Social media giant Meta Platforms (META +0.66%) was once a trillion-dollar company, but its questionable heavy investments in the metaverse and reduced ad revenue related to privacy changes in the Apple operating system have cooled Wall Street's enthusiasm. Today the stock sits almost 52% off its high and at a market cap of $477 billion.

Meta isn't perfect. It's pretty clear the company is working through some short-term challenges. But if you're looking for a stock that could double by 2030, Meta has the characteristics to do it. Let's look at the math and catalysts that underline the stock's potential path back to the trillion-dollar club.

Meta's health isn't as dire as it looks

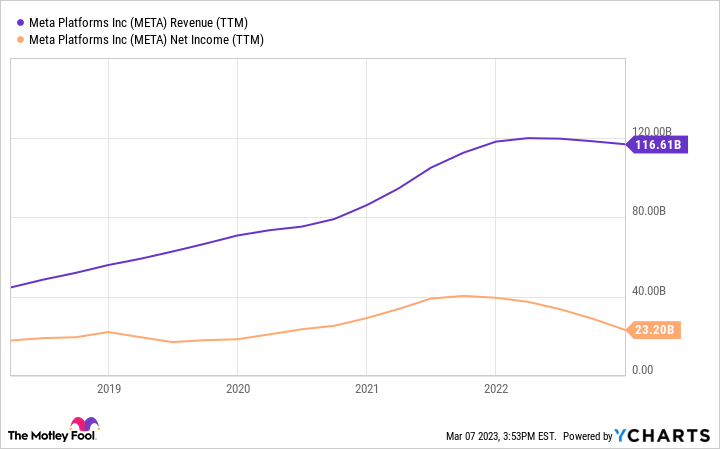

By some standards, it would appear that Meta's revenue and profits have stopped growing. That's led some to assert that Meta's golden years are over. But a deeper dive into the numbers challenges that assertion.

It's important to acknowledge that Meta's facing some challenges right now. First, Meta's Reality Labs segment, which houses its metaverse business, is pursuing a long-term agenda that's nowhere near profitability today. The segment posted operating losses of $13.7 billion in 2022, a significant drag on Meta's bottom line.

Second, the advertising environment right now is very soft for Meta as well as other ad-tech companies. Meta generates most of its revenue by selling ads to companies hoping to reach its massive user base through apps like Facebook, Instagram, and WhatsApp. Meta's price per ad decreased by 16% in 2022. That drop was partially offset by an 18% increase in volume. Considering this drag on Meta's business, managing to still generate $19 billion free cash flow in 2022 seems impressive.

META Revenue (TTM) data by YCharts

In fact, Meta's family of apps continues growing its user base; monthly active users increased 4% year over year to 3.74 billion in the fourth quarter. Meta can monetize these new users now, and as ad spending recovers in the future. One should worry if users fled Meta's apps, but that's not the case.

Multiple potential catalysts coming

Looking ahead, Meta's growth could pick back up from several factors, including:

Ad spending recovering: Companies will probably loosen their wallets on ad spending at some point. Not only should the economic environment improve over time, but there are several election cycles (including two presidential election cycles) between now and 2030. A study estimated that advertising spending hit $9.7 billion for the 2022 elections (which wasn't even a presidential election year), so politics are often great for business.

Short video monetization: Major competitor TikTok remains controversial and could even face a potential ban if U.S. relations remain tense with China. CEO Mark Zuckerberg has carefully managed the growth of Facebook and Instagram Reels, its internal competitor to TikTok. Monetization of Reels is in the early stages, which could boost Meta's top and bottom lines if successful.

NASDAQ: META

Key Data Points

Continued buybacks: Meta loves massive share repurchase programs. Total outstanding shares are down by 10.6% over the past five years alone. This helps boost earnings-per-share (EPS) because there are fewer shares to spread profits across. Management just approved a new $40 billion buyback authorization in Q4; the total $50 billion currently authorized could retire 10% of shares at this price.

Reality Labs: It's not helping Meta today, but that doesn't mean it won't work in the future. This catalyst is a leap of faith in Zuckerberg, though there are reasons to be positive, including a substantial market share in augmented reality.

The trillion-dollar math

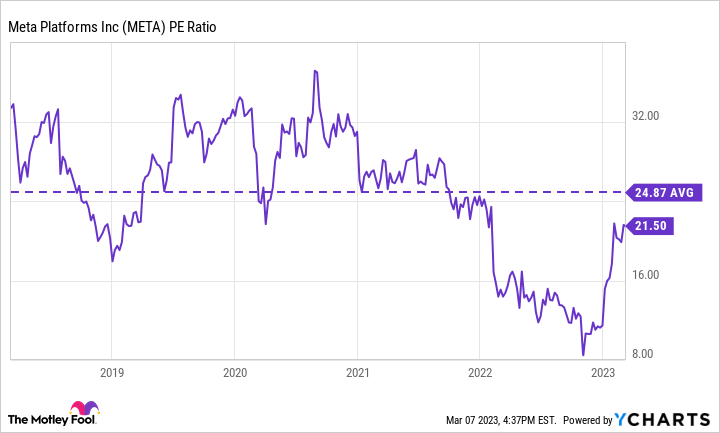

Meta has at least listened to the market; it announced cost cuts in recent months, and the stock responded by soaring off its lows in late 2022. Today, shares are still valued at 10% under their average price-to-earnings ratio (P/E) of the past five years. But to make it fun, let's assume that the stock's valuation remains at its current level indefinitely.

META PE Ratio data by YCharts

In other words, EPS growth will drive all of Meta's investment returns. Hypothetically, let's assume that Meta exhausts its $50 billion in repurchases, reduces the share count by 10%, and never starts another program. That would take outstanding shares from 2.6 billion to roughly 2.34 billion. Of course, the stock could fetch a higher valuation, and management will probably do more repurchases over the next seven years, but I want to be as conservative as possible.

If Meta can grow EPS by an average of 12% annually through a combination of the above catalysts, the company will earn $21.27 per share in 2030. If you multiply that by the P/E of 21.5 and then by our previously determined share count of 2.34 billion, Meta's market cap would be $1.07 trillion. The question is whether you believe that Meta still has the growth potential to make it happen. Only time will tell, but Meta has a realistic shot at eventually becoming a trillion-dollar stock again.