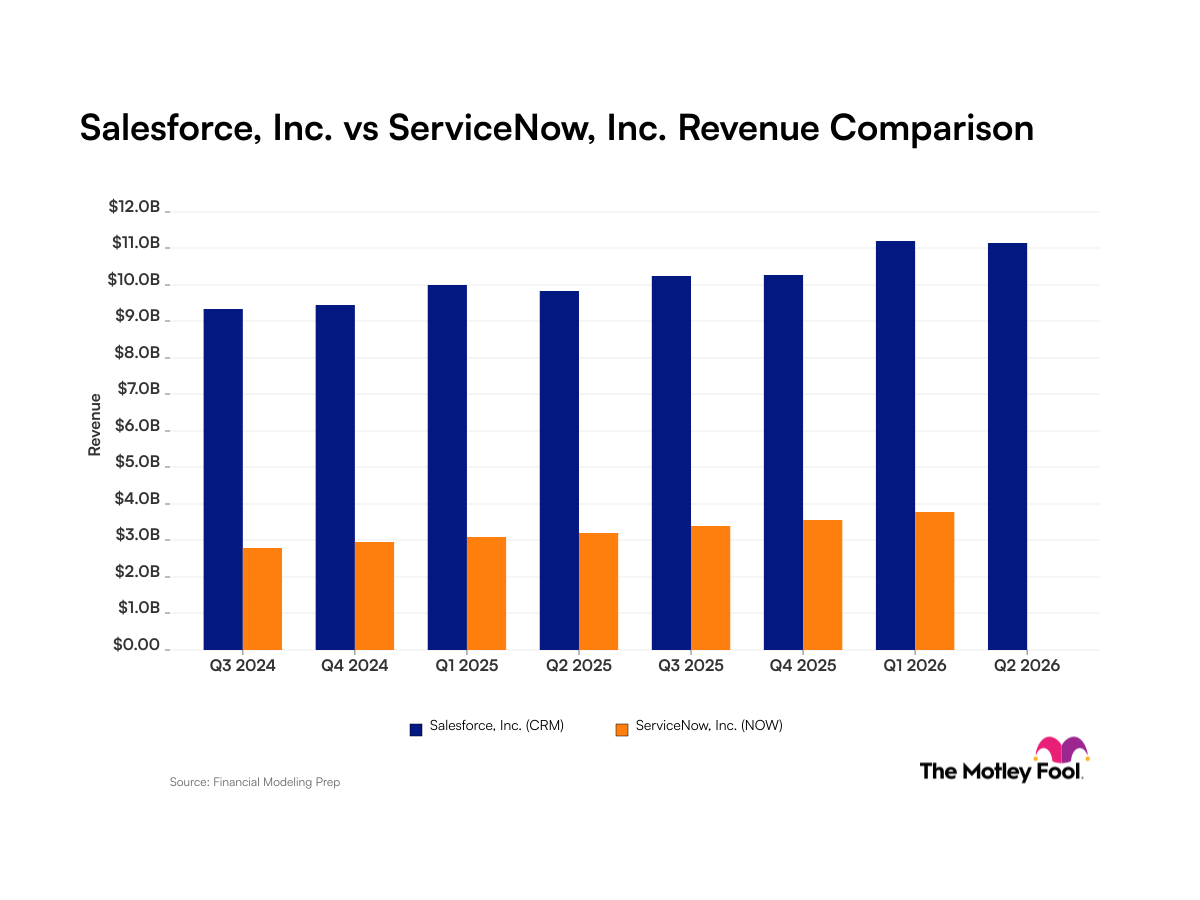

ServiceNow (NOW +10.34%) provides software-as-a-service (SaaS) platform solutions to optimize digital workflows for companies in the United States and internationally. ServiceNow's stated goal is to be the "defining enterprise software company of the 21st century."

Investors are certainly impressed with the performance. The company's stock has returned over 2,700% over the last 10 years. This year to date the stock has gained over 25% and pushes to new all-time highs consistently. While the past and present are impressive, the company also has a very bright future which should lead to further investor profits.

Source: Getty Images.

Tremendous cash flows being generated

The ServiceNow story should be required reading for every budding SaaS company investor. The company has been growing revenues at a compound annual growth rate (CAGR) over 35% for the last five years. It has a tremendous gross margin over 75% and smoothly scaled to profits, while producing impressive cash from operations (CFO).

The company went from generating $159 million in CFO in fiscal 2016 to an incredible $1.8 billion in fiscal 2020. Over this same period the company has also become profitable on a GAAP basis. ServiceNow generates these cash flows by keeping debt down -- less than $1.5 billion at last report -- and improving margins through scale. Five years ago, in 2016, the EBITDA margin was -2%, however it has steadily risen to over 12% in 2020.

Source: ServiceNow.

Shown above, revenue, EBITDA, and EBITDA margin have risen consistently each year. This is textbook scaling to profitability and ServiceNow has been highly successful as a result.

But will the outperformance continue?

It is natural for any investor to believe they have missed the boat if they did not catch it close to the launch point. However, ServiceNow is set to continue to dominate the broader market. First, revenues are expected to reach at least $5.6 billion for the full year 2021-another 30% increase over 2020. 98% of revenues are subscription-based or annual recurring revenues (ARR). This means that renewal rates are a key to continued dominance. Luckily, ServiceNow is reporting renewal rates over 97% in most quarters.

This low churn is coupled with impressive increasing utilization of the company's services by existing customers. In the third quarter of 2019, customers spending more than $1 million in ARR with ServiceNow averaged $3 million per year. In Q3 2021 this was up to $3.6 million, a 20% increase in just two years. Speaking of customers, ServiceNow counts over 6,900 in all and 80% of the Fortune 500 among them. ServiceNow is an integral part of the business world.

ServiceNow stock still has room to grow

ServiceNow is guiding for $5.5 to $5.6 billion in revenues in fiscal 2021. It expects to reach $10 billion in revenue by 2024 and $15 billion by the end of this decade. The company continues to expand offerings and expects a total addressable market (TAM) of $175 billion by 2024. Even after the meteoric rise of the last 10 years, the runway remains long for this company. Its stock has always been somewhat of a Wall Street darling, attracting increasing targets and praise for years.

ServiceNow trades at a price-to-sales (PS) ratio over 23 on a forward basis. This drops to just over 18.5 based on fiscal 2022 estimates. This lofty valuation has not stopped analysts from increasing price targets. This is likely due to the tremendous cash flows and compelling continued growth of the company. According to Yahoo, 30 out of 34 analysts are net bullish on the stock, with just four setting hold ratings.

The verdict

ServiceNow is well on its way to meeting its stated mission as a market defining software company. The business will make over $5 billion in revenue this year and has a clear pathway to $15 billion by decade's end. CFO has increased exponentially as the company uses its superior margins to scale to profitability. Current customers continue to spend more each year and the product is incredibly sticky. Wall Street continues to be bullish despite the already large gains and relatively high valuation. ServiceNow stock has crushed market returns over the last decade and this will likely continue for long-term investors.